The post How High Debt-to-Income Ratios Are Viewed by Mortgage Lenders appeared first on Avail.

]]>

Most mortgage lenders look at your credit score and the size of your down payment during the approval process, but your debt-to-income ratio (DTI) is the biggest factor in being able to qualify for a mortgage loan.

In this article, we explain how high debt-to-income ratios are viewed by mortgage lenders and provide you with ways to pay down debt in no time.

What High Debt-to-Income Ratios Tell Mortgage Lenders

Mortgage lenders refer to your DTI ratio to get a better understanding of how much of your monthly income goes towards debt repayment. There are two parts to your DTI — your front-end and back-end DTI — but your back-end DTI is looked at more often, since this number takes into account any existing debt that can impact your ability to take on a mortgage.

A high DTI tells a mortgage lender that you currently don’t have enough available income to take on another form of credit. And while it’s easy to think a bad credit score can result in your application being denied, most rejections are due to higher DTI ratios, according to the National Association of REALTORS® (NAR).

What Is a Good Debt-To-Income Ratio to Get a Mortgage?

Now that we’ve covered how a high DTI ratio can impact your chances of getting approved for a mortgage, the next step is knowing what ratio you’ll need to have to qualify for each type of mortgage loan. Here are the main four mortgage loans you can explore as a first-time homebuyer.

1. Conventional Loans

The max DTI ratio for a conventional loan was previously 45%, but has recently been increased to 50% to help more first-time homebuyers qualify for a mortgage. Conventional loans are ideal for homebuyers with a strong credit score and large down payment.

2. Federal Housing Administration (FHA) Loans

Unlike a conventional loan, FHA loans are easier to qualify for since they’re backed by the U.S. Federal Housing Administration. The maximum FHA debt-to-income ratio is set at 57%, making it easier to qualify for a mortgage with student loan debt or a lower credit score.

3. U.S. Department of Agriculture (USDA) Loans

The USDA DTI ratio limit is 41%, but mortgage lenders only factor the income and debts of the people on the loan, even though the income of all the people occupying the space are initially considered to determine USDA loan eligibility.

4. Veterans Affairs (VA) Loans

Veteran Affairs (VA) loans require a debt-to-income ratio of 41% or lower to qualify for this type of loan. However, VA loans are typically more lenient when it comes to their requirements since they work on helping former members of the Armed Forces easily finance a home. So even if you have a higher DTI ratio than 41%, you may be able to still get approved for a VA loan if you have a good credit score.

How to Quickly Reduce Your Debt-to-Income Ratio

Reducing your current DTI ratio may seem daunting to accomplish, but it can easily be done with the right steps. Here are three ways you can pay down any existing debt obligations:

- Pay down existing debt: Although paying down your debt is an obvious tip, this is almost always the first step to reducing your DTI ratio. You can either set up a budget to monitor your debt repayment efforts or pay a little extra each month on your payments.

- Avoid financing large purchases: It may be tempting to invest in a new couch or buy a new car, but the best way to avoid increasing your DTI ratio is by not financing new purchases until your current debt has been paid off.

- Refinance current loans: If you have an auto loan or student loans with a high interest rate, then it may be worth exploring refinancing options. Not only can you qualify for a lower interest rate, but it’ll be easier to pay down any current debt you have.

Get Preapproved for a Mortgage With Realtor.com®

The key to getting approved for a mortgage is not only preparing your finances to take on a home loan, but having the right team by your side. On Realtor.com®, you can get connected with a trusted mortgage lender in no time to begin the mortgage process. Visit Realtor.com® to start the homebuying process today.

Discover more first-time homebuyer content with expert insights on how to find a Realtor, get preapproved for a mortgage, and more on our first-time homebuyers resource page.

The post How High Debt-to-Income Ratios Are Viewed by Mortgage Lenders appeared first on Avail.

]]>The post First-Time Homebuying Checklist: Steps to Buying a House appeared first on Avail.

]]>

Buying your first home can be a confusing process where every step happens simultaneously, making it difficult to know where to begin. That’s why understanding the steps to buying a house can make the overall process easier for every first-time homebuyer.

We created a first-time homebuying checklist that outlines the main steps to buying your first house to easily reference throughout the process. This checklist is perfect for homebuyers who want a simple overview of how to purchase a house to take on the go.

What Are the Steps to Buying a House?

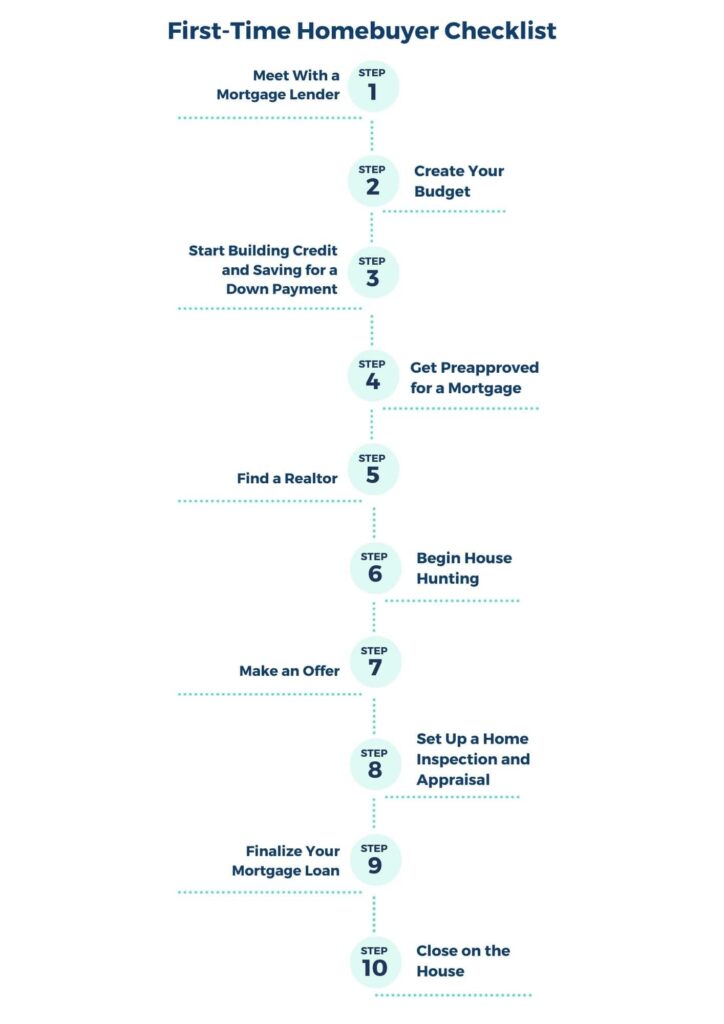

To make things easier, here are the 10 steps you will need to follow (and check off your list) when buying your first home.

1. Meet With a Mortgage Lender

The first thing you’ll want to do is meet with a mortgage lender you’re interested in working with for your first home purchase. This meeting will give you an idea of what loan options are available to you, if you’ll need to improve your credit score for the loan you want, and how much you will need to save in terms of upfront and long-term homebuying costs.

2. Create Your Budget

The costs of buying a home can quickly add up, which is why you’ll need to create a budget to properly prepare your finances. Your budget should factor in the upfront costs — your down payment, mortgage fees, and initial property taxes — as well as other hidden costs of buying a home that will add to the total cost.

A comprehensive and realistic homebuying budget can provide visibility on how much home you can afford, as well as future expenses to prepare for. If you’re unsure on how much you can afford, you can use the Realtor.com® Home Affordability Calculator to help you confidently craft a budget.

3. Start Building Credit and Saving for a Down Payment

Although it’s possible to buy your first home with bad credit or no down payment, the homebuying process will be much more efficient with a credit score over 629 and a larger down payment. A more favorable credit score will allow you to qualify for more mortgage loan options with lower interest rates and lower monthly payments.

Depending on your mortgage lender, if you can save at least 20% of the home’s cost for your down payment, you won’t need to pay for private mortgage insurance (PMI), which adds to your overall monthly costs.

Currently renting? Use CreditBoost* to report your on-time rent payments to TransUnion to help improve your credit score.

4. Get Preapproved for a Mortgage

A mortgage lender can help facilitate the preapproval process, as well as help you find the best mortgage loan for you. Since you’ll want to be preapproved for a mortgage before making an offer on a home, you’ll want to get this done on the earlier end of the house-hunting process. That being said, you don’t want to get preapproved for a loan multiple times since the process will affect your credit score, so it’s important to have your finances in order first.

Mortgage lenders that specialize in helping first-time homebuyers can even provide certain incentives — such as interest rate discounts or a lower annual percentage rate (APR) — for those looking to take out their first home loan. Realtor.com® makes this step a bit easier by connecting you with the right mortgage lender that will fit your financial needs.

Find out how much you’ll be spending on your mortgage loan through the Get A Rate Estimate tool by Realtor.com®.

