The post Landlord Tax Documents: Everything to Know for Tax Season appeared first on Avail.

]]>

When becoming a landlord, you will be responsible for reporting your rental income each tax season to avoid costly fees, fines, or penalties. To do this, you will need to file the relevant tax documents. In most cases, a certified public accountant (CPA) can outline what documents you need to submit.

We spoke with Riley Adams, CPA, the owner of Young and the Invested and certified public accountant, to get a general understanding of the main tax documents landlords use.

What to Know About Tax Documents for Landlords

The Internal Revenue Service (IRS) requires landlords to report rental income through the proper tax forms, which can vary depending on your situation. Examples of these forms include Form 1099, Form 1040 or 1040-SR, and Form 8825.

Each form outlines different information, so it’s best to work with a certified tax accountant if you’re unsure how to file your rental property taxes correctly. Failing to file the correct documents can result in costly penalties, fines, interest, or worse, if taken far enough. This is especially true with the recent 1099 requirement from the IRS that will require landlords to report rental income over $600 collected through payment processing platforms.

“If you receive rental payments via an electronic payments processor [that] exceed $600 during the year, you should expect to receive a 1099-K form in the mail, digitally or possibly both,” shares Riley Adams. “If you received rental income but didn’t receive a Form 1099-K, you still must report this income to the IRS on your tax return if you meet the minimum tax return filing requirements.”

To access additional tax forms, visit the IRS official website.

3 Most Common Landlord Tax Documents

You can expect to encounter several tax forms for activities related to your real estate business. We’ve outlined the main ones below.

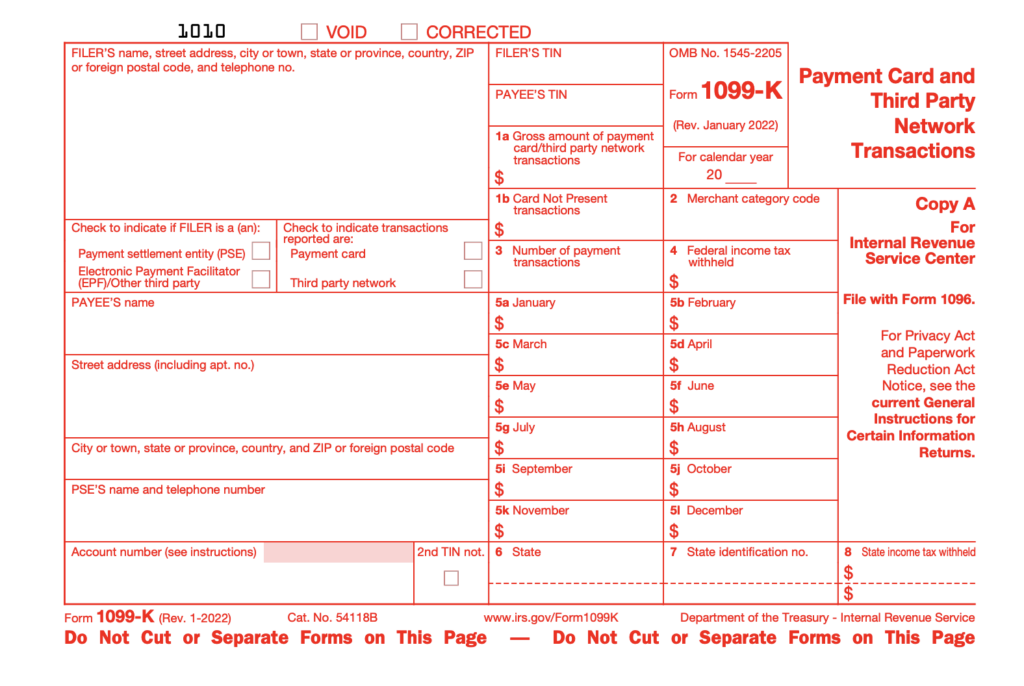

Form 1099-K

According to the IRS, Form 1099-K is “an IRS information return used to report certain payment transactions to improve voluntary tax compliance.” If you’ve received more than the minimum tax return filing requirement via payment processing platforms in the prior calendar year, you should receive a Form 1099-K by January 31, 2023.

“Unlike previous years that required a minimum number of transactions, new rules [will] require a single transaction and $600 or more in payments,” adds Adams.

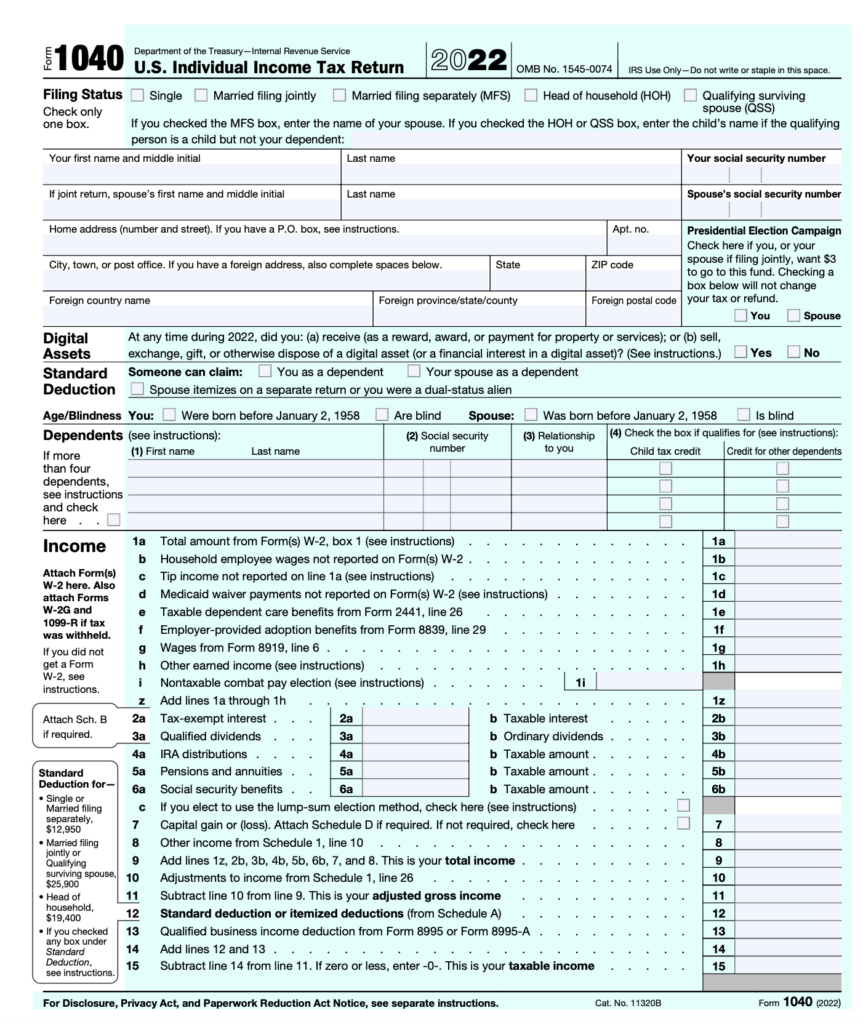

Form 1040 or 1040-SR (Schedule E)

Form 1040 is an official document taxpayers can use to file their annual income tax returns. Adams also shares that you can use this form to report your rental income, expenses, and applicable MACRS depreciation related to your rental real estate. The form is divided into sections to report your income and deductions to determine the taxes you owe or expect to receive in a tax refund.

