The post Do Apartment Credit Checks Hurt Your Credit Score? appeared first on Avail.

]]>

There’s a good chance your next apartment search will result in multiple credit checks initiated by landlords, but can apartment credit checks hurt your credit score? While they can show up on your credit report as an inquiry, they’re not as harmful as you might think.

Here’s everything you need to know about credit checks and how they can impact your credit score as a renter.

Are Apartment Credit Checks Hard or Soft Inquiries?

A hard credit check is when your credit report is pulled to check your credit history for a new line of credit. Soft credit checks pull the same information, but have less of an impact on your credit score since they’re not attached to a specific application for credit.

Most credit card providers, car dealerships, mortgage lenders, and other lending institutions run a hard credit check when you’re looking to add a new line of credit. Since landlords and property managers primarily want information on your credit history to determine your reliability to make on-time payments, these show up as soft credit checks.

Your credit score is usually left unchanged when applying for an apartment, unless you applied for a new line of credit during the same time period.

How Do Landlords Check Your Credit?

A landlord can check your credit directly through one of the three credit bureaus (Experian, Equifax, and TransUnion) or a property management software platform like Avail. If your landlord is using Avail to check your credit, then this will show as a soft credit check on your report.

You can also submit an Avail Renter Profile if you’re looking to limit overall credit checks on your report, as well as save on rental application fees. A renter profile includes the same information landlords require on a rental application and can be shared through an online link.

You also have the option to add a credit check, background check, and eviction report to your profile for a one-time fee of $55. The credit report is pulled directly from TransUnion and provides all the information landlords need when reviewing your application.

Can Multiple Credit Checks for Rentals Affect My Credit Score?

Since most credit checks for renting are considered soft checks, they won’t negatively impact your credit score. The FICO® credit-scoring model, one of the most popular credit scores, ignores inquiries made within 30 days of scoring. Regardless of how long your apartment search takes, your credit score should not be impacted by your apartment credit checks.

Other credit scores, like the VantageScore credit scoring model, consider all inquiries made within 14 days of rate shopping as a single inquiry, no matter the type of credit application. So if you apply for multiple apartments within that time frame, they’ll all show up as a single soft inquiry.

Limit Credit Checks With an Avail Renter Profile

Finding your next apartment can lead to multiple credit checks and expensive rental application fees, but there are ways to limit them. An Avail Renter Profile helps you easily share your rental history, landlord references, credit report, and much more with one shareable link.

Create an account to make your apartment search less expensive and stressful.

The post Do Apartment Credit Checks Hurt Your Credit Score? appeared first on Avail.

]]>The post How to Increase Your Credit Score to 800 and Above appeared first on Avail.

]]>

Your credit score is a three-digit number between 300 to 850 that’ll impact your ability to rent an apartment, get a new credit card, and even a new car. It’s usually advised to have a credit score around 629 or higher, but having one closer to 800 can be highly beneficial for credit borrowers.

That’s why we provided the tips you can implement today to increase your credit score to 800 and above, as well as how long it will take you to reach this goal.

How to Get an 800 Credit Score

Having an excellent credit score is very much possible, especially if you’ve already been working to improve your credit health. Here are seven steps you can implement to get an 800 credit score:

1. Check Your Credit Score

Your credit score is influenced by five factors: your payment history, credit utilization, account age and type, new accounts, and credit mix. Each factor is weighted differently for both FICO® and VantageScore, with payment history having the most impact on your overall credit score.

Knowing what’s influencing your credit report can make it easier to create a plan for how to get your credit score closer to 800. Whether that’s paying down existing debt or making consistent and on-time payments, the journey to excellent credit requires knowing what you need to work on in the first place.

Check your credit score through any of your credit providers or visit sites like myfico.com for a free FICO® scores estimate.

2. Make On-Time Monthly Payments

Payment history consists of 30% to 35% of your credit score, so if you miss a payment, it can make achieving your goal of an 800 score harder. If making payments has been difficult in the past, you can still increase your credit score by consistently paying the minimum amount towards your bills moving forward until you can afford to make larger payments.

The good news is almost all credit providers offer payment plans or financial assistance for their customers. All you have to do is reach out to your credit provider to discuss your options and plan out how you can get back on track.

3. Keep Your Credit Utilization Below 30%

Credit utilization, also known as credit usage, is the amount of available credit that’s being used compared to how much available credit there is in total. According to Experian, credit borrowers are advised to keep their credit utilization to 30% or less. Going over that can result in a high debt-to-income ratio or too high of an outstanding balance on your card.

Most credit card companies prefer borrowers to keep their information up-to-date, such as your annual income and whether you’re currently renting or own a home. If you applied for a credit card a few years back and now have a higher income, you can then update your profile and see if they’re willing to increase your available credit. While it’s not advised to use this new credit right away, this can help increase your credit score since you’ll technically be using less available credit.

You can also request a credit increase for certain credit cards, especially if you’ve exhibited good credit borrowing habits over the past year. Both options will allow you to improve your credit utilization as long as you refrain from using credit cards for upcoming purchases.

4. Consolidate Your Current Debt

Consolidating your current debt is a great way to start tackling existing debt with less payments and a lower interest rate. Let’s say you have two credit cards, each having a different balance and interest rate. Instead of making two separate payments on each card, you can get a credit repair loan that allows you to pay off the existing balance of both accounts with one loan. Now you’ll only have one payment each month with one interest rate, making it much easier to pay down your credit card balance in less time.