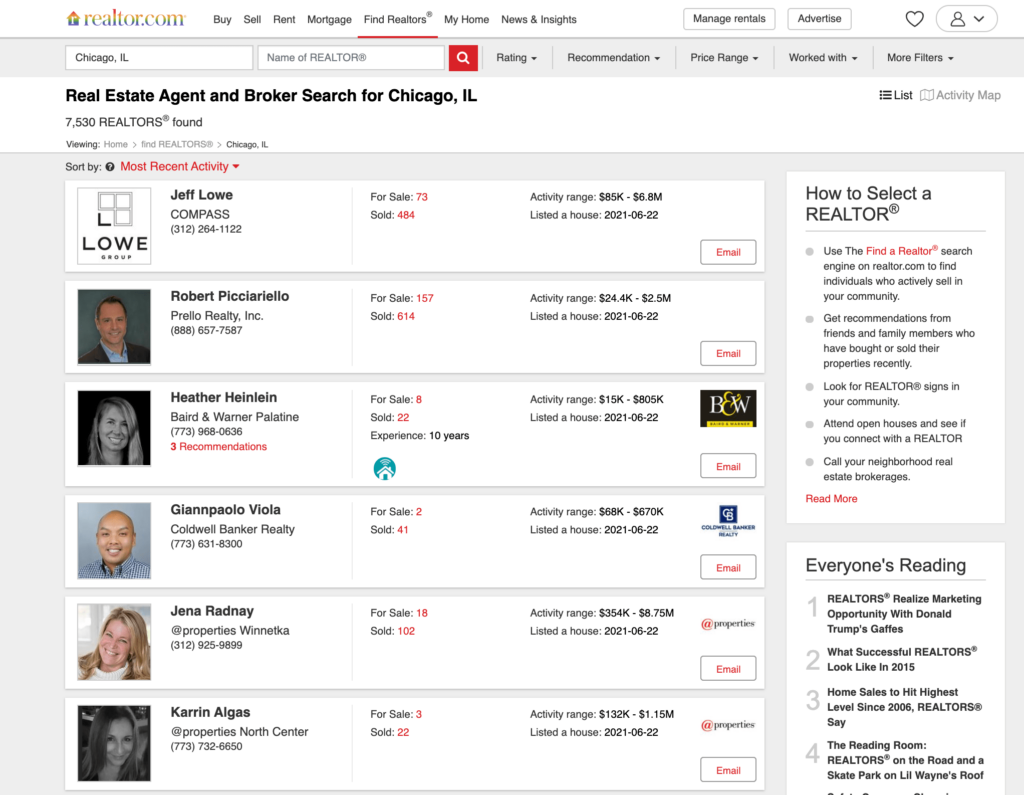

5. Find a Realtor

Next, you’ll want to find a real estate agent or Realtor to help you with your house search. These professionals will be able to take the weight of house hunting off your shoulders and provide additional assistance with negotiating prices, making offer letters, and closing on a home.

Easily search for Realtors near you who are knowledgeable about the types of homes you’re looking for and have the credentials you want when finding a reliable guide for the homebuying process.

6. Begin House Hunting

At this point, the thought of buying your first home is now very real. You’ll start searching for places that not only fit your lifestyle but improve it, which is an incredibly exciting experience.

On average, most people will tour about 10 houses (one per week) before deciding on a home. Using internet search tools, like the home search tool by Realtor.com®, will help prospective homebuyers get a better idea of what’s currently on the market and offer options they can share with their Realtor.

7. Make an Offer

Once you’ve found your dream home, it’s time to make a competitive offer on the property. This step will require you to negotiate a price with the seller and prove your worthiness for the home over other buyers. These tasks tend to be much easier with the help of a Realtor or agent, since you might find yourself in a bidding war for the property.

8. Set Up a Home Inspection and Appraisal

If all goes well during the offer stage and you successfully make a deal with the seller, then you will need to set up a home inspection and appraisal. While this seems like a minor step in the overall process, it’s actually critical to the deal and could save you money if the home is overvalued or is in need of repairs.

9. Finalize Your Mortgage Loan

The next step is to finalize your mortgage loan. This can either be done with the lender you were preapproved by or with a new one. The process, also known as the underwriting stage, will require that you submit proof of your income and job status, as well as any debt, taxes, and credit score information that could impact the loan. Once this is approved, you will be able to close on the house.

10. Close on the House

The final step to buying a house is to close on it. This is when there will be a transfer of all information regarding the title and deed to the house, as well as the money covering all upfront costs, so you will want to be well aware of everything happening in this stage to make sure nothing slips through the cracks.

Various professionals, such as your Realtor, an escrow officer, your mortgage lender, and more will be involved in this stage to make sure it runs smoothly. Then you’ll get the keys and become the proud owner of your first home.

Make Buying a Home Easier With Avail and Realtor.com®

There are a ton of resources available to help first-time homebuyers like yourself when navigating the steps to buying your first house.

If you’re still in the process of preparing your finances for the homebuying process, you can utilize the Avail CreditBoost* tool to work on improving your credit health by reporting your on-time rent payments to TransUnion each month. You can easily contribute to your FICO 9, FICO XD, and VantageScore credit scores while renting, helping you get that much closer to owning your first home.

Plus, Realtor.com® can help you every step of the way — with everything from deciding your home budget to getting connected with a mortgage lender and finding a trusted Realtor.

Find more first-time homebuying content designed specifically to help you as you work through the homebuying process.

*CreditBoost results may vary by individual.

The post First-Time Homebuying Checklist: Steps to Buying a House appeared first on Avail.

]]>The post The Pros and Cons of a Rent-to-Own Agreement appeared first on Avail.

]]>

The homebuying process requires first-time homebuyers to be well-prepared to take on the responsibility of owning a property. However, if you’re still on the fence about buying a house, then there’s another option you can consider — a rent-to-own agreement. Instead of buying right away, you can opt to rent the property for a given amount of time while still having exclusive purchasing rights. Many sellers and buyers have benefited from this type of agreement, but is this the right option for you?

To help you decide, we’ve explained what a rent-to-own agreement includes, as well as the main pros and cons to consider as a first-time homebuyer.

What Is Rent-to-Own?

A rent-to-own contract, also commonly referred to as a lease option agreement, occurs when a buyer is given the choice to rent the property for a specified period before buying it from the seller. It’s important to note that there are two types of this agreement: a lease option agreement and a lease-purchase agreement.

A lease option agreement offers the renter the option to buy the property from the owner once the lease ends, though they are not required to do so. If you find yourself not wanting to buy the property after renting it, you can simply move out without paying any additional fees to the seller.

On the other hand, a lease-purchase agreement will require the renter to buy the property from the seller once the lease ends. Choosing not to may result in a lawsuit or losing out on the money you’ve paid in rent that would have gone towards your down payment. A lease-purchase agreement should only be considered if the house offers what you’re looking for, a home inspection has been done, and you’re financially prepared to take on a mortgage once the lease ends.

Rent-to-Own: Pros and Cons Explained

The key to entering a rent-to-own agreement with confidence is to know exactly what you’re getting yourself into and understand this type of process. Here are the main pros and cons of rent-to-own agreements to be aware of.

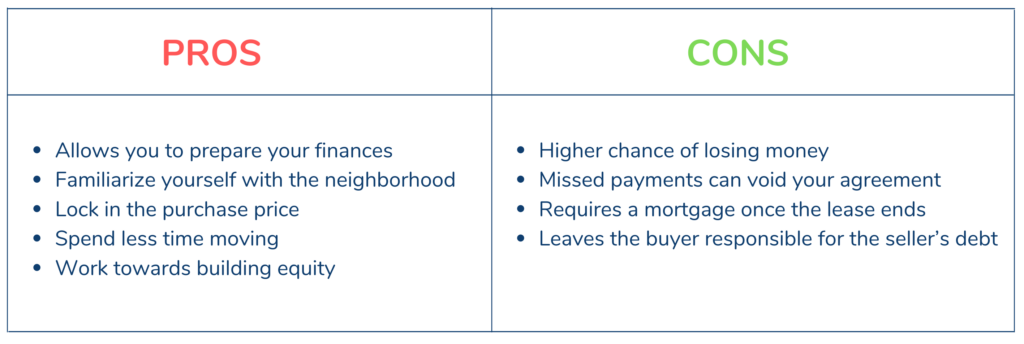

The Pros of Rent-to-Own

- Allows you to prepare your finances: A rent-to-own agreement is a great way to buy additional time if you’re working to improve your credit score or save a larger down payment while renting. Plus, you can easily report your on-time rent payments to TransUnion through CreditBoost* to contribute to your FICO 9, FICO XD, and VantageScore credit score. All you have to do is invite your landlord to Avail to set up your account.

- Familiarize yourself with the neighborhood: Rent-to-own can be the perfect way to see what the neighborhood is like and if it’s a good fit for your lifestyle before committing to homeownership.