You may also need to attach additional forms (or schedules) depending on the type of income you need to report related to your rental business.

Form 1040-SR, on the other hand, uses the same schedules and instructions as Form 1040 but is intended for taxpayers 65 years of age or older.

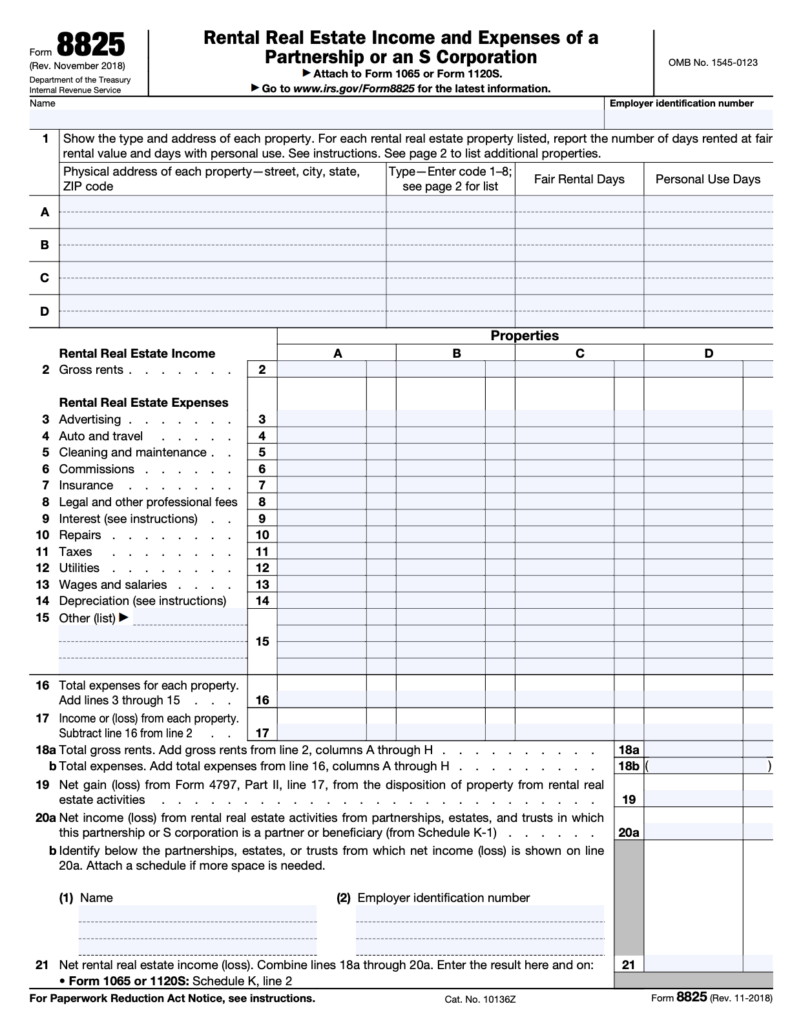

Form 8825

“If you’re incorporated as a partnership or S Corp, you’ll use Form 8825 to report income and [deductible] expenses from rental properties you own and operate,” shares Adams. “You can also report net income (loss) from rental real estate activities from partnerships, estates, or trusts.”

It’s helpful to know what tax forms you’ll most likely need to file. But as mentioned above, a CPA can help guide you through the process to complete the proper steps.

Manage Your Rentals With Avail

The best way to alleviate the stress during tax season is by knowing what tax documents to file and tracking important transactions like rental income and expenses. When collecting rent payments with Avail, you will receive a 1099-K to provide to tax professionals, making it easy to prepare the right documentation.

You can also use the Rental Property Accounting tool to track rental income and expenses for all your rental properties. Once you’re ready to file your taxes, you can export the dashboard into a spreadsheet to further customize and share with others.

Create an account or log in to manage your rentals with property management software.

*This article is intended for educational purposes only and does not constitute tax advice. Please consult a CPA for more information on filing your taxes.

The post Landlord Tax Documents: Everything to Know for Tax Season appeared first on Avail.

]]>The post How Is Rental Income Taxed? appeared first on Avail.

]]>

Owning and managing a rental property can be a great way to generate passive income through rent payments. But before pocketing that money, it’s important to remember that the Internal Revenue Service (IRS) taxes rental income and requires landlords to report it according to the new 1099 requirement.

To ensure you properly prepare for tax season, we explain how rental income is taxed and the best practices to track this.

What Is Rental Income?

According to the IRS, rental income is “any payment you receive for the use of occupation of a property.” Whether you rent your properties to travel nurses, traditional tenants, or solely rent a room, the IRS considers the money earned through this as rental income.

Other types of payments considered rental income are:

- Advance rent: This is any amount received before the lease term officially begins.

- Security deposits: You do not need to include security deposits if you plan on returning the full amount to the tenant. However, you will need to report this if you keep a part or all of the security deposit. If the security deposit was used to cover unpaid rent, the IRS considers this advance rent and will need to be reported.

- Expenses paid by tenant: If tenants are required to pay expenses you’re responsible for, such as utilities like the water and sewage bill, this is considered rental income.

- Property or services in place of rent: If you receive property or services in replacement of money for rent, you will need to include the fair market value of the property or services in your rental income. An example is when a tenant offers to paint your rental property instead of paying for two months’ rent.

How Rental Income Is Taxed

The IRS requires taxpayers that are landlords to report all of their rental income on their tax return — especially now with the recent 1099 rule requiring landlords to report rental income that exceeds more than $600 via non-employment channels. When filing your taxes, you must also report the payments the same year you receive them, even if they were credited to your tenants for a different year.

A tax professional or accountant can notify you on what tax forms you must file as a landlord, but you can generally use a Schedule E (Form 1040) form to report income and expenses from rental real estate. However, this can vary depending on your rental type, how long tenants have lived in the rental, and if it’s ever been used for personal reasons.

It’s also important to note that the amount your income is taxed will depend on which tax bracket you fall in, a detail a tax professional can share.

Is Rental Income Taxed as Ordinary Income?

Rental income is taxed as ordinary income, but there are deductibles you may qualify for as a property owner that can reduce that amount. These deductions include mortgage payment interest, insurance, utilities, Homeowner Association (HOA) fees, depreciation, repairs, renovations, and more. When filing your taxes, an accountant can help identify what deductions you qualify for.

Pro tip: Track rental property maintenance expenses throughout the year to reduce the amount you owe during tax season.

Can I Avoid Paying Taxes on Rental Income?

No, you cannot avoid paying tax on rental income, as reporting your rental income is an IRS requirement. But you can reduce the amount you owe by working with an accountant to identify what deductions and tax breaks you qualify for. Failing to report your rental income can result in accuracy-related penalties, criminal charges, and tax fraud charges.

For that reason, it’s important to have a process to track rental income, log property-related expenses for deductions, and prepare for tax season in advance. One way to do this is with the Avail Rental Property Accounting tool, which makes it easy to track all payments considered rental income and maintenance costs if logged through maintenance requests.

The dashboard automatically populates with any collected payments, which can then be exported as a spreadsheet to share with tax professionals for free. You can also add transactions collected outside of Avail to ensure everything is accounted for in one place and easy to track for tax season.

Track Rental Income and Expenses With Avail

The best way to prepare for tax season is by knowing how rental income is taxed, having a process to track rental income, and staying organized on all property accounting. While you can hire a contractor to track rental income and expenses for you, another option is leveraging an accounting software platform like Avail to streamline the bookkeeping process for all your rental properties. You can also collect rental payments, security deposits, move-in fees, and more on the same platform used to track rental income.