This approach can also be applied to student loans. When you refinance your student loans with one main loan, you can pay down the balance much faster with a lower interest rate, removing the stress of making separate payments for each student loan.

5. Report Your Monthly Bills to a Credit Bureau

Thanks to tools like CreditBoost* and Experian Boost , you can report certain bills to a credit bureau to help you improve your credit with payments you’re already making. With CreditBoost, renters can report their on-time rent payments directly to TransUnion to help build their FICO 9, FICO XD, and VantageScore credit scores with ease.

, you can report certain bills to a credit bureau to help you improve your credit with payments you’re already making. With CreditBoost, renters can report their on-time rent payments directly to TransUnion to help build their FICO 9, FICO XD, and VantageScore credit scores with ease.

For a small fee of $3.95/per reported month, you can easily report past and future rent payments to one of the three main credit bureaus to help get you that much closer to your goal of attaining an 800 credit score. All you have to do is invite your landlord to Avail to set up your account. Then, once you’re ready to make a payment, you can turn on CreditBoost to start contributing to your credit immediately.

6. Avoid Closing Old Credit Accounts

Contrary to popular belief, closing an old credit account can actually harm your credit score rather than improve it. By closing an account, you’ll end up reducing your overall credit availability, which then increases your credit utilization percentage. Another consequence of closing an older credit account is having the average age of your accounts decrease. On average, the total accounts on your credit report should average more than three years to provide creditors a reliable timeframe of your credit habits.

To avoid that from happening, you can occasionally make payments with an older credit card to avoid the account from closing. However, you should try to pay off the balance before the end of the card’s statement period to avoid having your score decrease by a few points.

7. Avoid Too Many Hard Credit Inquiries

It may be tempting to open a new credit card or apply for a personal loan, but it’s important to avoid too many hard credit inquiries. Hard credit inquiries occur when a creditor requests to look at your credit file to determine if they want to approve you for a new line of credit.

Having too many hard inquiries on your credit report can make it seem like you’re consistently looking to open more lines of credit, resulting in lenders being wary of taking you on as a client. If you plan on financing purchases soon or opening a new line of credit, you can space it out throughout the year to avoid decreasing your credit score.

How Long Does It Take To Go From a 700 to 800 Credit Score?

The time it takes to increase your credit score from 700 to 800 varies depending on how aggressive you approach boosting your credit. If you make consistent payments towards your debt and use tools like CreditBoost to report rent payments, you can expedite the process of improving your credit score.

However, it can take up to two years to remove hard inquiries from your credit report or any additional negative remarks that brought down your credit, so be prepared to incorporate long-term credit-building actions like those listed above to help.

Improve Your Credit Health With CreditBoost

Now that you know how to get your credit score to 800, it’ll be that much easier to accomplish your goal and work towards a brighter financial future. Take the first step towards improving your credit by reporting all on-time past and current rent payments through CreditBoost. Create an account to get started today.

*CreditBoost results may vary by individual.

The post How to Increase Your Credit Score to 800 and Above appeared first on Avail.

]]>The post What Credit Score Is Needed to Rent an Apartment? appeared first on Avail.

]]>

Searching for an apartment is an exciting experience, especially if you’re moving to a new city or on your own. However, the process to get approved for an apartment can be tricky if you have no credit or a credit score below 629.

To increase your chances of getting your application approved for your dream apartment, it’s important to know what landlords are looking for and how to practice good credit borrowing habits. Here’s everything you need to know about what credit score is needed to rent an apartment.

What Is a Credit Score?

A credit score is a number between 300 to 850 that credit bureaus provide borrowers to let them better understand a person’s creditworthiness and credit reliability. Your credit score is influenced by various factors, such as your payment history, credit utilization, account age and type, new accounts, and credit mix.

There are different types of credit scoring models — like FICO 9 and VantageScore — that weigh these factors differently, but they all work to rate your creditworthiness. Landlords look at an applicant’s credit report to better understand the way they handle their finances, view their payment history, and see how much debt they currently owe.

What Credit Score Do I Need to Rent an Apartment?

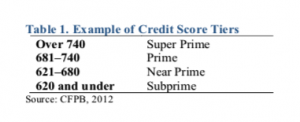

To rent an apartment, landlords typically require renters to have a minimum credit score of 629. But each landlord and property management company vary in their overall requirements, since a credit score alone doesn’t provide a full picture of who you are as a renter.

If you currently have a lower credit score but make on-time payments towards your bills and have an income of three times the rent amount, then you can still get approved for an apartment. But it’s advised to get your credit score closer to the 700s to easily find your next home without any sudden delays.

What Do Landlords Look at On a Credit Report?

When landlords request a credit report, they check to see if you can afford the set rent price and have a history of making payments on time. In addition to your credit score, they may also look at the following:

- Credit utilization: Most landlords don’t focus too much on how much available credit you’ve used. However, if you owe too much debt already, then this can deter them from accepting your application out of fear you won’t have enough money left over to pay rent.

- Account summaries: If you have multiple accounts open, especially ones with any amount past due, then this can indicate an inconsistent history of making required payments on time.

- Total tradelines: Payment history is the biggest contributor to your credit score, as well as what landlords pay the most attention to on your credit report. If you’ve been missing payments on current tradelines — or existing lines of credit — then this will usually result in your application being rejected.