- Lock in the purchase price: The housing market is constantly changing, meaning the original asking price could substantially increase at any moment. But with a rent-to-own agreement, you can lock in the original purchase price when you sign the lease.

- Spend less time moving: Since you’ll already be settled into the property, then you’ll no longer have to worry about hiring a moving company or packing up your belongings.

- Work towards building equity: Although you’re not technically building equity while renting, the payments you make will be contributing to the down payment for the home. Once you become the homeowner of the property, this will then contribute to your home equity.

The Cons of Rent-to-Own

- Higher chance of losing money: If you decide not to buy the property after signing a lease-purchase agreement, then you may lose money. Not only have you already paid the non-refundable option fee, but the seller can also keep the money you’ve paid in rent that was going to be used for your down payment.

- Missed payments can void your agreement: Failing to pay rent can result in the whole agreement being voided by the seller.

- Requires a mortgage once the lease ends: While rent-to-own agreements allow you to prepare your finances to own a home, be aware that if you don’t have a mortgage approved by the time the lease ends, then this can void the original agreement and leave you without a home.

- Leaves the buyer responsible for the seller’s debt: The way you handle your finances matters, but the same applies to the seller. The original property owner could stop making payments on their mortgage or local property taxes, which would leave you responsible for any outstanding debt that’s on the home once you become the new owner.

Is It Worth It to Rent-to-Own?

The benefits of a rent-to-own agreement make saving for a larger down payment or improving your credit score much easier than opting to buy a property right away. Even though you can always buy a home with bad credit, it’s best to wait until you have a credit score of at least 629 and have a lower debt-to-income ratio to avoid overpaying on interest.

That being said, a rent-to-own agreement should only be considered if you’re confident you’ll want to stay in the home for several years and can have a lawyer review the contract. A trusted Realtor and home inspector can also help you navigate the process to ensure you’re aware of any potential problems that may arise during the leasing period.

What Is Better: Rent-to-Own or a Mortgage?

Rent-to-own agreements are ideal for homebuyers still working to get approved for a mortgage loan with a lower interest rate. If you already qualify for your desired type of mortgage loan, then a rent-to-own agreement won’t provide you with much benefits.

Start the Homebuying Process With Realtor.com®

Now that you’re aware of the main rent-to-own pros and cons, the next step is deciding whether or not this route to homebuying is the best for you. Whether you prefer to buy a home right away or prefer to rent it out for a few months, Realtor.com® can help you find trusted Realtors in your area and connect you with a mortgage lender you’ll feel comfortable working with.

For more educational content on the homebuying process, check out our first-time homebuyers resource page. Get expert insights, downloadable checklists, and more.

*CreditBoost results may vary by individual.

The post The Pros and Cons of a Rent-to-Own Agreement appeared first on Avail.

]]>The post 8 Best Websites for House Hunting as a First-Time Homebuyer appeared first on Avail.

]]>

The homebuying process is an exciting journey to go through, but finding your perfect home may be difficult without the right resources. While you can always hire a Realtor to curate a list of homes for you, house-hunting websites can also identify properties for sale.

To help you decide which is the best website to buy a house, we outlined a list of the best house hunting sites to explore as a first-time homebuyer.

What Is the Best Website for House Hunting?

In order to find your dream home, you need to first know where to look. That’s why we outline the eight best house hunting sites to check out during your home search.

1. Realtor.com®

Realtor.com®, the official website of the National Association of REALTORS® (NAR), helps millions of first-time homebuyers across the nation find their perfect home. The platform has a user-friendly interface, making it easy to sort through available properties near you.

What makes Realtor.com® the best website for house hunting is its attention to the small details that matter to a first-time homebuyer. Each listing includes the most up-to-date information of the property from the Multiple Listing Service (MLS), as well as an overview on the home price over the years. You can also put money back in your pocket with the Buyer Cash Rewards program, which rewards homebuyers with 0.3% of the purchase price when buying a home with an agent on Realtor.com®.

Plus, if you’re still early in the homebuying process, you can get connected with a trusted mortgage lender to get preapproved for a mortgage.

2. Zillow

Zillow allows you to explore millions of listings online without the headache. Similar to Realtor.com®, the platform allows you to filter your online search, get connected with real estate professionals, and explore your mortgage options.

If you’re curious about the current valuation of a property, you can research the current Zestimate — an estimate of the current home’s market value — found on Zillow listings. The value itself takes data from the public, the Multiple Listing Service (MLS), and those submitted by users into consideration. However, the number can fluctuate depending on the housing market, how long it’s been listed, and more.

3. Homefinder.com

Homefinder.com, previously known as homescape.com, provides homebuyers with an interactive online experience to find available properties. You can easily find homes for sale, nearby foreclosures, off-market listings, and rent to own properties in one place.

The website’s capabilities are limited compared to other house-hunting websites, but it provides visibility into which homes are available that wouldn’t be found anywhere else.

4. Redfin

Redfin works to redefine the real estate market to favor buyers at every stage of the homebuying journey. The information shown on all of their listings includes information from the MLS, as well as information on transportation for those currently without a vehicle.

A Redfin Agent can help you navigate the process by walking you through showings, finding similar properties that fall within your budget, and can provide any insights you’ll need to know as a first-time homebuyer. The home seller typically covers the agent’s commission, but Redfin listings share how much of a percentage that will be. Plus, if you’re looking to buy a home in a hot housing market, you can see how many other homebuyers are looking at the exact same property you’re interested in.

5. Trulia

Trulia, a part of Zillow, is a great website to explore if you’re looking to find available homes in a specific area and see what other people in the community say about the neighborhood. Get local information or explore your mortgage options to see what type of loan you currently qualify for.

The platform has similar capabilities as Zillow, but there are a few differences worth noting. Unlike other sites, you can view LGBT Local Legal Protections to see how the LGBT community is being protected in the neighborhood. If you currently own a pet, each listing includes recent testimonials from local pet owners in the area for an idea on how the neighborhood will treat your furry friend.

6. Homes.com

Homes.com provides a simplified way to find for sale properties in your preferred location. The information on the listing is pulled from the MLS site and constantly updated to reflect relevant information. If you’re interested in learning more about the neighborhood by connecting with local experts, you can easily do so by contacting nearby real estate professionals familiar with the area directly on the site.

If you qualify for a Veteran’s Affairs loan (VA), you can even explore home loan options that can be applied to the home you’re interested in.

7. Estately

Estately is one of the newer house-hunting websites and recently became a part of Realogy in 2018. What makes them different from other sites is their focus on connecting homebuyers with the best real estate agents in any given area. All of the agents on their sites are on the buyer’s side and work on creating a simple homebuying experience for all.

When exploring their house listings, they’ll all include information on the property to ensure there’s full transparency in your home search. However, not all the information is updated right away, but there’s tons of information on the property you can discover on Estately.

8. ForSaleByOwner.com

Since 1999, ForSaleByOwner.com has provided resources to both sellers and buyers to make the homebuying experience seamless. When searching for a home online, you can sort through different types of properties such as single-family, condos, town houses, multi-family, and more.

If you’re considering buying a house without a Realtor, you have the option to contact the seller directly to navigate the process yourself.

Find Your Dream Home on Realtor.com®

The best website for house hunting ultimately depends on what type of home you’re looking for, how much information you want on the neighborhood, and other factors that are important to you. Regardless of which website you choose to utilize for your home search, Realtor.com® is ready to help you every step of the way.

Visit Realtor.com® to start the homebuying process today. Find a Realtor near you, get connected with a mortgage lender, and more.

The post 8 Best Websites for House Hunting as a First-Time Homebuyer appeared first on Avail.

]]>The post How Can I Qualify for a Mortgage With Student Loan Debt? appeared first on Avail.

]]>

If you’re worried you can’t get a mortgage because of your student loans, you’re not alone. With more than 44.7 million Americans with student loan debt, it’s becoming increasingly common for first-time homebuyers to already owe thousands of dollars when buying a home. However, you’ll need to be aware of how this debt can affect your ability to get preapproved for a mortgage.

Here are the ways mortgage lenders approach homebuyers with debt, as well as everything you need to know about how your student loans can affect the mortgage process.

How Are Student Loans Viewed By Mortgage Lenders?