To get started, create an account for free to set up your rental properties and invite your tenants to Avail.

The post How Is Rental Income Taxed? appeared first on Avail.

]]>The post Rental Property Maintenance Expenses: How to Estimate Maintenance Costs appeared first on Avail.

]]>

Rental property maintenance is an integral part of being a landlord. But whether you’re managing your first rental or are planning to add another property to your portfolio, it’s essential to understand how to estimate rental property maintenance costs.

In this article, we cover common methods used to estimate rental property maintenance expenses, different types of maintenance costs, and helpful rental property accounting platforms.

How Do I Calculate Maintenance Costs on A Rental Property?

There are various ways to estimate maintenance costs, such as the 50% rule, 1% rule, and square footage rule. The approaches differ slightly, but each rule ensures that you have enough available to cover routine maintenance and unexpected repairs.

The 50% Rule

The 50% rule encourages landlords to set aside half of their monthly rental income for repairs, maintenance, and additional property management costs. If you charge your tenant $1,200 for rent, then $600 would go towards monthly expenses if you’re following the 50% rule.

The 1% Rule

This method suggests that annual maintenance costs will total approximately 1% of the total property value. If your unit’s value is $300,000, plan to budget about $3,000 to spend on rental property maintenance.

The Square Footage Rule

Under these guidelines, landlords set aside $1 per square foot of the property. A 2,000-square-foot rental will require approximately $2,000 to maintain annually.

These are only a few of the general rules of thumb for estimating costs, but remember that they are only estimates. As an additional step, you can reach out to other landlords and property managers operating in the area for feedback on their costs and budgeting strategies via phone, social media, or an online community for landlords.

In addition to helping you manage your rental property, you can connect with other landlords through the Avail Community Forum to get advice, tips, and more. You can also ask other landlords how to best estimate your rental property maintenance expenses if the methods above don’t work for you.

What Is Included in Rental Property Maintenance Costs?

Maintenance costs cover a wide range of expenses that can be separated into two categories: fixed and variable. Understanding these distinctions can help make estimating rental property maintenance costs more accurate.

Fixed Expenses Examples

Fixed expenses are costs that are paid for at regular intervals, such as monthly or annually. These expenses aren’t fixed at a specific price point but are recurring expenses to help maintain the property and operate your rental business. Here are some common examples of fixed property expenses.

- Routine maintenance: Routine maintenance refers to the necessary fixes that a rental property requires. This includes tasks like landscaping, power washing windows and siding, replacing furnace filters, and more. Landlords can combine the costs of each task over the course of a month for a reliable estimate of this expense.

- Move-out repairs: These are repairs that you complete when a tenant’s lease has expired and they move out. After completing a move-out inspection, you can identify whether certain rooms require new paint, if the carpet needs to be shampooed, and more.

- Utilities: Utilities can include electricity, water, natural gas, and more. Before estimating this cost, consider who is responsible for paying utilities at your rental — the landlord or the tenant. If you cover them yourself, combine the total monthly fees to estimate what other months could cost. If you operate a multifamily rental, consider the utilities for common areas. Even if you include utilities in your rent price, you may have to cover additional costs for these shared spaces.

- Insurance: Purchasing rental property insurance coverage can make for a smoother renting experience for landlords and tenants. You may need additional protection based on geographic location, or you may want to protect your property from specific situations. After speaking to an agent, you can incorporate your insurance premium into your expense estimates.

Variable Expenses Examples

Variable costs are expenses that arise throughout operating your rental. They may or may not occur regularly, so it’s a good idea to set aside a little bit extra in case of emergencies.

- Seasonal maintenance: If you live in an area that experiences different seasons, some of your maintenance expenses can go towards adjusting for seasonal scenarios. For example, you may need to replace filters and check the belts of the HVAC system to prepare your rental for summer, rake leaves during the fall, and have sidewalk paths shoveled during the winter months.

- Appliance repairs: Over time, your rental property appliances will require repairs. Appliances don’t break down at regular intervals, so consider the number of appliances in your rental, their age, and how frequently they’re used when you estimate this expense.

- Emergency repairs: It’s always good to have funds available for emergencies to address emergency repairs right away, especially considering local landlord-tenant laws require landlords to do so. If a pipe bursts at night, the heater dies in the middle of winter, or a tenant’s air conditioning stops working during a heat wave, you’ll have to get the problem addressed as quickly as possible. It’s impossible to know when an emergency may occur, so you may consider accounting for an emergency fund when estimating your rental property maintenance expenses.

- Capital expenditures: Capital expenditure, or CapEx, refers to the cost of making improvements to a rental property to increase the overall value. Unlike necessary repairs, these improvements are mainly intended to raise the value of the property and aren’t necessary to make the space safe for tenants. Replacing a fridge with a stainless steel version would be a capital expenditure, while simply fixing the old fridge that’s already on the property would be considered a repair.

How to Track Expenses With Avail

There are two ways to keep track of rental property maintenance expenses — with a spreadsheet or rental property accounting tool. Using a spreadsheet will require manual updating, but the Avail Rental Property Accounting tool can help streamline expenses and income tracking in minutes. If you manage maintenance issues with Avail, the dashboard will automatically populate any associated maintenance costs. Landlords can also manually add expenses logged outside of Avail to keep everything in one convenient place.

The Rental Property Accounting tool also supports building-level transactions, so if you own multifamily properties, you can assign manually-entered transactions to an entire building or an individual unit. This helps you track expenses like lawn care for an apartment building without needing to assign the transaction to a specific unit.

Can You Write Off Maintenance on a Rental Property?

According to the Internal Revenue Service (IRS), landlords can write off qualifying rental property maintenance expenses. This may include payments like mortgage interest, property tax, depreciation, and repairs.

To remain compliant with local landlord-tenant laws, be sure to consult with a tax professional. With the Avail Property Accounting tool, you can add a note to each transaction to identify what maintenance qualifies as a write-off when filing your taxes.

Track Rental Property Maintenance Expenses With Avail

Properly tracking rental property accounting can make it easier to see how much you’re spending in maintenance for a rental and what you can write off on your taxes. With Avail, you can keep your income and expenses organized in one place with the Rental Property Accounting tool. In addition to tracking rental income, you can also log and track rental property maintenance expenses for all of your rentals — for free.

Once you’re ready to share your maintenance expenses with a tax professional, easily export the dashboard into a spreadsheet to further customize or share.

Log in or create an account today to track your rental property maintenance expenses today.

The post Rental Property Maintenance Expenses: How to Estimate Maintenance Costs appeared first on Avail.

]]>The post New 1099 Requirements for Landlords and Rental Property Taxes appeared first on Avail.

]]>

There are several ways landlords and property managers can collect rent. You can use a rent collection app, an online payment platform, or request paper checks from your tenants. Up until recently, it was possible to receive payments without having to report the earned amount during tax season.

However, the Internal Revenue Service (IRS) implemented a new change regarding rental income reporting in 2022 to address unreported rent. Landlords and property managers must now report rental income over $600 during tax season, as opposed to $20,000 previously.

Note: The IRS has delayed the 1099 requirement to the 2024 tax filing season.

To help you better understand the changes made by the IRS, we outline what you need to know about filing a 1099 form according to a certified public accountant (CPA).