Can You Rent an Apartment With a Low Credit Score?

Although it’s very possible to rent an apartment with a low credit score, you’ll need to make at least three times the rent in monthly income and illustrate good credit borrowing habits so you can prove to your landlord that they can trust you to make timely rent payments throughout your lease. A landlord may also require you to find someone you trust to become a co-signer on your lease in case you’re suddenly unable to make payments.

How to Improve Your Credit Score as a Renter

As a renter, it’s important to always practice good credit borrowing habits to increase your credit score. In addition to making on-time payments on your bills and keeping your credit usage below 30%, renters can begin reporting rent payments to TransUnion with rent reporting tools like CreditBoost.

With CreditBoost*, you can contribute to your FICO 9, FICO XD, and VantageScore credit scores for $3.95/per reported month. This can be especially beneficial if you currently have little to no credit and are looking to build a strong credit history through the rent payments you’re already making. You can also report your utility payments to a credit bureau or explore credit builder loans if you’re looking to improve your credit score without a credit card.

Report Your Rent Payments With CreditBoost

Now that you know what credit score is needed to rent an apartment, the next step is to practice good credit habits to increase your chances of getting approved for your next place. To start, you can invite your landlord to Avail to set up your account and begin reporting your rent payments through CreditBoost. Whether you’re moving into a new rental or still paying rent at your current place, you can start improving your credit health through each on-time rent payment.

Create an account or log in to turn on credit reporting today.

*CreditBoost results may vary by individual.

The post What Credit Score Is Needed to Rent an Apartment? appeared first on Avail.

]]>The post What Is a VantageScore? appeared first on Avail.

]]>

A VantageScore is a tri-bureau credit scoring model that was developed by Experian, TransUnion, and Equifax to compete with FICO®. This credit score model has gone through four major variations since its official launch in 2013, with VantageScore 4.0 being the most recent version.

In this article, we’ve provided an in-depth look at the VantageScore credit scoring model, how it works, and the importance of this credit score.

How Does the VantageScore Credit Model Work?

VantageScore previously refrained from using percentages to illustrate the importance of each aspect of your credit that’s calculated into your final score. However, it recently released an updated breakdown indicating how important each factor is to one’s overall score.

- Payment history (40%)

- Age and type of credit (21%)

- Credit utilization (20%)

- Size of balances (11%)

- Inquiries/new accounts (5%)

- Amount of available credit (3%)

Similar to the FICO® scoring model, your payment history has the biggest influence on the current state of your VantageScore credit score.

What Is the Difference Between VantageScore 3.0 and VantageScore 4.0?

VantageScore 4.0 introduced three major changes to its credit scoring model since the release of the VantageScore 3.0. The following changes are:

- Uses trending data from the three major credit bureaus (TransUnion, Experian, and Equifax) to get an in-depth view of a person’s borrowing habits and payment history.

- Does not weigh tax liens and civil judgements as heavily as the VantageScore 3.0 credit scoring model.

- Allows people who would normally be neglected by traditional scoring models build credit without a credit card.

Overall, the newer version of VantageScore adjusts to current credit-borrowing trends to provide lenders and landlords with an accurate view of a person’s creditworthiness.

What Is a Good VantageScore?

VantageScore provides a credit score that ranges from 300 to 850. Scores between 661 to 850 are considered ideal, while scores below 660 need improvement.

If you’re currently in the process of building your VantageScore credit score, you can work on paying down any existing debt or use tools like CreditBoost* to begin reporting on-time rent payments directly to TransUnion. For a small fee of $3.95 per reported month, you can contribute past and future rent payments to your VantageScore credit score to help focus on your credit health through payments you’re already making each month.

All you have to do is create an account and invite your landlord to Avail. Once they’ve set up their account and begin collecting rent online, you can start reporting your on-time rent payments right away to contribute to your FICO 9, FICO XD, and VantageScore credit score.

VantageScore vs. FICO® Score: What’s the Difference?

Both FICO® and VantageScore credit scores can provide an accurate view of a person’s credit borrowing habits based on their calculated credit data. However, there are a few differences that every credit holder should be aware of.

A VantageScore credit score can be established in as soon as a month, while a FICO® score requires at least three to six months of credit activity to produce a credit score. VantageScore also allows people that would normally be excluded from most FICO® models to build credit through on-time payments towards their monthly bills.

Late payments can negatively impact your VantageScore credit score much more than a FICO® credit score since they weigh that factor differently.

Are There Lenders That Use VantageScore?

According to a recent study conducted by Oliver Wyman, the VantageScore model accounted for roughly 12.3 billion credit scores used between July 2018 and June 2019, proving that it’s a popular credit scoring model. That being said, credit card companies, personal loan providers, and landlords may use VantageScore to better understand the way you handle your finances rather than simply checking your credit score.

Remember that lenders and landlords all vary in which credit scores they refer to, so it may be best to ask them if your VantageScore credit score will be looked at during the approval process or if they prefer using a different model instead.

Build Your VantageScore With CreditBoost

If you’re looking to build your credit health right away, you can begin contributing your on-time rent payments to your VantageScore credit score with the help of CreditBoost.

Create an account to send an invitation to your landlord to join Avail today. Already have an account? Log into your account to turn on the CreditBoost feature the next time you make a payment and start working towards a better financial future.