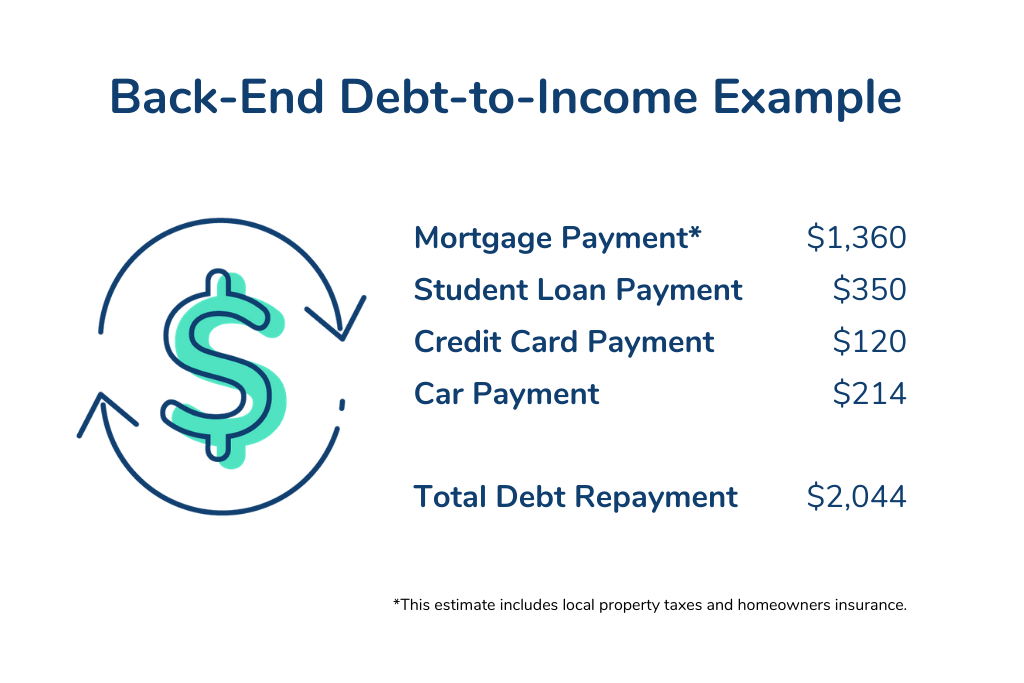

During the mortgage preapproval process, mortgage lenders primarily focus on your back-end debt-to-income ratio (DTI). Your back-end DTI ratio shows how much of your gross income goes towards any outstanding debt on your credit cards, as well as your student, personal, and auto loans.

To calculate your back-end DTI, your mortgage lender will need to add your monthly debt payments together and then divide the total by your gross monthly income. As a general rule, mortgage lenders prefer homebuyers to have a back-end DTI of less than 35%, but there are exceptions for those with a good credit score and strong payment history.

Do Student Loans Affect Debt-to-Income Ratio?

Your student loans directly impact your back-end DTI since this number shares how much of your income goes towards debt repayment. Homebuyers with a high back-end DTI typically can’t get a mortgage because of student loans, unless they have a down payment of at least 20% and a credit score over 629.

If you’re unsure of how to calculate your DTI, we’ve outlined an example below for more context. Let’s say you currently have the following debt breakdown per month:

Your total debt repayment per month would roughly sit at $2,044. This number would then be divided by your gross income (before taxes) to determine your DTI ratio.

Do Student Loans Affect the Mortgage Process?

While student loans alone cannot prevent you from buying a home, they can heavily impact how the homebuying process plays out. Aside from your back-end DTI ratio, student loans can also affect the following factors that play a role in your ability to buy your first home.

- Your credit score: In addition to your DTI ratio, mortgage lenders look at your current FICO® credit score to determine your creditworthiness and reliability as a borrower. If you’ve missed various payments towards your student loans, then this can decrease your overall credit score, which then disqualifies you from certain loan options.

- The size of your down payment: Saving a large down payment is no easy task, especially if your student loan payments account for most of your debt repayment. You’ll be required to put down anywhere from 3% to 20% (unless you apply for a VA or USDA loan), so anything less can result in you paying more for homeowners or private mortgage insurance.

- Mortgage loan options: There are various mortgage loan options available for first-time homebuyers, with some having stricter requirements than others. If you’re looking to apply for a conventional or a Federal Housing Administration (FHA) loan, then you may not get approved due to your high DTI ratio.

How to Qualify for a Mortgage and Buy a House With Student Loan Debt

If you’re buying a house with student loan debt, there are certain steps you can take to begin the homebuying process. Here are the four main ways you can prepare to buy your first house despite your student loans.

1. Know How Much You Can Afford

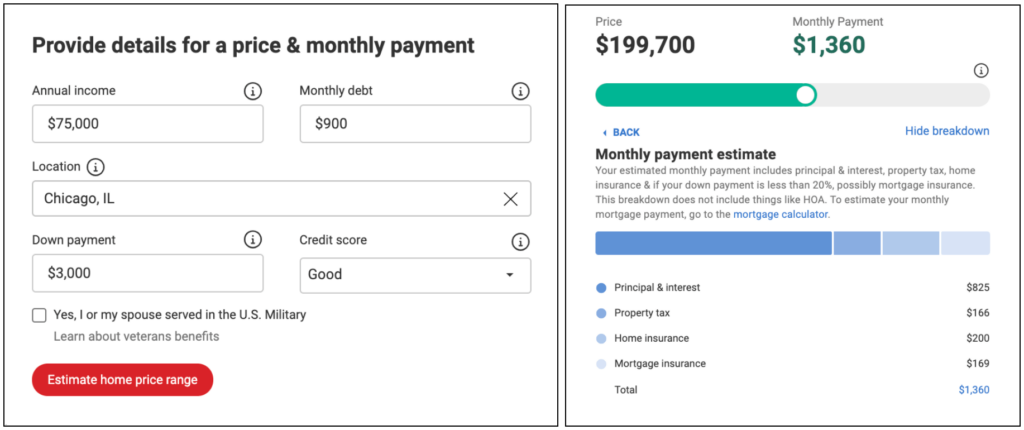

Before meeting with a mortgage lender, it’s advised to first determine how much you can afford on a home. You can use the Realtor.com® Affordability Calculator to see how much home you can afford based on your financial situation, as well as a suggested monthly payment for your mortgage.

The monthly payment estimate includes the principal and interest, property taxes based on your location, and possible home insurance you will need if you were to contribute a down payment of less than 20%.

Once you’ve determined your overall budget, you can then get connected with a trusted mortgage lender to explore your options and discuss your current finances further.

2. Increase Your Credit Score

Aside from your DTI ratio, mortgage lenders also pay attention to your credit score to see how much credit you owe, your payment history, and your overall credit mix. While you can always pay down your debt to increase your credit score, there are certain bills that affect credit scores that you can rely on to improve your credit health — like your monthly rent.

If you’re renting and need to improve your credit score, you can build your credit health by reporting your on-time rent payments to TransUnion for $3.95 per reported month through CreditBoost*. Not only can your on-time rent payments contribute to your FICO XD score (an alternate credit score that shows borrowers how you handle utility payments), but you can also build your VantageScore and FICO 9 credit scores all in one place.

The higher you can increase your credit score, the more likely a mortgage lender will preapprove you for a mortgage, even with student loan debt.

3. Build a Savings Fund

Mortgage lenders are more likely to preapprove you for a mortgage loan if you have a few thousand dollars in a growing savings fund, in addition to a good credit score. Having a savings fund ensures lenders you can still afford the mortgage payments, even if you suddenly experience a job change or have a high DTI ratio due to student loans.

The more cash you have on hand as a first-time homebuyer, the more likely mortgage lenders will want to work with you even if you don’t meet all the requirements for a certain loan.

4. Apply for Down Payment Assistance Programs

Most states offer down payment assistance programs for first-time homebuyers that are regularly accepted by mortgage lenders. You can always search online for local programs you may qualify for, but your mortgage lender can also find programs you can apply for to increase your chances of buying a home with student loan debt.

Some examples of assistance programs you can explore are local grants, deferred-payment loans, or low-interest loans, all of which vary in requirements depending on the mortgage lender and your location.

Know How Much You Can Afford With Realtor.com®

Student loan debt can impact your chances of qualifying for a mortgage loan, but with the right strategy, you can increase your chances of purchasing your first home in the near future. Whether that’s by paying down your existing debt or reporting on-time rent payments to improve your credit score, you can get that much closer to officially becoming a first-time homebuyer.

To properly prepare your finances to cover the upfront costs of buying a home, utilize the Realtor.com® Affordability Calculator to get insights into how much you can afford to pay on a home with your current student loan debt.

*CreditBoost results may vary by individual.

The post How Can I Qualify for a Mortgage With Student Loan Debt? appeared first on Avail.

]]>The post When Is the Best Time to Apply for a Mortgage? appeared first on Avail.

]]>

Getting preapproved for a mortgage is easier than ever now that you can explore different mortgage rates online and easily get connected with a mortgage lender. But knowing exactly when to apply for a mortgage as a first-time homebuyer may not be so clear, making it harder to know exactly when to begin the homebuying process.

That’s why we’ve shared expert insights on when you should apply for a mortgage, as well as things to avoid that can make it harder to get approved by your mortgage lender.

When Should I Apply for a Mortgage?