New 1099 Requirements for Rent Payments

The IRS will require landlords to report rental income exceeding $600 via non-employment channels versus $20,000. This change comes from the American Rescue Plan Act that was signed into law by Congress in 2021, which was intended to address the amount of unreported income earned through non-employment-related channels.

“If you receive rental payments via an electronic payments processor and they exceed $600 during the year, you should expect to receive a 1099-K form in the mail, digitally or possibly both,” shares Riley Adam, CPA, a certified public accountant and founder of Young and the Invested. “A copy should be sent to you for your return and also to the IRS, [but] you must still report this income to the IRS on your tax return if you meet the requirements, even if you didn’t receive a Form 1099-K.”

Before working on your tax return, he suggests reviewing the forms provided by a payment processing platform to check for potential errors. “If there is an error made on the form provided to you, you can rectify the issue by clarifying the correct figures on your Form 1040 (tax return),” he shares. “It can be unlikely that the payment processor will rectify the error [and] instead leave that to the 1099-K recipient.” So make sure to check your 1099 forms to ensure there’s no errors.

You can then provide this to your tax professional for them to prepare the required forms once you have all of the necessary information. “If doing your own taxes, you can use this information to answer questions provided in tax software solutions or by hand by downloading the forms directly from the IRS’ website.”

It’s especially important to abide by the new 1099 requirement to avoid unfavorable penalties. “Failure to file the proper forms could result in a follow up from the IRS to inquire about your tax position and also result in corresponding penalties, fines and interest for failing to pay sufficient taxes.”

It’s worth noting that the change applies to payments received through all third-party processing vendors such as PayPal, Venmo, Zelle, and landlord software. While certain services like PayPal and Venmo will provide a 1099-K to users that cross the new threshold amount, others will not. If you use a service that doesn’t, you’ll be responsible for filing the appropriate form yourself.

What Is a 1099 Form?

The 1099 form is a tax form that documents income from a source that isn’t an employer. Examples include rental income, earnings made as an independent contractor, and a tax refund from the state or local level. There are 20 different variations of the 1099 form, but a few are important for landlords to be familiar with:

- 1099-K: “If you accepted credit card or debit card transactions that amount to more than $600 during the tax year, you’re likely going to receive a Form 1099-K reporting these payments,” shares Adams. Most rent collection apps and payment services will provide 1099s prior to tax season.

- 1099-NEC: Businesses use the 1099-NEC form to record payments to non-employees for services throughout the year. If a landlord works with an independent contractor for repairs and maintenance, they will need to provide them with a 1099-NEC if they cross the $600 total threshold.

- 1099-MISC: As the name suggests, the 1099-MISC form is for miscellaneous sources of income. This is relevant to property owners who collect rent in the form of cash or paper checks.

Rental Income Taxes Explained

According to the IRS, a taxpayer must report all rental income when preparing rental property taxes with few exceptions. If you rent out your property for $1,000/month and earn $12,000 by the end of the year, the remaining amount after deductions is taxable income.

In addition to on-time rent payments, you’ll need to track other sources of rental income. If you keep a portion of a tenant’s security deposit at the end of their lease to cover repairs or damages, that amount is your rental income, and taxable. Other sources of taxable income include advance rent, tenant-paid owner expenses, and lease cancellation payments.

Reporting Rental Income

Due to recent 1099 laws for rent paid to landlords, it’s even more important to accurately track and report rental income. Instead of reverting to a paper-and-pencil method, landlords can use a platform like Avail to easily keep track of rental income.

The Avail Rental Property Accounting tool can help streamline the tracking process by providing a comprehensive view of collected rent payments and logged maintenance expenses for each rental property. Create an account to get started today.

*This article is intended for educational purposes only and does not constitute tax advice. Please consult a CPA for more information on filing your taxes.

The post New 1099 Requirements for Landlords and Rental Property Taxes appeared first on Avail.

]]>The post 7 Best Accounting Software Platforms for Landlords appeared first on Avail.

]]>

As a landlord, you’re tasked with staying on top of accounting for your rentals to see how they’re performing financially. While you can always track everything with a spreadsheet, accounting software specifically designed with landlords and property managers in mind can simplify the process. Unlike regular accounting tools, these platforms make it easier to see how much cash flow is coming in for each rental property and how much your operating expenses are totaling each month.

However, you may be wondering which platform is the best for you and your goals, which is why we outlined the best accounting software for landlords. Keep reading to see how each platform differs in offerings, pricing, and more.

What Is Accounting Software for Rental Properties?

Accounting software for rental properties is intended to help landlords keep track of important income and expenses that impact their profits and performance. They are also designed to make filling out your tax forms easier, especially if you have more than one rental property.

What Is the Best Accounting Software for Real Estate Investors?

Various types of rental property accounting software platforms exist, but here are the best options to look out for.

1. Avail

Avail (part of Realtor.com®) is landlord software designed for independent landlords with one to 50 properties. Advertise your rental, screen tenants, collect rent online, track income and expenses, and more, all in one platform.

Payments collected through Avail and logged maintenance costs automatically upload to your rental property accounting dashboard to make it easier to see how much money is coming in and out. You can also sort your income and expense tracker by property, payer, type, category, date, or amount if you’re looking for specific information on your finances.

Avail even makes it easy to keep your income and expenses organized. When manually adding transactions to the Rental Property Accounting tool, landlords have the option to assign a specific building or unit. This function can be especially helpful for landlords who own multifamily properties and want to track expenses related to the entire property as well as a specific unit.

And, if you want to quickly sort through your payments and costs, landlords can filter transactions by building or unit. This can help you find the information you need much more efficiently.

Once tax season approaches, you can export your tracker into a customizable spreadsheet to share with tax professionals or add additional information to the document. The Avail Rental Property Accounting tool is free for all landlords, regardless of how big your portfolio is.

2. Appfolio

Appfolio is a property management software platform intended for landlords with 50 units or more. The accounting tool uses AI technology to read PDF files and identify important information on income and expenses, removing the manual process. Appfolio also allows landlords to automate accounts payables workflows by setting up automated payments to pay invoices on time each month.

If you’re looking to analyze the performance of your investment portfolio, you can do so with its customizable dashboard showing important financial data, such as total expenses and revenue. Although there are no required setup fees, monthly fees can range from $280 for small landlords to $1,500 for landlords with more than 1,000 units.

3. Rentec Direct

Rentec Direct offers accounting tools that work to make rental tracking less time-consuming. Unlike traditional accounting systems, Rentec makes it easy to review, edit, and print ledgers for every property, tenant, and bank account. Sort through all of your financial reports by name, reporting period, account, and rental property. Any income and expenses logged in the platform can also be exported into a spreadsheet to share with tax professionals to prepare for your tax forms.

There are two available account options — Rentec Pro and Rentec PM — with Rentec PM offering more benefits. Rentec Pro is $35/month, while Rentec PM is $40/month, totaling up to $420 to $480 annually.

4. Buildium

Buildium is another option designed for landlords with 50 units or more and can cost anywhere from $50 to $460 per month to have an account. Its property accounting tool allows you to track budgets, vendor payments, monitor company financials, and collect rent payments.

Their system also reconciles your bank statements automatically to ensure all of your documents include accurate information. While there are tons of benefits that Buildium offers, it can quickly become expensive to use for landlords with smaller portfolios.

5. Stessa

Stessa is designed to make rental property money management simple with automated income and expense tracking, personalized reporting, and more. You can easily see the current value of your portfolio based on your financials, occupancy rate, available properties, and cash flow. Their transaction dashboard can also be filtered by rental property, category, date, and payer to easily sort through your income and expenses.