*CreditBoost results may vary by individual.

The post What Is a VantageScore? appeared first on Avail.

]]>The post FICO Score 9: Everything You Need to Know appeared first on Avail.

]]>

When focusing on maintaining or improving your credit score, you will likely hear about your FICO Score 9. This credit scoring model looks at your medical debt, paid collections, and rental history differently than previous versions of the FICO® credit-scoring model. More credit lenders are switching from the former FICO 8 scoring method to FICO 9 to better understand a person’s money habits, but you may be wondering why this change matters to you.

In this article, we explain everything you need to know about FICO Score 9 and share four easy ways to improve your credit score.

What Is a FICO Score 9?

A FICO Score 9 is the second-latest version of the FICO® credit-scoring model that officially launched in 2014 with some slight differences from the previous version, FICO 8. There have been numerous revisions of the credit scoring model over the past three decades to keep up with changing credit-borrowing trends.

The main function of your FICO Score 9 credit score is to inform lenders and landlords of your reliability as a borrower and your ability to make on-time payments. When compared to previous versions of the credit scoring model, FICO Score 9 treats medical debt, collection accounts, and rental history differently to allow credit lenders to better determine a person’s creditworthiness.

How the FICO 9 Is Different From FICO 8

The new credit scoring model approaches three categories differently than FICO Score 8. Here are the changes to be aware of:

- Medical debt: FICO Score 9 doesn’t consider medical debt as much as FICO Score 8 since medical bills are not a strong indicator of credit risk compared to other types of unpaid bills.

- Collection accounts: Collection accounts that have been paid in full are no longer taken into consideration when calculating a person’s credit score. Existing medical debt will have less of a negative impact on FICO Score 9.

- Rent payments: Rental history can be factored in a FICO Score 9 to help those with little to no credit history establish credit without a credit card. Although landlords are not legally required to report a renter’s rent payments to a credit bureau in most states, you can request them to start or do it yourself through tools like CreditBoost.

If you currently have little to no credit, the FICO Score 9 can be a great way to start building it through rent and utility payments, a credit builder loan, and more.

When Do Lenders Use the FICO Score 9?

Many lenders are beginning to move away from the FICO Score 8 to FICO Score 9 for a more updated and predictive FICO® score evaluation that improves their assessment process. However, each lender varies in which credit score they refer to during the approval process, which is why you’ll want to ask your specific lender if they will be looking into your FICO Score 9 at all.

4 Ways to Improve Your FICO Score 9 Credit Score

Improving your credit score is easier than you think. We’ve outlined four ways to improve your credit score in no time.

- Pay bills on time: Payment history is typically the biggest factor in your current credit score. The more on-time payments you make towards your monthly bills, the easier it will be to increase your credit score.

- Report your rent payments: Now that renters are allowed to report rent payments to credit-evaluating systems like FICO Score 9, using a tool like CreditBoost* can help you easily build credit without a credit card. All you need to do is invite your landlord to Avail to create an account and set you up to start reporting your rent payments.

- Use less credit: If you’re making on-time payments but still continue to see a decrease in your credit score, then it may be due to credit utilization. According to Experian, one of the three main credit bureaus, it’s advised to have a credit utilization rate below 30%. The less available credit you use, the better.

- Check your credit score: Regularly check your credit score to keep tabs on how you’re doing from a credit standpoint. It will help to identify the biggest contributing factor to your current score in order to make spending changes that will improve your credit.

How Do I Find Out My FICO 9 Credit Score?

Based on information from your credit report, you’ll receive a score between 300 to 850 that will indicate your creditworthiness. The Consumer Financial Protection Bureau makes it easy for anyone to access their credit score through their credit card company or any other provider that has opened up a new line of credit. While there are some methods to check your credit score that are free, you may need to pay a small fee to get your actual FICO® scores.

You can also explore sites like myfico.com to use their free FICO® scores estimator to get a projected credit score or obtain your actual credit score for a monthly fee of $19.95.

Improve Your Credit Score With CreditBoost

FICO Score 9 makes it easier to improve your credit score by minimizing the effect of medical debt, allowing you to report on-time rent payments, and excluding fully paid collections debt. But it’s still important to practice good credit habits to avoid decreasing your credit score.

Invite your landlord to Avail today to start reporting your past and future rent payments to TransUnion to contribute to your FICO 9, FICO XD, and VantageScore credit scores. All you have to do is create an account, send an invitation to your landlord to join, and we’ll take care of the rest.

*CreditBoost results may vary by individual.

The post FICO Score 9: Everything You Need to Know appeared first on Avail.

]]>The post What Bills Affect Your Credit Score? appeared first on Avail.

]]>

While there are traditional ways to build your credit, certain monthly bills can also positively or negatively affect your credit score. Figuring out what bills help build credit may not be easy at first, which is why we did the heavy lifting for you to make improving your credit health that much easier.

These are the bills you can leverage to boost your credit score today, as well as the importance of on-time payments and your payment history.

What Bills Help Build Credit?

Not all of your monthly bills can be reported to credit bureaus, but you may be surprised at exactly which ones have the power to help your credit score. Here are the main six bills to be aware of when building up your credit score.

1. Rent Payments

Before property management platforms, renters were unable to report rent payments to credit bureaus to build their credit health. Now that more landlords are utilizing platforms like Avail to make renting easier, renters are able to pay rent online and report on-time payments through CreditBoost* for $3.95 per reported month.

