The post Is Renters Insurance Worth It? What Does It Cover? appeared first on Avail.

]]>

Since only 37% of renters have renters insurance, it might not feel like something every renter needs — but it is. For an affordable monthly payment of anywhere from $12 to $15 a month, you can protect everything you own from theft and damage, and it covers a lot more than you’d think.

Here’s what you need to know about renters insurance before you purchase it.

What Does Renters Insurance Cover?

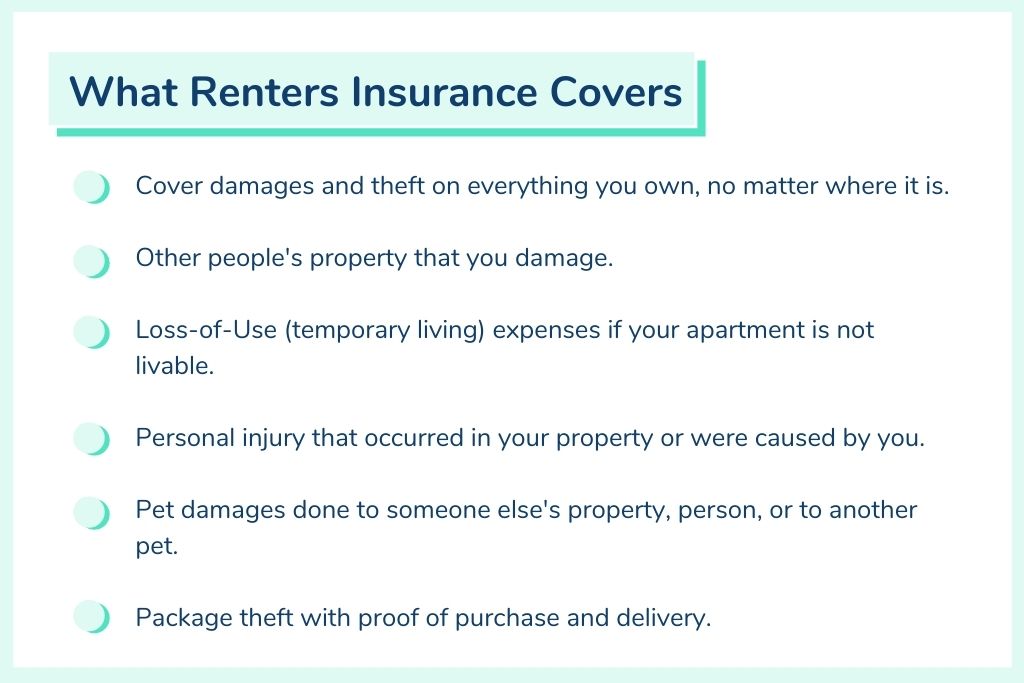

The overall purpose of renters insurance is to cover a renter’s personal property if it’s damaged or stolen, so if it’s anything within those parameters, it’s usually covered.

Most insurance companies will cover everything that you own and account for in your policy, even if they aren’t in your apartment. That includes all items that you take with you on vacation, that may be in your car, or anywhere else. As long as you own it, it will be covered by your renters insurance if damaged or stolen.

Some renters insurance policies cover damages to other people’s property that you’re responsible for, whether it be to property in a friend’s apartment or to the property in other units in your building. If it’s the latter, your insurance will cover the damages to other units as long as they’re not covered by your security deposit. However, renters insurance won’t cover damages to the rental itself. Either the person responsible for the damages, your landlord, or your security deposit will pay for the repair.

Renters insurance also covers the cost of temporary living at a hotel or elsewhere if your apartment and the property in it are damaged by a natural disaster. This money would cover the cost of temporary housing, food, cost of laundry, etc.

Finally, if your renters insurance has a liability clause, it can cover personal injuries or damages that occurred in your apartment or were caused by you. That is to say that if you decide to put money aside in your policy for a personal liability clause, your renters insurance will cover the medical or legal fees of anyone who was hurt in your apartment.

What Does Renters Insurance Not Cover?

When shopping for a renters insurance policy, it’s important to know what each plan doesn’t cover so you can decide which is the right one for your needs.