However, Stessa is mainly intended to help with financials and cannot be used to help with other areas of renting (like rent collection, maintenance tracking, or tenant screening).

6. Property Matrix

Property Matrix offers a complete set of accounting tools that can make the bookkeeping process easier for landlords with large portfolios. You can manage income and expenses with their tracking tool, analyze the performance of your rentals, and more.

Property Matrix has the highest monthly cost, with their Standard subscription costing $400 per month, their Property Matrix Pro costing $475 per month, and the Enterprise subscription costing up to $1,200 per month.

7. DoorLoop

Doorloop makes it easier to streamline and optimize various parts of the rental process with their property management software tools. You can create custom income and expense reports, collect rent, and upload important documents.

Doorloop offers three plans — the Starter plan for $49/month, the Pro for $79/month, and Premium for $109/month. It’s important to note that the cost does go up the more units you manage.

How Does Accounting Software Differ From Bookkeeping Software?

Bookkeeping software helps keep track of income and expenses through a daily ledger, while accounting software offers more capabilities to users. Accounting software can help you get a better idea of how well your rentals are performing financially and integrate other areas of managing your rentals, such as rent collection and maintenance costs.

Who Should Get Accounting Software?

You may be able to get away with manually tracking your rental property income through a spreadsheet, so long as you only have one or two rentals. However, the process can quickly become time-consuming and leave more room for discrepancies if you do not regularly upkeep the spreadsheet. With accounting software, you can automate the bookkeeping process without having to hire a property manager or additional help.

Make Rental Property Accounting Easy With Avail

Whether you’re looking for an easy way to track rental property income and expenses or a complete suite of tools to manage a large portfolio of properties, there are various options to explore. With Avail, you can use the same platform to manage your rentals and rental property accounting to keep everything in one place.

Create an account or log in to start managing rental property accounting with Avail for free.

The post 7 Best Accounting Software Platforms for Landlords appeared first on Avail.

]]>The post Rental Tracking: How to Track Rental Property Expenses appeared first on Avail.

]]>

Tracking your rental property income and expenses requires time and resources to keep everything organized. Thanks to property management software platforms, the process can now be done without the help of a property manager and in less time. We share best practices on how to track rental property expenses and tips on how to properly manage rental tracking.

What Does Rental Tracking Consist of?

Rental tracking involves identifying which operating expenses need to be accounted for and creating a process to periodically track them. This can be done with a rental property expense tracker to streamline the process for you or via a spreadsheet if you prefer to do it yourself. Regardless of your bookkeeping method, all of your records should include accurate and up-to-date information on your rental property accounting.

Having inaccuracies on financial documents can make it difficult to analyze how profitable your rental is and correctly fill out your tax forms.

Important Records Landlords Should Save

Storing important records makes it easier to log accurate expense totals and have supporting documents to share with the Internal Revenue Service (IRS). There are six types of records you’ll want to save, including the following:

- Receipts and invoices: Receipts and invoices from contractors (such as maintenance or property managers), software platforms, utility companies, and supply stores should all be saved to prove the expense amount.

- Bank statements: Bank statements can be a great way to illustrate a months’ view of income and expenses, but the bank account should be used for only property-related transactions.

- Proof of rent payment: Rent payment documents show how much the tenant paid in rent, the date, and for which rental property.

- Mortgage loan documents: Your mortgage documents show how much you pay each month with a breakdown of the principal, interest, taxes, and insurance.

- Federal and state tax returns: Store your previous federal and state tax returns in a safe place for easy reference.

How to Keep Track of Rental Property Expenses

The key to tracking rental property expenses is establishing a process that works for you, helps you stay organized, and gets you prepared for tax season. Here are three steps to help you track your expenses for your rental property.

1. Identify What Needs to Be Tracked

Identifying what needs to be tracked can make it easier to organize your transactions and update your financial records. Some examples of income and expenses to track are:

- Recurring rental payments (rent, parking fees, pet fees)

- One-time tenant fees (move-in fees)

- Fees to break a lease

- Security deposits used to cover unpaid rent or property damage

- Recurring monthly expenses (mortgage, HOA fees, property taxes)

- One-time fees (maintenance, legal fees)

- Property depreciation

2. Establish a Bookkeeping Process

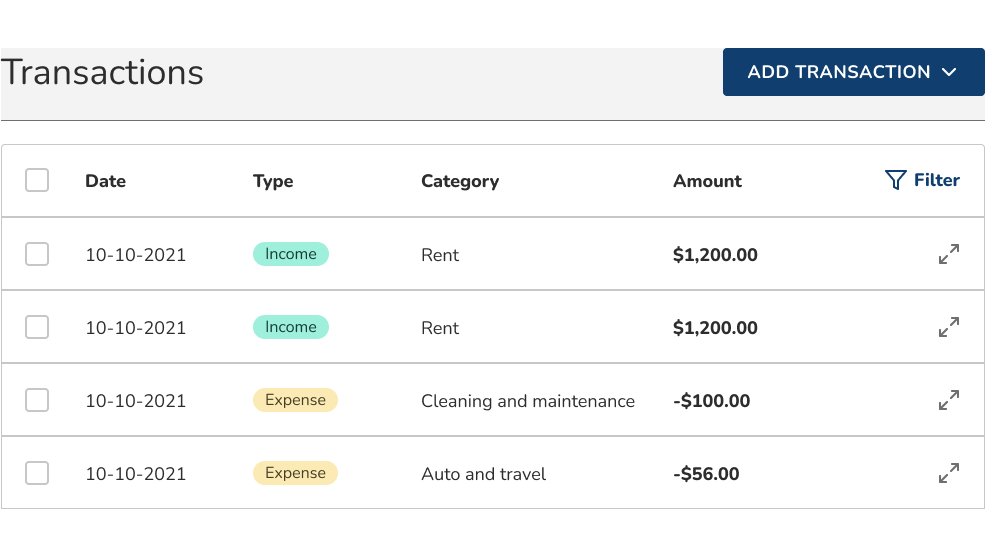

With the Avail Rental Property Accounting tool, you can track income and expenses in the same platform used to manage your properties. Your dashboard automatically updates with payments from tenants and logged maintenance costs for each rental property. You also have the option to add new transactions collected outside of Avail to keep all of your income and expenses in one place.

Each transaction shows who paid, the total amount, the date, the type of transaction, and which rental property it’s for. If you’d like to upload supporting documents (such as an invoice or receipt), this can be easily done for future reference. Once tax season approaches, you can export your rental property income and expense tracker to share with tax professionals or further customize it to your liking.

3. Check Income and Expenses With Bank Statements

There can be discrepancies between your financial documents and bank statements. Periodically check your financial documents to ensure all the information is correct, especially once you know how much certain expenses totaled out to.

Doing this throughout the year can help you catch anything worth adjusting and make it easier to complete your tax forms.

Track Rental Property Expenses With Avail

Rental tracking doesn’t have to be time-consuming. The Avail Rental Property Accounting tool can help you save time and money by logging important transactions for each rental property — all in one place, for free.

Create an account or log in to streamline the bookkeeping process for your rentals today.

The post Rental Tracking: How to Track Rental Property Expenses appeared first on Avail.

]]>The post Landlord’s Guide to Rental Property Accounting appeared first on Avail.