As a first-time homebuyer, you’ll need to meet certain requirements to both qualify and get approved for your preferred mortgage loan. Before submitting your application, here are five things you should have prepared to go into the approval process with confidence:

1. A Low Debt-to-Income Ratio

According to the National Association of REALTORS® (NAR), the biggest reason mortgage lenders rejected a homebuyer’s application this past year was due to their debt-to-income ratio. Your debt-to-income ratio (DTI) looks at how much of your gross income goes towards debt repayment on a monthly basis. A favorable DTI ratio is generally 36%, but the number varies depending on the type of mortgage loan you’re applying for.

Mortgage lenders refrain from extending additional credit to homebuyers if a majority of their monthly income goes towards paying off their debt. To avoid that from happening to you, try to pay off as much of your debt as possible before meeting with a loan officer to bring down your DTI ratio. Paying off a credit card or a portion of your student loan debt are great ways to bring down your debt and allow more of your income to go towards your down payment for a home.

2. A Qualifying Credit Score

Mortgage lenders look at your FICO® credit score for two reasons: to gauge your reliability as a borrower and determine if you qualify for the mortgage loan you want. Although buying a home with bad credit is possible, you should always try your best to have a credit score over 629 in order to qualify for a mortgage with a lower interest rate.

Improving a low credit score is generally easy to do, so long as you pay your bills on time and avoid opening up new lines of credit. If you’re looking to build your credit health in addition to paying down your existing debt, you can utilize platforms like CreditBoost* to report your on-time rent payments to TransUnion and contribute to your FICO 9, FICO XD, and VantageScore credit scores.

Currently renting? Invite your landlord to Avail to start reporting your on-time rent with CreditBoost.

3. A Large Down Payment

Saving for a down payment can be the hardest part of the homebuying process, since you’ll have to put down anywhere from 3% to 20%, depending on your mortgage loan. That being said, some loans, such as those provided by the VA and USDA, don’t require a down payment at all. Instead the mortgage lender will require that you purchase private mortgage insurance (PMI) in order to accept the application.

A larger down payment can be extremely beneficial if you have a low credit score or higher DTI ratio because it can increase your chances of getting approved even if you don’t meet all the requirements. To save for a down payment while renting, you can cut down on miscellaneous spending or create a savings fund specifically designed for the costs of buying a home.

4. A Stable Income

Mortgage lenders refer to your income documents — pay stubs and tax documents — to determine how much you can afford to pay on a home and confirm you’ve had a consistent stream of income for the past two years.

Generally, you should be able to afford a house that costs two to three times your gross monthly income. That means that if you currently make $75,000 annually, then homes costing anywhere from $150,000 to $225,000 will fall within your price range.

Because your income plays an important role in determining whether or not you will be able to make your monthly mortgage payments, it’s advised that first-time homebuyers who recently started at a new job wait a few months, or even years, before applying for a mortgage. However, if you’re set on buying a home sooner, then you’ll need to prove you’ve been on a stable career track with a growing salary to put your lender at ease. Those who were recently discharged from the military can provide a waiver to prove their consistent income.

5. Timing

The beginning of the month is usually the best time to meet with a mortgage lender. Mortgage lenders fit in the most applications for approval during the first week, while the middle of the month is used to gather all the documentation needed to complete the process.

Although the time of the month has no effect on your chances of getting approved for a loan, it does ensure you find a mortgage lender that can meet your needs and properly help you through the process.

Don’t have a mortgage lender? Get connected with trusted professionals on Realtor.com® to begin the preapproval process in no time.

What Not to Do After Applying for a Mortgage

Now that you’re ready to apply for a mortgage, it’s important to know what actions to avoid in order to save yourself from being denied a loan. Here are four things you should not do after submitting an application for a mortgage:

- Avoid changing jobs: Changing jobs either before or during the mortgage process could interfere with getting approved for a mortgage. This is especially true if you move to a lower-paying position or move into a less stable industry.

- Avoid large purchases like a new car: Financing new debt obligations increases your DTI and decreases your credit score due to hard inquiries — all of which can hurt your mortgage application in the long run.

- Avoid co-signing other loans: Even if you’re not responsible for the payments on the loan, this new debt will be added to your credit report and your DTI ratio — forcing you to restart your own mortgage approval process.

- Avoid closing existing credit card accounts: Having less credit during the homebuying process seems like a good idea, but this can actually substantially decrease your credit score in a very short period of time.

Begin the Preapproval Process With Realtor.com®

The best time to apply for a mortgage is when you’re ready for homeownership and have prepared your finances to take on a home loan. Whether that’s by lowering your DTI ratio or building your credit health by reporting on-time rent, taking the right steps early on can increase your chances of getting approved. If you’re still in need of a mortgage lender, you can easily get connected with trusted mortgage lenders in the industry through Realtor.com®.

Create an account or log in to invite your landlord to start contributing your on-time rent payments to your FICO 9, FICO XD, or VantageScore credit scores with CreditBoost.

*CreditBoost results may vary by individual.

The post When Is the Best Time to Apply for a Mortgage? appeared first on Avail.

]]>The post 6 Reasons Why You Should Hire a Realtor appeared first on Avail.

]]>

Homebuyers have historically relied on Realtors to lead the homebuying process, but now that it’s easier to find available homes online, is hiring a Realtor still worth it? Although you’re not legally not required to work with a real estate professional to buy a home, there are various reasons why you should for a positive homebuying experience.

In this article, we’ve outlined the main reasons why you should hire a Realtor to help you as a first-time homebuyer, along with the tools to help you find the right Realtor for you.

What Are the Main Benefits of Using a Realtor?

The purpose of a Realtor is to help you find your perfect home with as few hiccups as possible. Whether that’s searching an extensive list of for sale properties or negotiating a great deal with the seller, your Realtor is there to spearhead the overall process on your behalf.

In addition to alleviating time-consuming tasks, here are the six benefits that come with working with a real estate professional:

1. Discover Hidden Property Listings

While you can always search online for available homes for sale, the National Association of REALTORS® (NAR) discovered more than half (53%) of American homebuyers experienced the most difficulty with finding the right property when beginning the process on their own.

That fact alone is a good reason why all homebuyers, especially first-time homebuyers, can benefit from a Realtor since they have access to internal resources with a list of homes that have yet to hit the market. From the Multiple Listing Service (MLS) to “off-market” listings, they can find homes that match your criteria in faster time.

Pro tip: Choose a Realtor specialized in helping first-time homebuyers to ensure your needs are met from the beginning.

2. Educate You on the Homebuying Process

According to the NAR, homebuyers (especially those 30 years and younger) in the past year have benefited from hiring a Realtor since they were able to better understand the purchase process.

Realtors must undergo rigorous training to understand the homebuying process inside and out. Some also receive specialized training in various areas that can help them provide more personalized assistance.

A few examples of trainings they can earn are:

- Military Relocation Professional (MRP)

- Real Estate Negotiation Expert (RENE)

- At Home With Diversity (AHWD)

From the best type of mortgages to steps to buying a home with bad credit, you can approach buying your first home with confidence by having a trained professional guide you through each step. If you’re unsure on where to find one, The Realtor.com® Find a Realtor tool allows you to search through their extensive network of trusted Realtors across the nation, which can be filtered by location and credentials.

3. Source Lawyer-Approved Contracts

If there’s one thing you can expect from the homebuying process, it’s tons of paperwork from getting preapproved for a mortgage to officially closing on a home. Buying a home without a Realtor leaves you responsible for hiring a real estate lawyer to review all the agreements and decipher them on your own.

A huge reason why homebuyers hire a Realtor is to reduce the chances of landing in a legal issue with the buyer and to have someone that’s knowledgeable on real estate laws. If this is something you’re concerned about, then it’s best to choose a Realtor that can handle and review all the legally-binding agreements.

4. Point Out Red Flags in a Property

Unless you have a background in plumbing or home inspections, it’s very easy to miss red flags that need to be addressed to the seller right away.

Since a Realtor’s primary job is to discover homes that fit a first-time homebuyer’s criteria, they know exactly what to look for when viewing homes. Furnace issues, leaks, roofing problems, mold, and insect issues can all be easily identified by a Realtor, which can then be raised during negotiations to reduce the overall cost of the home.

5. Superior Negotiation Skills

The homebuying process almost always includes negotiations, and with the right Realtor, you can get a better deal on your dream home. A few expenses that can be negotiated down are closing costs, home warranty premiums, repair costs, and cosmetic updates to the home.

A Realtor, especially those with RENE certifications, can negotiate on your behalf to bring down the overall cost of buying a home and even fight for additional incentives to take advantage of — like keeping recently added appliances or having the seller cover the closing costs.

6. Refer Trusted Professionals

When purchasing your first home, there will be a good handful of professionals you’ll need to work with to keep the process moving. For example, you’ll most likely need help from a:

- Mortgage lender

- Real estate attorney

- Title insurance company

- Appraiser

- Insurance agent

- Title and escrow specialists

- Home inspector

- Pest Inspection company

You can spend some time finding potential contractors to work with, or you can hire a Realtor, who often has reliable and trustworthy people they can refer you to. The more referrals you can utilize, the less time you’ll have to spend online searching for people that can help you right away.