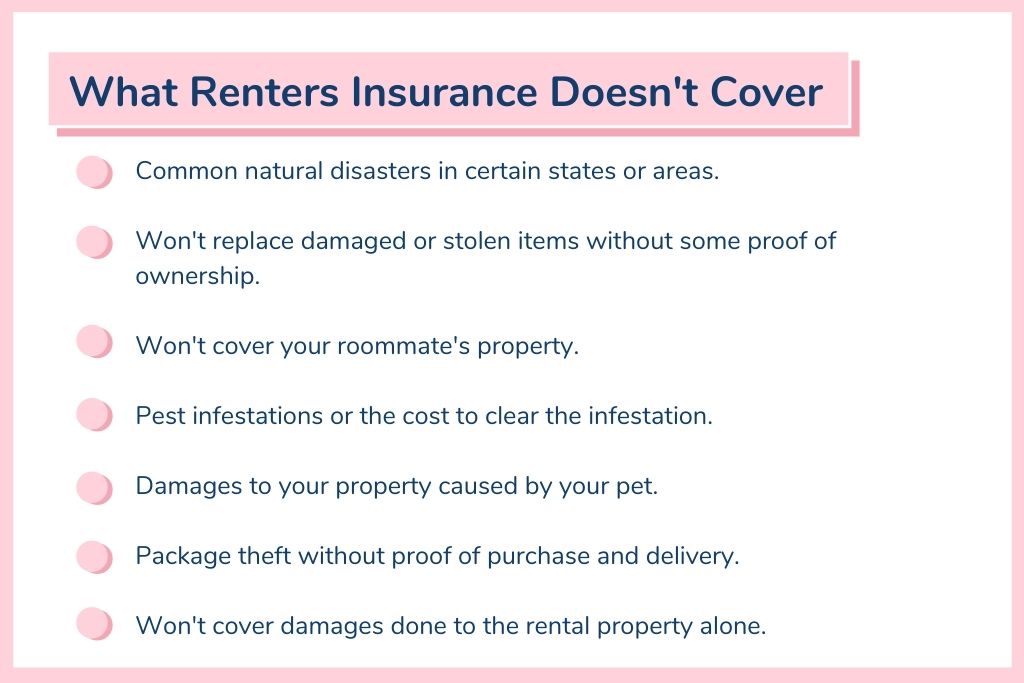

In some states, certain common natural disasters might not be covered by renters insurance and will require you to purchase a separate policy. For example, renters insurance in California doesn’t cover earthquakes, while Florida doesn’t cover flooding.

Generally, renters insurance won’t replace damaged or stolen items that don’t have a proof of ownership, as the insurer will never know if that item is really yours. This can be difficult, especially if you don’t keep physical or digital receipts of each item you purchased. It’s not required that you have a receipt for a stolen or damaged item, but you will need to prove that the item was once yours. Try to document (physically or digitally) all purchases of expensive items; for inexpensive items, have photos, receipts, credit card statements, or detailed descriptions of the items for your insurance provider.

Renters insurance plans won’t cover your roommate’s property either, unless you are married or related.

Pest infestations also aren’t covered by renters insurance, which means that the cost of damages done by pests as well as the cost of an exterminator will be on you as a renter or your landlord, depending on the circumstances.

When it comes to pet damages to your own personal property, renters insurance won’t cover those costs, but it will cover pet damages to other people’s property. For example, if your dog destroys your neighbor’s chair, the cost to repair would be covered. It will also cover the cost of veterinary care or medical bills if your pet hurts another animal or person, inside or outside of your home. Some breeds aren’t covered by insurance policies, so look into your plan to see if your pet is protected.

Package theft can be an unclear subject when it comes to renters insurance. Since the theft of personal items is covered by renters insurance, then it should cover package theft, so long as you can prove that your package was stolen. This can be done by having proof of purchase, delivery, and even a statement from the company stating that it was delivered, though it depends on your policy’s limits.

That being said, it might not be worth it to file a claim with your insurance provider for the stolen package if it’s not more valuable than your deductible, as you might end up paying more money just to have it covered. If the cost of the package exceeds the amount that your renters insurance will cover, then you can either be reimbursed for part of it or add a rider to your policy that will protect that item specifically.

Is Renters Insurance Worth It?

Most of the time, the choice is up to you. If you live in an area where there are a lot of thefts, it’s probably a good idea. If you have a lot of valuable items in your apartment, or just want that peace of mind, then yes, it makes sense to buy renters insurance. Depending on the plan, it can be fairly affordable and pretty useful when you need it.