]]>

Many can agree that rental property accounting makes managing a rental stressful, especially if it’s your first time. But there are ways to make the process easier without having to hire outside help.

We share all the different areas of rental property accounting to know about and tips to implement to your routine that can make your finances easier.

The Importance of Rental Property Accounting

Rental property accounting is crucial for landlords looking to analyze their investments, prepare for tax season, and keep track of money going in and out. Not having a bookkeeping process in place for each rental can make it harder to catch when a property is too expensive to maintain or gauge its profitability in a changing housing market.

Whether you prefer to hire an accountant or do it yourself, the key to rental property accounting is developing habits to stay on track with your finances.

What Are the Basic Principles of Rental Property Accounting?

There are different components to rental property accounting, such as banking information, how you plan to track income and expenses, and understanding rental income tax forms. Here are the three basic principles of rental property accounting to be aware of:

1. Banking

While it may be tempting to have all your rental income deposited into your personal banking account, it’s important to create a separate bank account for your rental properties. This keeps your rental income separate from your personal funds and may even be required by local landlord-tenant laws. You can create a new checking account (or business account if you have an LLC) to have all your rental income deposited and to use to cover operating expenses.

2. Income and Expense Tracking

Having a bookkeeping process in place removes having to total up all your expenses at the end of the year or when it’s time to complete your tax forms. Instead of sorting through multiple bank statements or rent roll reports, you can have your income and expenses already outlined to share with tax professionals or to analyze how your rentals are performing financially.

With the Avail Rental Property Accounting tool, rental property bookkeeping is automated. Rental payments collected through Avail and logged maintenance costs will automatically populate to your dashboard, and our system will update new income for each rental property with information on the payer, the date, the total amount, the building or unit the payment is for, and the type of transaction. This information can then be exported into a spreadsheet to further customize or share with tax professionals.

3. Tax Forms

It’s important to familiarize yourself with rental property-related tax forms to understand what information is requested. In most cases, the Internal Revenue Service (IRS) requires landlords to complete a Schedule E (Form 1040) to report rental income and expenses for each property. It’s also important to note that the IRS now requires landlords to report rental income that exceeds $600 with the new 1099 requirement.

The Main Types of Rental Property Income and Expenses to Track

As a landlord, there are different types of rental property income and expenses you’ll need to track. To ensure you’re accurately bookkeeping the right transactions, it’s advised to track the following:

- Rental income: Income consists of rent payments, move-in fees, pet fees and rent, fees to break a lease, and security deposits that have been kept to cover property damage or unpaid rent.

- Operating expenses: Not everything regarding your rental is considered an operating expense. According to the IRS, these are the main items that you’re expected to report: advertising fees, auto and travel (for commuting), cleaning fees, landlord insurance premiums, maintenance, legal fees, mortgage interest, property taxes, landlord software fees, Homeowner Association (HOA) fees, utilities, and rental property depreciation.

If there are additional transactions you’d like logged through Avail, you can add them to your income and expense tracker with attached receipts or invoices for future reference.

How to Manage Rental Property Income

Managing your rental property income doesn’t have to be time-consuming. Here are three steps to help you manage your finances and stay on top of important transactions.

- Create a separate banking account: This account will be where any rental property-related income will be deposited and used to cover expenses.

- Track income and expenses for each rental: Create an account with Avail to track your income and expenses for each rental for free. You can also input previous transactions collected outside of Avail to keep everything in one place.

- Reconcile monthly and report at year-end: At the end of each year, it’s important to reconcile your financial statements with the numbers in your budget. Reconciling involves comparing the numbers on your financial statements with the ones on bank statements attached to each bank account. Doing this exercise can help you catch and adjust discrepancies to show accurate information on your documents.

Do You Need an Accountant to Help With Rental Property Accounting?

It may be worth hiring an accountant to help with rental property accounting if this is your first time managing a rental or you don’t have time to track your finances. However, platforms like Avail now make it easier to stay on top of your finances and have a comprehensive view of your income and expenses for each rental property.

Make Renting Property Accounting Easier With Avail

Rental property accounting doesn’t have to be stressful, especially with the right tools. Avail can help you track your income and expenses for multiple properties in one place — for free. Easily add your rental properties, set up your tenants, and collect rent payments to have each transaction automatically populate to your dashboard.

Create an account or log in to make rental property easier with Avail.

The post Landlord’s Guide to Rental Property Accounting appeared first on Avail.

]]>The post What Is Rental Property Depreciation? appeared first on Avail.

]]>

Rental property depreciation can help you deduct property-related costs to lower your taxable income for the year. Tax professionals typically help in calculating depreciation for your properties, but there are benefits to knowing what rental property depreciation is and what to keep track of as a landlord.

Here’s everything you need to know about rental property depreciation and how to calculate depreciation for your properties.

What Is Rental Property Depreciation?

Rental property depreciation describes a property’s reduction in value due to wear and tear or property damage. Depreciation can help landlords recover the costs associated with income-producing properties (such as buying, improving, and managing costs) and must be taken over the expected life of the property.

How Does Rental Property Depreciation Work?

According to the Internal Revenue Service (IRS), you can begin to depreciate your property once it’s ready to rent and available to tenants. Depreciation ends once you’ve fully recovered your costs or when the property is no longer a rental, whichever comes first.

An example of rental property depreciation is as follows: You purchased a rental property on June 20 and published a rental listing for the rental property on August 15. You’ve completed the tenant screening process and found your next tenant set to move in by September 1. Depreciation on the property would begin in August, since your property was ready to be leased in that month.

Rental property depreciation can continue even if the property is not in use, whether it be to make extensive repairs or during the process of finding a new tenant. There are different depreciation methods to follow, but this is often determined by a certified tax professional when completing your taxes.

Can Your Rental Property Be Depreciated?

Your rental property must meet the following requirements set by the IRS to qualify for rental property depreciation:

- You must be the owner of the property

- The property must be used to generate income

- You must be able to determine useful life for the property that’s more than one year

If you’re unsure if your property qualifies, you can refer to a certified tax professional to help answer your questions.

How to Calculate Depreciation on a Rental Property

To calculate depreciation on a rental property, you’ll need the cost basis of the property, the recovery period, and recommended depreciation method. Rental properties placed in service (or in use) after 1986 can follow the Modified Accelerated Cost Recovery System (MACRS) method that spreads costs over the span of 27.5 years — the useful life of a rental property, according to the IRS.

Ideally, a certified tax professional would help you calculate depreciation on a rental property to ensure your tax forms are filled out correctly. However, here are three steps to take to help you perform the calculation yourself.

- Determine the cost basis of your property: The basis of the property is the total acquisition cost, including the mortgage, legal fees, transfer taxes, and title insurance. This number is then subtracted from the value of the land the property is built on.

- Separate the cost of land and buildings: You can only depreciate the cost of the building, not including the land. To separate the cost between the two, you can refer to the property’s fair market value for individual costs.

- Use a property depreciation calculator: Use a property depreciation calculator to determine the cost basis, recovery period, and place in the service period for your property.

The depreciation you calculated can then be shared with a tax professional to confirm the amount is correct.

How Much Does Depreciation Reduce Tax Liability?

You can report your rental income and expenses for your rentals on a 1040 tax form. The depreciation amount will need to be outlined on the appropriate line of Schedule E to reduce your tax liability for the year. Tax liability reduction will depend on the tax bracket you’re in and how much depreciation you report.