CreditBoost can be extremely beneficial for those with little to no credit, since Avail automatically reports on-time rent payments to TransUnion to contribute to your FICO XD score — an alternative credit score that looks at how you handle utility payments to determine your creditworthiness.

This tool also reports to your VantageScore and FICO 9 credit scores, which are often used by various lenders and landlords to gauge your reliability towards payments.

Invite your landlord to Avail to create an account so you can start reporting rent right away.

2. Utility Bills

Utility companies don’t report payments to credit bureaus unless an account goes into collections or is considered delinquent. But if you’re looking to improve your credit health without opening up a new line of credit, then it may be worth exploring a platform that allows you to report your utilities, phone bill, and popular streaming services for free — like Experian Boost.

CreditBoost and Experian Boost together can jumpstart your journey to a higher credit score by reporting payments automatically to both TransUnion and Experian.

3. Auto Loan Payments

Auto loans can either positively or negatively affect your credit score depending on your payment history. This type of loan consists of a set amount of installments that need to be paid during a certain timeframe, so even one late or missed payment can harm your credit score.

Know that your auto loan payments are automatically reported to credit bureaus each month, so it’s always advised to make your payments on time when trying to preserve and build your credit health.

4. Student Loan Payments

Considering 43.2 million students have an average debt of $37,787 in student loans, it’s important to know the impact this loan can have on your credit score. Whether you have public or private loans, both types need to be handled carefully to avoid negative remarks on your credit report.

Almost all student loan providers keep a track record of the payments you make (and miss), so while you can default on your loans, it’s advised to make as many on-time payments as possible. If you’re in need of some financial flexibility, you can also contact your loan provider to explore your payment options.

5. Credit Card Payments

There are both good and bad ways credit cards can affect your credit score. Applying for a new line of credit alone is considered a “hard inquiry,” which can decrease your score by a few points. Overspending on your card can also harm your score, as it shows you’re at risk for not being able to pay it all off.

However, having a lower credit utilization rate — meaning that you’re using a small portion of your card’s available credit — can boost your credit score over time.

It’s important to note that even missing one credit card payment can substantially decrease your credit score within 30 days. Credit cards offer great benefits, but they should always be used responsibility to avoid decreasing your credit score drastically.

6. Medical Bills

It’s easy to assume medical bills will not impact your credit score since most healthcare providers don’t report payments to credit bureaus. But if you have any outstanding medical debt that recently went to collections, your healthcare provider will likely sell your debt to a collection agency.

This will not only impact your credit score in the short term, but it will continue to live on your credit report for up to seven years from the original delinquency date. The good news is that this type of debt can be removed from your credit report, though it will take a few weeks to complete.

This is why you should always negotiate your bill or start a payment plan with your medical provider if you suddenly have a medical bill you can’t afford.

How Important Is My Payment History?

Your payment history is the most important factor credit lenders and landlords look at on your credit report. Failing to make any kind of payments can mark you as unreliable and make it harder to get approved for new lines of credit or a new apartment.

For more context on the importance of payment history, let’s look at the FICO® scoring criteria. Your credit score is based on the following factors:

- Payment history (35%)

- Credit utilization (30%)

- Account age (15%)

- Inquiries/new accounts (10%)

- Credit mix (10%)

VantageScore, a credit scoring model created by the three major credit reporting agencies as an alternative to FICO®, looks at slightly different criteria. Your credit score will still be determined by the following unweighted factors:

- Payment history

- Age and type of credit

- Credit utilization

- Size of balances

- Inquiries/new accounts

- Amount of available credit

Whether you’re looking at your FICO® or VantageScore credit scores, payment history plays the biggest role in determining your reliability as a borrower. The more on-time payments you make towards your bills can help you avoid a questionable payment history, and even boost your credit score.

Report Rent Payments With Avail

Now that you know what bills affect your credit score, the next step is creating a plan to improve your credit. As a renter, your largest monthly payment is probably your rent, so why not report it to a credit bureau?

Create an account or log in today to invite your landlord and start reporting your on-time rent payments through CreditBoost. Once your landlord sets up your account, you can begin contributing to your FICO 9, FICO XD, and VantageScore credit score all in one place.

*CreditBoost results may vary by individual.

The post What Bills Affect Your Credit Score? appeared first on Avail.

]]>The post How to Buy Your First Home With Bad Credit appeared first on Avail.

]]>

The homebuying process can be overwhelming for many, especially for those looking to buy a home with bad credit. While it may seem impossible to purchase a home with a credit score of less than 629, it’s very much doable so long as you take the right steps.

That’s why we outlined everything you need to know about how to buy a home with bad credit and increase your chances of getting preapproved for a mortgage.

Can You Buy A House With Bad Credit?

The minimum credit score requirement to buy a house varies depending on the loan you’re applying for. Conventional loans require a credit score of at least 620, but first-time homebuyers exploring Federal Housing Administration (FHA), VA or agriculture mortgage loans can get away with having a credit score of 500.

There are also home loans for people with bad credit scores, but you’ll most likely pay a higher mortgage payment with a high interest rate. To avoid overpaying in interest and fees, you can contribute a higher down payment in cash to reduce the amount you’ll need from the loan itself. The more money you can put towards a down payment, the less you’ll need to apply for in the form of a mortgage loan.