Is Hiring a Realtor Worth It?

Many first-time homebuyers agree that hiring a Realtor during the homebuying process was worth it. Out of all the homeowners that decided to purchase a home through an agent so far in 2021, nine out of 10 homebuyers would use their agent again or recommend their agent to others according to the NAR.

While you can still begin your search online, hiring a Realtor to take ownership of finding potential homes to view ensures you spend less time searching and more time preparing for the big move.

Why Hire a Realtor Explained

Buying your first home is an exciting milestone to accomplish, and having the right team by your side can limit the amount of time (and stress) that can sometimes come from this process. If you’re unsure how to find a Realtor, you can always request local referrals, search on Facebook, or utilize the Realtor.com® Find a Realtor tool.

Want to learn more about the homebuying process? Check out our growing library of first-time homebuyer resources full of educational content that answers all your questions on buying a home and more.

The post 6 Reasons Why You Should Hire a Realtor appeared first on Avail.

]]>The post Is Buying a House Without a Realtor a Good Idea? appeared first on Avail.

]]>

Buying a house without a Realtor is possible, but it may not be the best route to take. First-time homebuyers choose to work with a Realtor to guide them through the process and handle the paperwork required to close on a home. By not hiring a Realtor, there’s a higher chance of the homebuying process taking longer or landing in a tricky situation.

So before committing to buying a home without professional help, let’s first review the purpose of having a Realtor and why working without them is a bad idea.

What Is the Purpose of Having a Realtor?

A Realtor — a real estate agent that’s an active member of National Association of REALTORS® (NAR) — acts as a liaison between you (the buyer) and the person selling the property you’re interested in.

While you’re responsible for getting preapproved for a mortgage, a Realtor can find homes that match what you’re looking for, negotiate a competitive offer on your behalf, and decipher complex paperwork.

Do I Need a Realtor to Buy a House?

Working with a Realtor to buy a home is not required, but first-time homebuyers can greatly benefit from the services they offer. In addition to finding available homes to consider, Realtors can guide you through each step of the process.

Occasionally, homebuyers choose to not work with a Realtor to save money on the costs of buying a home. But the seller is usually responsible for this cost, not the homebuyer, so forgoing assistance from experts can only make buying a home that much harder.

If you’re unsure on how to choose a Realtor as a first-time homebuyer, you can request local referrals from your network or visit sites like Realtor.com® to get connected with trusted Realtors near you.

Why Buying a House Without a Realtor Is a Bad Idea

Working without a Realtor comes with a few disadvantages. Here are the main four to consider before committing to buying a home without the help of a Realtor:

1. Less Market Knowledge

Realtors have access to sites like the Multiple Listing Service (MLS), which have millions of real estate property listings to choose from. They also have more visibility into “off-market” listings — for sale homes that aren’t on the MLS or marketed by the seller.

When attempting to buy a home for the first time, you want plenty of help with not only finding your perfect home but helping you craft a competitive offer that will increase your chances of buying the house faster.

2. Large Amounts of Paperwork

Unless you have a background in real estate, handling the homebuying process alone can increase your chances of forgetting an important step or landing in a sticky legal situation.

While homebuyers will typically hire a lawyer that specializes in real estate law for help, a Realtor can also walk you through the closing paperwork so the process is clearly defined.

3. Handle Negotiations Alone

Handling negotiations on your own can result in you paying more for the home or having your offer dismissed by the seller entirely. Not to mention that this process can be extremely stressful and difficult to navigate properly. To avoid that happening, you can hire a Realtor with strong negotiation skills to do the heavy lifting on your behalf.

Realtors are often required to be well-versed in negotiating, with some holding a special credential known as the Real Estate Negotiation Expert (RENE) certification. This training provides Realtors with exclusive tools and skills so they can be strong advocates for their clients throughout every step of the homebuying process.

Easily find Realtors with RENE credentials by using the Realtor.com® Find a Realtor tool. Simply filter your search by clicking “Add Credentials” and entering the city you’re based in to get started.

4. Limited Connections for Help

A Realtor often has hundreds of connections you can utilize to make the homebuying process easier, like mortgage lenders, home inspectors, contractors to renovate your home, and more. Choosing to refrain from hiring a Realtor will often add more time to the process and take up more of your time as well.

How to Buy a House Without a Realtor

If you’re still considering buying a home without a Realtor, then there are steps you’ll need to take to ensure the process goes smoothly.

Here are the six main steps you’ll need to follow to properly buy a house without professional help:

1. Get Preapproved for a Mortgage

As a first-time homebuyer, the first step you’ll need to take is getting preapproved for a mortgage. A mortgage preapproval letter lets you know how much you can afford when it comes to your down payment and monthly mortgage payments based on your financial situation.

If you’re unsure of the best type of mortgage for you, you can ask your mortgage lender which options you qualify for based on your credit score, debt-to-income ratio (DTI), employment history, and overall income.

2. Research Your Neighborhood

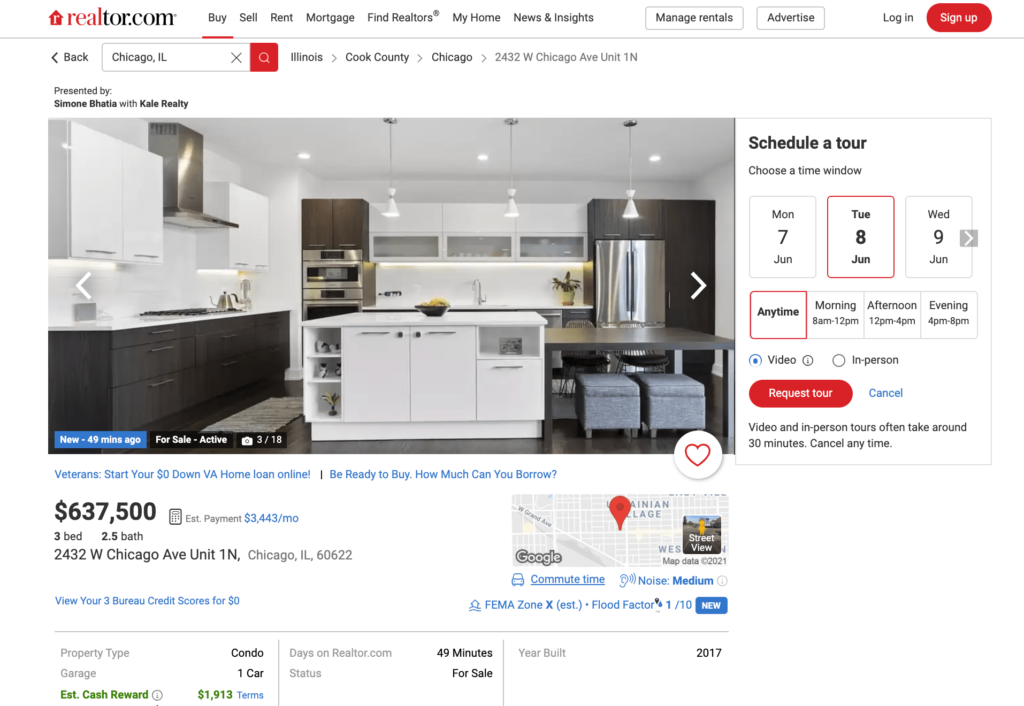

Helpful sites like Realtor.com® can help you discover homes that are for sale and are close to a specific address, educational institution, or based in a preferred neighborhood.

Each property listing includes helpful information, such as the property details, insights into how much your monthly payment may be, veteran and military benefits, nearby schools, and more. Once you find a property you’re interested in, you can easily schedule a video or in-person showing with the seller to view the property.

3. Request a Seller’s Disclosure

Before making an offer on a home, most real estate experts advise requesting a seller’s disclosure statement. A seller’s disclosure outlines all remodeling work that’s been done on the following: structural issues, issues with utilities, the removal of lead paint, damage from wood-boring insects, toxins in the soil, and mold or water damage.

Not all states require sellers to disclose these property issues unless directly asked by the buyer, so it may be worth researching your state’s disclosure laws and then compiling a list of questions to ask the seller during the initial showing.

4. Make an Offer

Crafting a competitive offer letter can increase your chances of landing your ideal home during a hot housing market. You’ll want to be sure to include the following information in your offer letter if you want to be considered:

- The full legal names of all parties purchasing the property (i.e. a spouse, partner, or family member)

- The amount you’re offering for the home

- Specific conditions you’re requesting be completed before the sale is processed

- Requested seller concessions (discount points or cash towards closing costs)

- A copy of your mortgage preapproval letter

- The date you expect to close

- The date you want to move into the home

- A deadline for the seller to respond to your offer

5. Hire a Lawyer and Home Inspector

If you’re buying a home without a Realtor, hiring a real estate lawyer and home inspector can ensure nothing falls through the cracks before getting the keys. A lawyer can review any paperwork you’re expected to sign and immediately escalate anything that requires your attention.