Track Rental Property Income and Expenses With Avail

Taking advantage of rental property depreciation on your tax forms is essential for landlords. Rental property depreciation allows you to spread out the cost of buying a property over decades to lower your taxable income.

For that reason, it’s important to keep track of your property-related expenses with a platform like Avail to make tax season easier. The Rental Property Accounting tool can help you track your rental income and expenses in the same platform used to manage your rentals — for free.

Create an account or log in to streamline the bookkeeping process.

The post What Is Rental Property Depreciation? appeared first on Avail.

]]>The post 4 Tips for Preparing Your Rental Property Taxes appeared first on Avail.

]]>

Filing taxes for a rental property can be stressful, but preparing the necessary paperwork can be a helpful way to simplify the process. In this article, we spoke with Riley Adams, a certified public accountant (CPA) and the owner of Young and the Invested, to share helpful tips on preparing your rental property taxes as a landlord.

What Information and Documents to Prepare for Tax Professionals

According to Adams, the best way to make tax time easier is by tracking rental income, incurred expenses during the year, and the depreciable basis in your properties.

In addition to that, he suggests preparing the following for tax professionals:

- Rent rolls with a record of rent payments. If you collect rent payments and other fees with Avail, our system automatically generates rent roll reports to download.

- Relevant receipts and work orders that list costs related to maintaining your property. “Receipts are also recommended for any inquiries from the IRS, including but not limited to follow-up questions or even audits,” he shares.

- Compile previous tax returns to track the property’s taxable basis and relevant 1099 forms.

- Bank statements if you don’t have rent rolls or similar documentation.

- Mortgage documents and payments for all your rental properties.

- Documentation supporting investments or renovations made in the property that are eligible for depreciation.

He recommends keeping track of all these forms and documentation to substantiate any reported figures or positions taken on your tax return.

4 Tips to Consider When Preparing Your Rental Property Taxes

There are steps you can take to help with filing taxes on your rental property. Here are four tips that can help you prepare your rental property taxes to share with tax professionals.

1. Identify What Needs to be Tracked

Renting out a property should be approached as a business, since rental income and operating expenses will need to be tracked. For that reason, it’s important to identify what expenses and transactions you need to be aware of when tax season approaches.

Some operating expenses examples are advertising, cleaning and maintenance, mortgage payments, landlord software fees, and property taxes. Your expenses will vary depending on where your rentals are located and what you prefer to do yourself.

Adams also suggests documenting any costs split between personal and business use. “Make sure you document what this split is and use it consistently across your tax return,” he shares. “You can sometimes split personal costs with business costs [when investing in real estate], which allows you to deduct a portion of your expenses used for both needs.” Examples can include your internet bill, an at-home office, and property maintenance fees.

2. Log Income and Expenses to Share With Tax Professionals

Now that you know what rental income and operating expenses to track, establish a process to log them. With Avail, you can collect rental income (rent payments, security deposits, move-in fees, pet fees) and log income and expenses with the Avail Rental Property Accounting tool.

Existing payments, maintenance costs, and other transactions collected through Avail will automatically populate to your dashboard. Furthermore, you can assign manually-entered transactions to an individual unit or building.

You can also filter income and expenses to display by unit or property to help organize the information you plan to share.

You must prove any transaction reported on your tax return with supporting documentation, so you’ll want to save invoices, receipts, and other necessary documents. The tool allows you to add one-time transactions and upload any associated paperwork in case you need to provide more information to the IRS.

Once you’re ready to share your rental income and expenses, all your transactions can be exported into a spreadsheet to further customize and share with tax professionals. A process often considered time-consuming can now be streamlined in minutes without the help of a property manager.

3. Research Rental Tax Deductions You May Qualify For

Being a landlord can help you qualify for certain rental property tax deductions relating to your mortgage, insurance, property renovations, and homeowner association fees. It’s smart to research the different types of tax deductions that exist for landlords or ask an accountant for further information.

Adams also shares that if you held property for more than a year that was used to earn rental income, you may qualify for treatment of the property as Section 1231 property. “This special designation allows you to treat the gains on the property as capital gains and the losses as ordinary income, in effect giving you the most advantageous tax treatment in either situation,” he explains. “You may also qualify for using the Section 1031 tax exchange rules to transfer your taxable basis between rental properties, avoiding a tax hit in the year of sale.” However, your tax professional will ultimately determine if you qualify for this tax treatment.

4. Research Gain on Sale of Your Primary Residence Exclusions

If you’re selling your primary residence that you’ve lived in for two out of the last five years, you may be eligible to exclude all or a portion of the gain on sale, according to Adams. “If you are a single filer and meet the residency requirements, you can generally exclude up to $250,000 in gains recognized from the sale or up to $500,000 for joint filers,” he adds. “You may be exempt from reporting these gains on your tax return, but this can vary based on eligibility.”

Track Rental Property Expenses With Avail

Tax season can quickly become overwhelming for any landlord, but there are ways to simplify preparing your rental property taxes. Platforms like Avail make it easier to streamline the bookkeeping process to help you track your rental property income and expenses in accordance with the IRS for free.

With the Avail Rental Property Accounting tool, you can track all the necessary information for your tax forms in minutes. Create an account or log in to simplify tax accounting for your rental property.

*This article is intended for educational purposes only and does not constitute tax advice. Please consult a CPA for more information on filing your taxes.

The post 4 Tips for Preparing Your Rental Property Taxes appeared first on Avail.

]]>The post Avail Introduces a New Rental Property Accounting Feature appeared first on Avail.

]]>

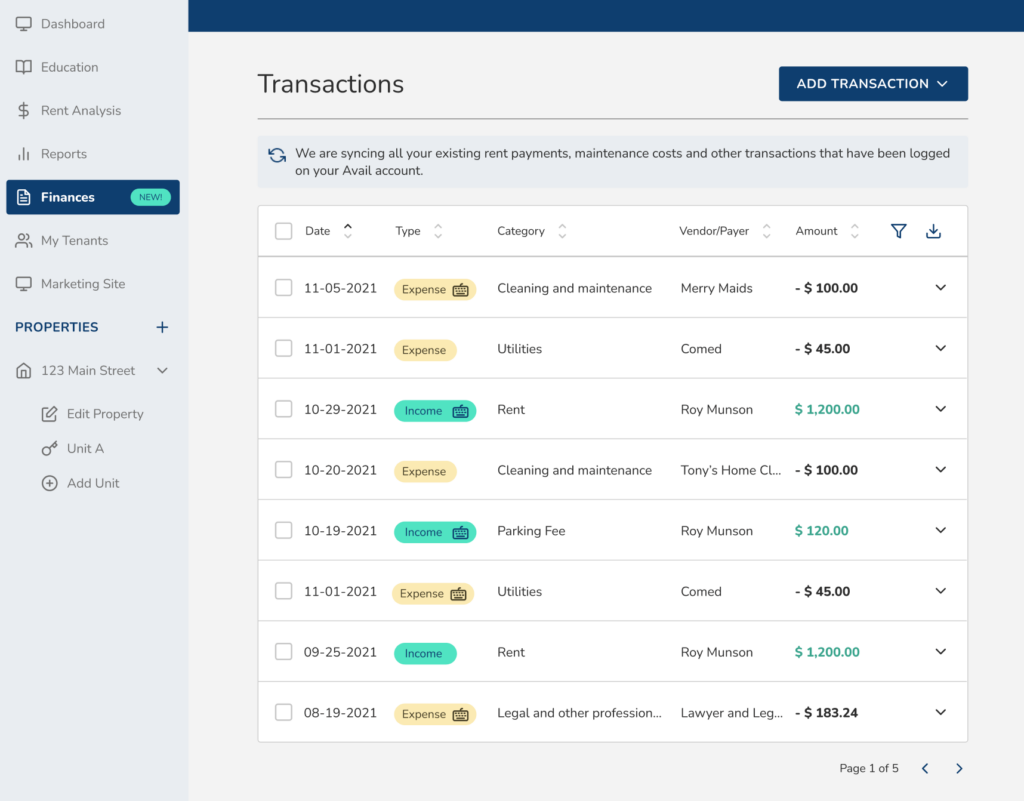

Keeping track of your rental property income and expenses is now easier than ever with the new Avail Rental Property Accounting tool. Landlords can comprehensively track and manage their financial transactions related to each rental in the same platform they collect rent payments, manage maintenance requests, and more.