Unlike traditional banks, some mortgage lenders may be able to help you apply for the best mortgage loans that you qualify for and create a plan to improve your credit score overall.

How to Get a Mortgage With Bad Credit

Getting a mortgage loan with bad credit is possible, but you’ll need to take action to ensure you find the best deal. We’ve outlined five steps you can take to increase your chances of getting preapproved for a mortgage loan with a bad credit score.

1. Check Your Credit Score

Before meeting with a mortgage lender, you should first check your credit score to see what’s impacting your credit health the most. Your credit score is based on five factors: payment history, amounts owed, length of credit history, credit mix, and new credit.

Each factor impacts your credit score differently, but you’ll want to know exactly what’s causing the most damage and how you can quickly fix it. Have you missed credit card payments or do you currently have a large amount of debt you owe? The sooner you can determine what your bad credit consists of, the easier it will be to come up with a plan to fix it to get approved for a home loan.

2. Work With a Mortgage Lender

Once you know what your credit score is, the next step is meeting with a mortgage lender. You have the option to work with a traditional bank, but a Mortgage Loan Originator or direct lender can help you find more home loans for buyers with bad credit.

They will run a qualifications review by having you fill out a 1003 form with all of your information and current liabilities. You can also use this time to discuss your current credit score and see if they have any suggestions on which loans you should apply for to get the best deal.

3. Explore Credit Repair Companies

A credit repair company works to improve your credit by working with the three main credit bureaus — Experian, TransUnion, and Equifax. They focus primarily on removing negative marks on your credit report due to late or missed payments, maxing out your credit card, debt collections, and more. They accomplish this by negotiating with creditors and credit bureaus to resolve issues impacting your credit health.

Credit repair companies charge anywhere from $19 to $149 on a monthly basis, but this varies depending on how much work needs to be done on your credit report. Your mortgage lender may have some suggestions on companies to explore when working on your credit, or you can ask family or friends for recommendations.

4. Create a Monthly Budget

A monthly budget can help you save for a down payment and pay off any outstanding debt that’s contributing to your bad credit score. If you’re looking to purchase a home in the next few months, then the best way to increase your chances of getting preapproved is by working on your credit now and saving for a down payment of more than 20% as soon as possible.

Credit tip: Track all of your expenses each month and set aside a certain amount for each category to avoid overspending.

5. Improve Your Credit Score for a Home Loan

Once you’re working on improving previous blemishes on your credit report, it’s also important to pay attention to what you’re doing now that can help you get a better credit score for a home loan. One way to help your credit score is to work on paying off credit card debt or student loans early or by making on-time payments.

It’s also best to avoid opening up new credit card accounts (to avoid hard inquiries) or closing existing cards, since both can decrease your credit score. For those currently renting an apartment, reporting your on-time past and current rent payments with CreditBoost* can be a helpful tool to start working on your credit health today.

Improve Your Credit Health With Avail

There are ways to purchase your first home with bad credit. Whether that’s by working with a mortgage lender or by saving for a larger down payment, you can in fact purchase a home with a score of less than 629. See how much house you can afford with your current debt by using the Realtor.com® Home Affordability calculator.

While buying a home with bad credit is possible, it’s still best to work on improving your credit score by paying off and making on-time payments to any outstanding debt. You can also start reporting on-time rent payments through CreditBoost with Avail, which will go towards your FICO 9, FICO XD, or VantageScore credit scores.*

Create an account today or log in to get started.

*CreditBoost results may vary by individual.

The post How to Buy Your First Home With Bad Credit appeared first on Avail.

]]>The post How to Rent an Apartment With Bad Credit appeared first on Avail.

]]>

Being unemployed, having past or current debts, or being an international student or employee are just a few reasons why a renter might not have a desirable credit score. While each of these situations is different, the common factor is that renting with a credit score between 300 and 500, or none at all, can be complicated.

If you’re a renter with low or no credit, landlords might perceive you as someone who is unable to keep up with repeating payments or irresponsible with money, which can make finding a rental harder. That’s why it’s important for you to be open to negotiations and various discussions with a landlord on their credit history. Here are some of the ways you can do this.

1. Find Credit-Free Apartments

A good starting place for those who want to find an apartment that will accept their lower credit score are buildings that don’t check a renter’s credit at all. These landlords, apartments, and buildings offer the most flexibility for you as a renter who would otherwise be turned away for your credit. This will also require less work on your end.

It’s important to note that this option is not as common as rentals that do require credit checks, so it’s wise to not only look for credit-free apartments but those that check credit as well.

Find available rentals near you on Realtor.com®.

2. Build a Renter’s Resume

Renter’s resumes are similar to those that are required by various employers, but these feature your rental history rather than your job experience. It’s one of the best ways to present yourself on paper as a reliable renter, with your experience and your landlord recommendations all in one place. A renter’s resume will work to balance your credit score, showing the landlord that you’re still reliable and responsible.

3. Have Proof of Employment and Savings

Some landlords might take a renter’s low credit score to mean that they don’t have the financial stability to make regular payments. In order to show a landlord that despite your credit score, you are able to meet the financial rental expectations, it’s smart to supply proof of employment and savings.

This might come in the form of a paycheck or contract. If proof of employment and income is not an option, showing that you’ve accrued enough savings for rent is another valid option.