A home inspector, on the other hand, can identify any issues impacting your plumbing, heating, home build, and more. They can also let you know if anything was missed on the seller’s disclosure statement that you previously requested from the original property owner.

6. Finalize Home Financing and Closing

The closing process begins once your mortgage underwriting is finished, the appraisal of the home is completed, you’ve reached an agreement with the seller, and you’re ready to sign the final paperwork.

You’ll then receive a closing disclosure, which shares information on the terms of your mortgage loan, your closing costs, and more. Once you’ve signed the final paperwork, congratulations are in order because you’re finally a homeowner!

Find a Trusted Realtor on Realtor.com®

Buying a house without a Realtor is a route few homebuyers take, but it can be done with the right steps. Even so, hiring a Realtor allows you to work closely with seasoned experts in real estate that can help you feel peace of mind when purchasing your first home.

Regardless of your decision on whether or not to work with a Realtor, Realtor.com® can be your trusted resource on the entire homebuying process. From finding a Realtor to getting preapproved for a mortgage, there’s a team of homebuying experts ready to help you every step of the way.

The post Is Buying a House Without a Realtor a Good Idea? appeared first on Avail.

]]>The post 12 Costs of Buying a Home First-Time Homebuyers Should Save For appeared first on Avail.

]]>

When preparing for the homebuying process, it’s important to know how much it can actually cost to buy a house. While some costs of buying a home are more apparent than others, you’ll want to account for both the obvious and the hidden costs when planning to buy a house as a first-time homebuyer.

To help you feel prepared every step of the process, here are the main costs associated with buying a home.

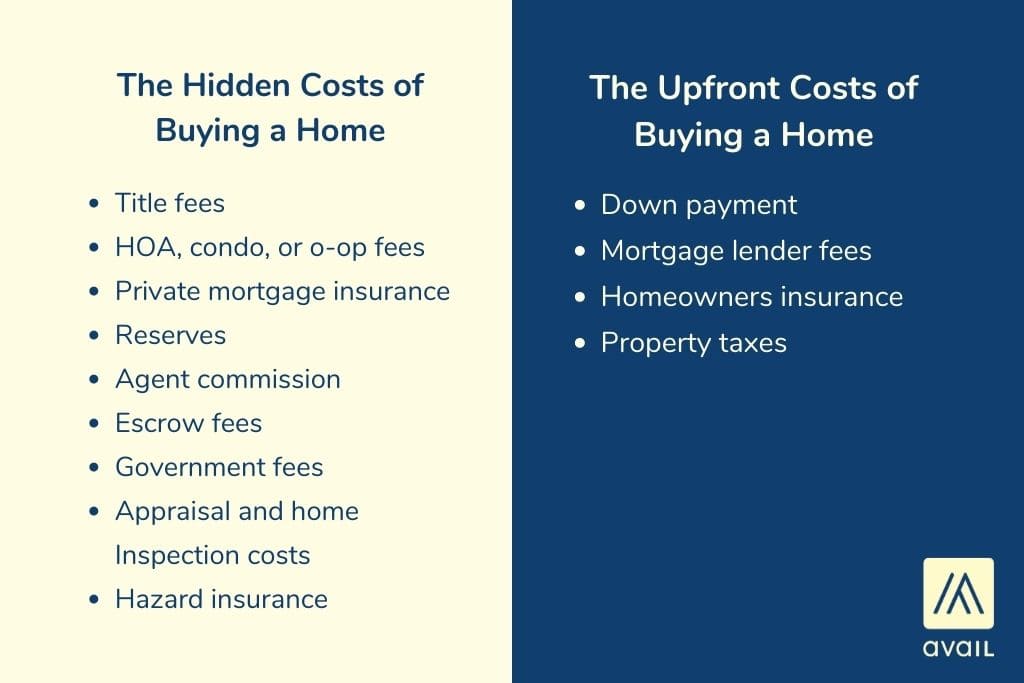

Upfront Costs of Buying Home

There are multiple upfront costs when buying a home, including the down payment, mortgage lender fees, property taxes, homeowners insurance, and more. Here are the main costs to be aware of:

1. Down Payment

Your down payment will be the biggest upfront cost you’ll be responsible to cover during the homebuying process. The minimum down payment requirement varies depending on your mortgage lender, which could be anywhere from a minimum of 3% to 10% of the cost of the house.

For a better idea on how much you’ll be required to put down, here are the down payment minimums for the main mortgage loans for first-time homebuyers:

- Conventional loan: 3%

- Federal Housing Administration loan: 3.5% to 10%

- Veteran Affairs loan: 0%

- U.S. Department of Agriculture loan: 0%

- Adjustable-Rate loan: 5%

2. Mortgage Lender Fees

Mortgage lender fees encompass everything you will need to pay during the preapproval and closing process. The origination fee, underwriting fees, and application fees are all included in the final cost.

An origination fee goes directly to the bank or mortgage lender for the creation of the loan, which ranges from 0.5% to 1% of the mortgage amount. If you plan on putting down cash for your home, then this cost may be higher for smaller loans.

Underwriting fees cover the work of going through and approving the mortgage application. These fees are non-negotiable and are specific to the mortgage lender’s or bank’s policies, ranging anywhere from $400 to $900 dollars for this process alone.

These costs will be outlined in a Loan Estimate from your mortgage lender given within three days of applying for a loan, far before you start the closing process if following our homebuying timeline. This includes your estimated interest rate, monthly payment amounts, the total closing costs for the loan, estimated insurance and tax costs on the loan, and how these costs may change in the future.

This loan estimate will also give you an idea of if your loan has any penalties for paying off your mortgage early (if applicable) or if the loan has a negative amortization feature.

Find a mortgage lender who can offer you competitive mortgage rates and facilitate the preapproval process by visiting Realtor.com®.

3. Homeowners Insurance and Property Taxes

Another upfront cost will be your homeowners insurance and property taxes. You will need to pay the first six months of your property taxes and the first 12 months of homeowner’s insurance at closing.

Hidden Costs of Buying a Home

Once you’ve saved enough for the more expensive costs of buying a home, the next step is to prepare for hidden costs that will pop up during the closing process.

1. Title Fees

These fees include costs associated with the house’s title — a legal document proving the rights of ownership and the right to sell. These include a one-time fee for searching for the title, the title settlement, title insurance, and a title insurance binder (a temporary form of title insurance that covers the buyer and seller during the transfer).

The total cost of the title fees can vary depending on which title service you go with and your ability to negotiate a lower cost.

2. HOA, Condo, or Co-Op fees

Homes that are part of a condominium association, a co-op, or the Homeowner’s Association (HOA) require homeowners to pay various group member fees.

These fees can range anywhere from $50 to $800 depending on the association and location.

3. Private Mortgage Insurance

If your mortgage lender requires private mortgage insurance (PMI) because of a smaller down payment, you will need to budget for this monthly cost as well. While not all mortgage loans require a PMI, it’s likely that you will need to add this to the overall cost of buying a home. Mortgage insurance is required by all FHA and USDA loans, or if you’re putting less than 20% down on a conventional loan.

At closing, you could be required to pay a mortgage insurance premium at closing and a monthly premium after you buy the home. This is dependent on the PMI provider as well — in some cases, you can package these costs into your monthly PMI payments, though this can affect the amount you will need to pay on your mortgage each month.

4. Reserves

A homebuyer’s reserves refer to the amount of money the buyer will need to have in their bank account after paying all closing costs and the down payment. This is not a cost per say, but an amount of money that you will need to have set aside in order to close on the house and leave your mortgage lender confident that, after all the upfront costs are paid, you will still be able to make your mortgage payments.

Some mortgage lenders will require that you have at least “two months of reserves”, which translates to enough money to cover at least two months of mortgage payments.

5. Escrow Fees

Escrow fees come from opening and maintaining an escrow account that will hold the money for the home while the deal is being finalized. This account is typically managed by your mortgage lender.

Your escrow account will also continue to serve as a savings account for your monthly mortgage payments, property taxes, and homeowner’s insurance payments. This makes it easier for you to contribute money specifically to your continuing home costs.

6. Government Fees

There will be taxes associated with transferring the title from the seller to the buyer and, depending on the state and county where the home is located, can be as high as 2.7%. Either the buyer or the seller can pay the transfer taxes, and can be negotiated between the two parties.

Recording fees are charged by the government when recording the purchase or sale of a piece of real estate. This information will be filed in your county’s public land records.

7. Appraisal and Home Inspection Costs

When buying a home, you will need to be in charge of finding an appraiser for the home to make sure that the value of the home is correct. According to the National Association of REALTORS® (NAR), this can cost between $300 to $500 but could save you money if the cost for the home is lower than what it’s being sold for.