Here’s everything you need to know about the Avail Rental Property Accounting tool.

How the Avail Rental Property Accounting Feature Works

Instead of using spreadsheets, the Avail Rental Property Accounting tool can help you easily track your rental income and expenses in one platform — for free.

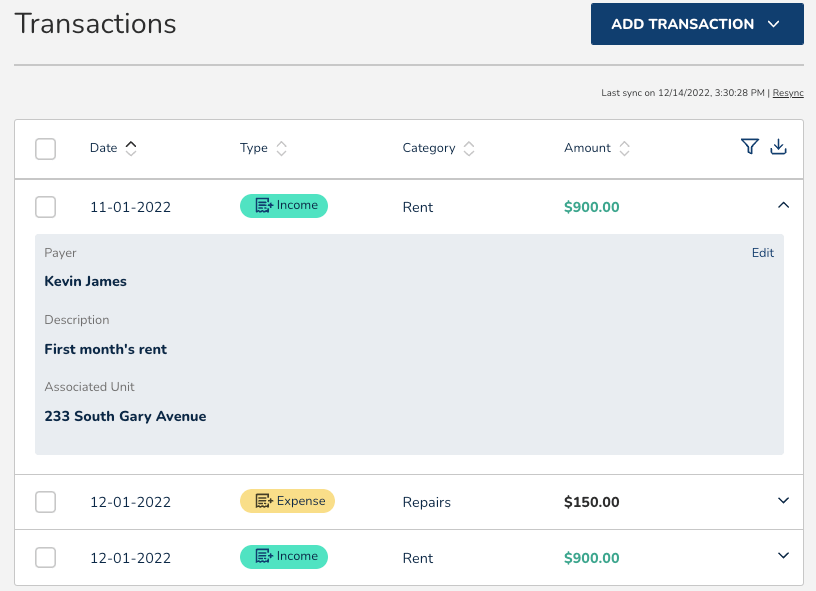

When you click on the “Accounting” tab, you can view all the rental income that each of your rental properties has generated and log operating expenses that accumulate over time. If you’re already using Avail to collect payments from tenants, your transactions will automatically populate in your transaction dashboard with information on the tenant, total payment amount, the relevant building or unit, and type of transaction.

Monthly fees — rent payments, parking fees, pet fees, and move-in fees — collected through Avail will automatically populate as one rent payment in your dashboard. One-time payments, such as a maintenance repair or a late fee, will be displayed separately with the type as “other”. If you want to keep them separate, you cab manually input them to have a clear view of all transactions.

You will also be able to view maintenance costs that have been logged in previous tickets to get a complete overview of your expense transactions.

Avail Rental Property Accounting Feature Benefits

There are other rental property accounting software platforms available, but Avail can help you in the following ways:

- Increases visibility: Instead of sorting through bank statements, you have more visibility into all of your property-related transactions in the same platform used to manage your rentals.

- Makes tax season easier: The new accounting feature allows you to categorize each transaction as an income or expense to help you prepare for tax time.

- Track the performance of your rentals: You have the option to filter your transactions by building or unit to see how each rental is performing. Since everything is outlined by transaction category, you’ll be able to see if you’re paying more in expenses than what you’re generating in rent payments.

How to Track Your Income and Expenses With Avail

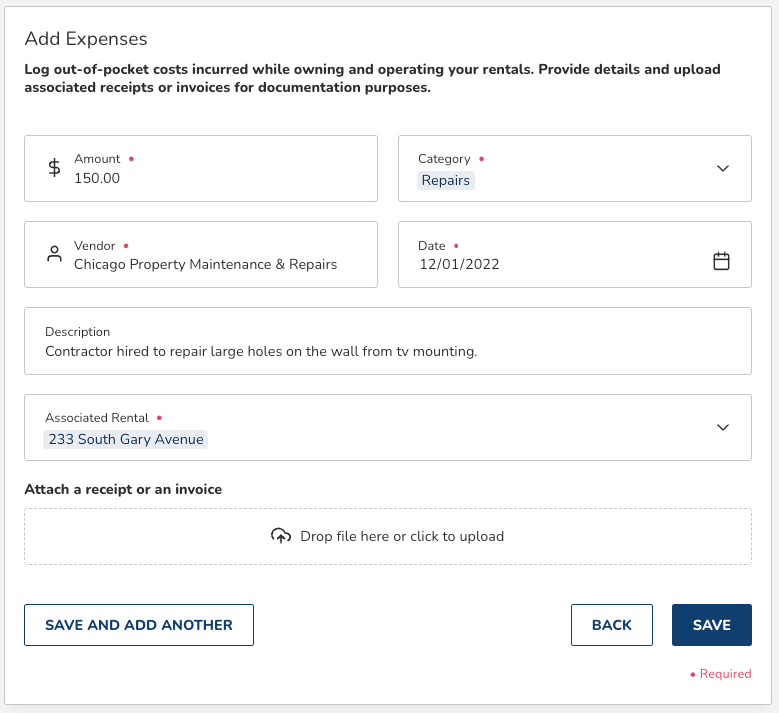

The Avail Rental Property Accounting tool is a great way to streamline the tracking process for income and expenses. If you need to add a new expense transaction, you can include what it’s for, the total amount, and upload pictures of invoices or receipts for safekeeping. Both new and synced transactions can then be deleted or edited if the total cost changes.

Each transaction can be categorized by the type of transaction (expense or income), whether it’s an admin expense, maintenance expense, or a rental payment from a tenant.

Can I Export the Transactions in the Rental Property Income and Expense Tracker?

You can view all of your transactions through your dashboard or export them into a spreadsheet. Both options can be filtered and sorted to your liking to help you view the property information, the date, income or expense category, the total amount, and more.

Transactions that were manually added or automatically populated can be exported into an excel spreadsheet that can be further edited or shared with a tax professional.

Will Charges for Existing Users Automatically Populate?

Payments collected through Avail and maintenance tickets with reported costs will automatically populate in your dashboard, whether it be rent payments or small repairs. However, new users will need to manually input previous expenses and income collected outside of Avail if they want all of their transactions in one place.

Simplify Rental Property Accounting With Avail

Rental property accounting can be stressful to handle as an independent landlord, but Avail helps simplify the process for free. Landlords can collect rent payments, keep a track record of rental income, and log expenses in minutes. The log can then be exported to share with accountants or tax professionals to help you file your taxes.

Create an account or log in today to start taking advantage of the Avail Rental Property Accounting tool.

The post Avail Introduces a New Rental Property Accounting Feature appeared first on Avail.

]]>