4. Pay More Upfront

Overall, a renter with low to no credit needs to be prepared to possibly pay more upfront in order to secure an apartment, if the landlord requests this. Though this option is less common, it’s better to put aside a bit more money to, for example, pay a larger security deposit or put two to three months’ rent down upon signing the lease.

5. Turn On Autopay

Using automatic rent payment options is another way for a renter with low credit to prove to a future landlord or property management company that they can make monthly rent. There are many different services that will allow you to make automatic rent payments each month, including Autopay for renters paying their rent through Avail

Not only does Autopay take the stress off of you to remember when to pay rent, but it also allows your landlord to be comfortable knowing that rent will be paid on time each month.

6. Find a Co-Signer

Renters with low credit can also find a co-signer, otherwise known as a lease guarantor, with higher credit in order to secure a rental property. If you’ve exhausted all other options, this could be a good move for you. However, this measure should be the final resort. Signing a lease with a co-signer can be risky for both parties, as the co-signer will be legally responsible for paying rent if you cannot.

Because of these possible risks, it’s best to find a co-signer that you know and trust, and that trusts you. If this is not an option, there are various lease guarantor services available. These companies act as a co-signer and will back you in a lease agreement. However, the price of these services vary based on your circumstances and their own requirements, adding an additional cost to your rent.

7. Boost Your Credit From Renting

A beneficial tool for renters with low credit is the Avail CreditBoost* feature, which gives renters a chance to positively impact their FICO 9, FICO XD, and VantageScore credit score by paying their monthly rent on time. CreditBoost also allows renters to report their previous rental payments of up to two years, retroactively helping them build credit through previous rentals.

While there is more to be aware of as a renter with low to no credit looking for a new rental property, it’s important to understand that there are still plenty of options for finding a home. Be open to all the different ways you can show a landlord how responsible you are as a renter, and when you do secure a rental property, make sure you’re helping build up your credit score with every on-time rent payment.

*CreditBoost results may vary by individual.

The post How to Rent an Apartment With Bad Credit appeared first on Avail.

]]>The post Tenants Benefit When They Get Credit for Paying Rent appeared first on Avail.

]]>

HUD’s most recent study, reported by the Wall Street Journal, explains that tenants stand to benefit when their landlords report on-time rent payments. For vulnerable renters in public housing with limited to no credit, reporting on-time rent payments can be highly important to their credit health. “This study shows that public housing tenants currently have credit scores well below average. One-half to two-thirds of those with credit scores are rated as subprime (below 620). Up to half of all tenants studied were “credit invisible” to one or both of the consulted credit scoring systems,” according to HUD.

In conjunction with the release of the study, HUD’s Assistant Secretary for Policy Development and Research said, “Rent is the largest monthly recurring expense that many households pay and reporting it can be a powerful way to reduce credit invisibility … This unprecedented study will excite a new conversation about the need for focusing on improving the credit of low-income families, and how on time rent payment is an important way to show credit-worthiness.”

Low credit scores increase costs for renters in other areas of life. Acquiring insurance, a cell phone, credit cards, car loans, and home loans all require credit. Not to mention many landlords require a credit check in order to rent an apartment or house. Renters with subprime credit scores end up paying higher deposits, fees, and interest rates on nearly everything. The single largest monthly bill renters are paying isn’t counting towards their credit score.Click To Tweet

According to Housing Authority of Cook County’s (HACC), “Other HUD research finds that low credit scores substantially limit tenant choice on where they search for private rental housing and that tenants are motivated to improve their credit, receive financial education, and take advantage of available credit counseling.”

The HUD study also reflects much of what Avail has seen in regards to reporting rent payments for renters.

The release of @HUDgov’s study confirms what we’ve known all along: Tenants fair far better when they’re able to get credit for paying rent on time. Read more about the study via @_willparker_‘s piece for @WSJ here: https://t.co/sfvVHLGCrp

(1 of 5)

— Avail (@HelloAvail) February 14, 2020

Historically, reporting rent payments in the past has been a challenge for independent DIY landlords because they simply did not have the time or the resources to do this. Often only big landlords with expensive solutions were able to achieve this.

(2 of 5)

— Avail (@HelloAvail) February 14, 2020

“Currently, it is negative rent-payment information that accounts for the overwhelming majority of what credit agencies receive on rent, according to HUD.” (@WSJ)

And this is exactly what we hope to change.

(3 of 5)

— Avail (@HelloAvail) February 14, 2020

By reporting on-time rent payments, @helloavail is giving renters who may have limited or no credit, the chance to build their credit above subprime cutoffs.

(4 of 5)

— Avail (@HelloAvail) February 14, 2020

For any housing authorities that are looking for an affordable solution to help residents, come and talk to us — we’d love to help! All media inquiries, direct quotes or questions please reach out to @ryanmcoon, CEO of Avail (or email us: press@avail.co) https://t.co/eGizXusffa

— Avail (@HelloAvail) February 14, 2020

HACC was a significant participant in the study and also released a statement. Richard Monocchio, HACC Executive Director, said, “More and more landlords throughout suburban Cook County are using credit score checks to determine whether or not to accept a tenant’s application, especially in areas of opportunity … For our low-income tenants, many of whom have low or non-existent scores due to their circumstances, this means an automatic denial. HACC is proud to have participated in this groundbreaking study and is excited to explore a path forward given the promising findings.”