Home inspection fees, including pest inspection, will make sure the house is in good condition and ready to be sold. The NAR states that this can cost about $300 to $500 to get done, but it will ensure that you don’t buy a home in need of massive repairs or one that is plagued by termites.

8. Hazard Insurance

If you’re in an area where you need to purchase hazard insurance, this will be an extra cost to be aware of. If your home is determined to be in a “high risk” region when it comes to floods, earthquakes, wildfires, severe storms, or any other natural disaster, you will be required to get hazard insurance, which can cost between 0.25% to 0.33% of the home’s value for a year-long policy.

9. Agent Commission

While the seller of the home normally pays for the real estate agent’s commission, there are times when the buyer will be responsible. Make sure you inquire into who will be paying the agent (if one was used) so you don’t get saddled with a cost you weren’t prepared for. This can cost around 3% of the sale price for each agent included in the transaction.

How to Save for a House With the Help of Realtor.com®

With these extra costs and fees, it’s important to include everything in your budget. As a first-time homebuyer, this may seem like a daunting task, but knowing every cost associated with the homebuying and closing process will help you save wisely.

If you’re not sure as to whether or not you want to continue to rent or buy, you can use the Realtor.com® Rent vs. Buy calculator. This will help you decide if you should continue to keep saving and building your credit for a home or if you have the necessary budget to move forward in the homebuying process.

To learn more about what you need to know when it comes to buying a house, check out our First-Time Homebuyer Resource hub.

The post 12 Costs of Buying a Home First-Time Homebuyers Should Save For appeared first on Avail.

]]>The post The Pros and Cons of Buying a House as a First-Time Homebuyer appeared first on Avail.

]]>

Owning a home has plenty of advantages that you normally wouldn’t get with renting, especially as a first-time homebuyer. But considering how big of an investment purchasing a home is, it’s normal to still be on the fence on whether to rent or buy.

To help you decide, here are the in-depth pros and cons of buying a home and the tax deductions you may qualify for as a first-time homeowner.

Rent or Buy a Home: Pros and Cons of Buying a House

Before purchasing a home, most experts recommend being well-informed on the advantages (and disadvantages) of homeownership first.

Let’s go through the top pros and cons of buying a home you should consider early on.

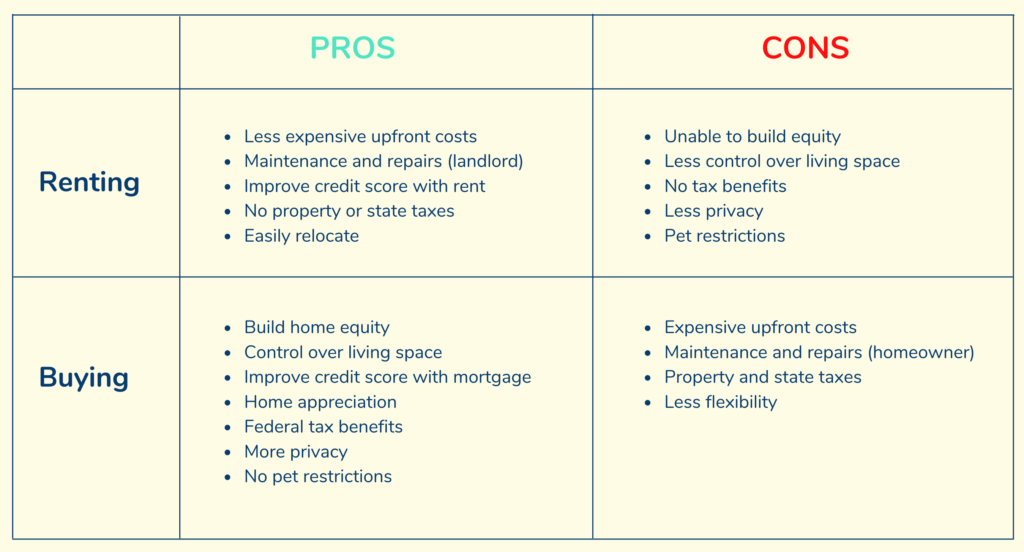

Pros of Buying a House

There are various advantages to buying a home instead of renting, such as the chance to build home equity and benefits of not having to deal with a landlord. However, there are more ways buying a home can benefit you right away, including:

- Build home equity: Home equity represents the amount of your home that you own, which increases with each on-time mortgage payment. As you pay down your mortgage over time, you begin building equity that can later be used to borrow home equity loans or lines of credit.

- Control over living space: Unlike renting, you’re able to renovate your home how you please so long as it abides by any laws set by the Homeowners Association (HOA) or your mortgage lender, if applicable. Updates to your home can also increase the overall value of your property, or even be tax-deductible if considered a medical expense.

- Improve credit score: While renters can now report on-time rent payments through platforms like CreditBoost, you can also build your credit by paying off your mortgage. Your credit score typically goes down a few points when taking out a home loan, but this can be built back up.

- Home appreciation: More often than not, your home will increase in value over time, making it a strong investment for yourself versus a landlord or property management company.

- Federal tax benefits: Purchasing a home can require a large down payment, but homeowners can qualify for more tax deductions than renters. Both states and the federal government have deductions homebuyers can qualify for to offset the costs of owning.

- More privacy: You’ll no longer have to worry about a random visit from your landlord, since homeowning allows for more privacy compared to renting.

- No pet restrictions: If you currently own a pet or are planning to, then you won’t need an outsider’s approval to have them in your home. This is especially beneficial if you own a pet breed that’s normally excluded from most rental properties.

Cons of Buying a House

While buying a home has tons of benefits in the form of tax deductions and renovation flexibility, there are a few cons to be aware of as a first-time homebuyer:

- Expensive upfront costs: The costs of buying a home can be more expensive than renting, but this depends on the type of home loan you get preapproved for and your financial situation. On top of the down payment, you’ll need to cover additional expenses like closing costs and HOA fees, if applicable.

- Handle maintenance and repair: When renting a property, your landlord or a property management company is responsible for any sudden maintenance or repairs. Buying a home means you’ll be responsible for fixing any repairs and necessary maintenance.

- Property taxes: As a homeowner, you’ll be responsible for any property taxes in your city or county. The amount you’ll pay each month varies on the tax rate in your area.

- Less flexibility: Buying a home is a huge investment that’s suited for homeowners planning on staying somewhere for more than two years. Selling your home in the first year of owning can take months to complete and cost additional money if you still owe a majority of your mortgage.

Renting vs. Buying a House Comparison

Now that you’re familiar with the pros and cons of buying a home, the next step is comparing buying vs. renting. While there are some similarities between the two, in most cases, there are more benefits to buying a home instead of renting.

You should also see what your chances of getting preapproved for a mortgage are compared to getting approved for a rental lease. Unlike renting, mortgage lenders look at your credit score, debt-to-income ratio (DTI), current income, employment history, and any outstanding liabilities when determining your reliability to pay a mortgage.

If you have a low credit score or only qualify for home loans with high-interest rates, then that’s an additional factor to consider when making your decision to rent or own a home.

What Are the Tax Benefits of Owning a Home?

Most states offer their own set of tax benefits for homebuyers, but there are federal tax deductions you may qualify for as well. Some examples of these include:

- Property tax deduction: The IRS allows homeowners to deduct a total of $10,000 in state and local property taxes, so long as they’re married or filed their taxes jointly. For those that are single or filing separately, you can deduct up to $5,000.

- Home equity debt: When borrowing your home’s equity to improve your home, the interest you pay each year can be tax-deductible. You’ll need to itemize deductions when filing your taxes using an IRS Form 1040.

- Home office expenses: If you use part of your home for business purposes, then you may be able to take advantage of the home office tax deduction. An example of this would be if you use an extra room in your home to run your business or keep stock of inventory.

- Renewable energy tax credits: Thanks to the federal solar tax credit, also known as the investment tax credit (ITC), you can deduct 26% of the cost of installing a solar energy system from your federal taxes.

- Medically necessary home improvements: If you, your spouse, or any of your dependents require home improvements to be made due to medical necessity, then this can be considered a medical expense. However, you’ll need to go through extensive screening to ensure you qualify for this expense during tax season.

Weigh the Pros and Cons of Buying a House

The process to buy a house as a first-time homebuyer can be overwhelming at first, but having the right team by your side can make it less stressful. By knowing the pros and cons of buying a home, you’re one step closer to knowing which is the best option for you.

If you’ve decided buying a home is right for you, the next step is meeting with a mortgage lender to get preapproved for a home loan. Visit Realtor.com® to begin the process of getting preapproved for a mortgage and get connected with a trusted mortgage lender that can walk you through every step.

Still unsure of the homebuying process? Check out more educational articles catered for first-time homebuyers to help you feel confident every step of the way.

The post The Pros and Cons of Buying a House as a First-Time Homebuyer appeared first on Avail.

]]>