Reporting rent payments helps renters, and it doesn’t have to be difficult or time-consuming for landlords to report on-time rent payments. HUD concludes that most landlords do not have the capability to report rent for their tenants, since the process is either labor intensive or cost prohibitive. Avail has created a solution to tackle this problem, called CreditBoost*.

It’s not only tenants who will win from reporting on-time rent payments — both landlords and tenants benefit when tenants are incentivized to pay their rent on time. Tenants have the added benefit of reporting their on-time rent payments as a form of building credit, which is a great way to help those that HUD refers to as “credit invisible” avoid unnecessary and costly fees.

“The report released by HUD reiterates what we’ve known for a while,” said Avail CEO Ryan Coon. “Renters benefit when their on-time payments are considered by the credit bureaus. With renting becoming more popular across all age groups and income brackets, reporting rent payments is increasingly important for all renters. Last year, we released functionality for this inside of the Avail platform, and have already helped tens of thousands of renters from across the U.S. boost their scores via our CreditBoost feature. We look forward to working with more landlords and public housing authorities to boost credit scores for all renters across the country.”

HUD concludes that more attention to reporting rent payments is warranted by stakeholders and policymakers. Avail is already working to help landlords who otherwise wouldn’t able to report rent payments and is ready and capable to help housing authorities across the country.

Housing Authorities looking for a solution provider to report rent payments on behalf of renters, please email partnerships@avail.co.

*CreditBoost results may vary by individual.

The post Tenants Benefit When They Get Credit for Paying Rent appeared first on Avail.

]]>The post How to Report Rent Payments to Credit Bureaus appeared first on Avail.

]]>

Rent is probably your biggest expense each month. But are you getting anything in return for making those sizable payments on time? Most people aren’t, and many renters don’t even realize they could help improve their credit by knowing how to report rent payments to credit bureaus.

NerdWallet reported that less than 1% of credit files contain any rental information, even though all three major credit bureaus (Equifax, Experian, and TransUnion) include rent payment information when they receive it.

Renters can benefit from reporting their on-time rent payments — especially renters who need some help boosting their credit score or developing a credit history — and there are a few ways it can be done.

How to Get Credit for the Rent You Pay

It’s important to keep in mind that the two major credit scoring companies (FICO and VantageScore) handle rent payment information differently.

The FICO Score, which is commonly used, doesn’t calculate rental payment information into scoring. But the newer versions of the report (both the FICO 9 and FICO XD) do take rental payments into account. VantageScore also incorporates rental payment information into their credit scoring.

Because renters can’t report their rent payments themselves, they’ll need their landlord or a third-party reporting service to report the payments for them.

1. Use a Rent Reporting Platform

Renters can sign up to have their rent payments reported through a third-party reporting platform. Because rent reporting usually benefits a renter the most, it can make sense to use a platform where renters are the ones responsible for signing up and paying any associated fees.

Platforms like CreditBoost report rent payments on a monthly basis to TransUnion, and renters can choose to report their past rent payments and/or current payments to the bureau. An added bonus for renters is that only on-time payments are reported, so their score won’t necessarily be hurt if they slip up and submit a late payment.

2. Have Your Landlord Report Your Rent Payments

Your landlord is another source for reporting your rent payments. Companies like TransUnion accept rent payment information directly from landlords, but your landlord will need to sign up for one of the services and pay the associated fees.

Some landlords will be inclined to skip the extra effort of signing up for a reporting service, but reporting rent to a credit bureau actually helps encourage renters to pay their rent on time, since falling behind on multiple payments can lead to negative reporting and a decreased credit score.

3. Pay Rent With Your Credit Card

Outside of directly reporting rent payments to a credit bureau, some renters overlook simple payment options that can help them improve their credit score — like paying rent with a credit card.

Online rent payment platforms like Avail allow renters to pay their rent with a credit card, which can help strengthen credit and, in some cases, help renters get reward points or cash back on rent payments.

While these payments won’t be listed as a separate tradeline on a credit report, they can still help boost a renter’s credit score if they’re consistently paying off full balances as they would a regular rent payment.

Which Property Management Software Platforms Report Rent Payments?

Over the past few years, property management software platforms have started providing landlords and renters the opportunity to report on-time rent payments to a credit bureau. As some states begin requiring landlords to allow renters to report rent payments, it’s always a good idea to see if your landlord is already utilizing landlord software that can help you report your rent.

There are a few property management software platforms that offer rent reporting capabilities, but they may require your landlord to pay a fee or can only help with a small handful of tasks. With Avail, renters can report their monthly rent with CreditBoost for a low fee, and landlords can easily collect rent payments and manage various properties in one place for free.

How to Start Reporting Your Rent Payments

Chat with your landlord to find out if they have a system in place for reporting rent payments. Some landlords might already offer the option to report rent to the credit bureaus and help you improve your credit.

If they don’t, you can sign up for a third-party reporting platform like CreditBoost and invite your landlord to collect rent online. Avail lets renters pay their rent with a bank account, debit card, or credit card, and once enabled, CreditBoost will automatically report all on-time rent payments that are made through Avail.

Find out more about paying rent through Avail and how reporting rent payments with CreditBoost can help build your credit*.

*CreditBoost results may vary by individual.

The post How to Report Rent Payments to Credit Bureaus appeared first on Avail.

]]>