Sometimes your landlord will require that you have renters insurance before signing the lease, since renters insurance can provide just as much protection for your landlord as it can for you. It reduces the chances of your landlord having to pay for any damages, injuries caused by pets, relocation costs due to a natural disaster, or possible stolen property.

How Much Renters Insurance Do I Need?

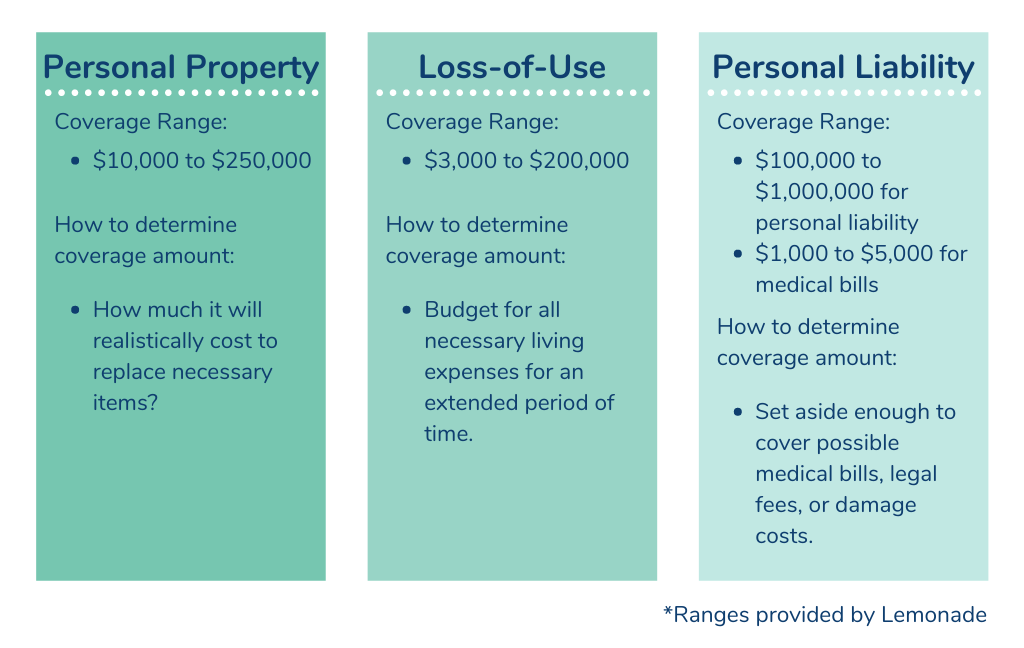

When choosing a renters insurance policy, you will need to decide on the coverage amounts for 1) personal property, 2) loss-of-use, 3) personal liability and medical expenses.

To determine the coverage amount for personal items, think about all the items you have and how much it will cost to replace the things that you will need after a possible emergency. For example, you will probably need to replace your laptop if it’s damaged before thinking about the cost of smaller items like kitchenware. If you follow this method of thinking, you can set aside an amount that’s realistic and worth paying for.

When choosing how much money is needed for loss-of-use or temporary living expenses if your apartment isn’t livable for some time, budget for all necessary living expenses for an extended period of time. That total will tell you how much you will need to be able to maintain your lifestyle until your apartment is livable again.

For personal liability and medical expenses, the amount of coverage you want can be tricky to determine. There are many factors involved, including where you live or if you have a pet. Your landlord or building association might require a minimum personal liability coverage amount in order to rent from them. That being said, think about how much you want to have set aside to cover possible medical bills, legal fees, or damage costs. Be realistic about how expensive medical and legal bills can be, and allot enough money so that you won’t have to take on that financial burden alone.

Oftentimes, we think that our stuff will always be safe; that it will never be damaged or stolen. Why spend money to protect it if there’s only a chance that things could go badly? But when you think about the value of all your items and how much it would cost to replace them, getting renters insurance might be the easiest decision you make.

If you feel renters insurance is right for you or your landlord or building requires it, start with an affordable renters insurance option like Lemonade. Lemonade has low monthly payments, competitive coverage, and an easy-to-use app that will help you get the insurance plan you need. And if you already have insurance but aren’t happy with it, then Lemonade can help switch you over.

The post Is Renters Insurance Worth It? What Does It Cover? appeared first on Avail.

]]>The post A Landlord’s and Renter’s Guide to Dealing With Natural Disasters appeared first on Avail.

]]>

Natural disasters can be devastating for landlords and their renters. According to the National Oceanic and Atmospheric Administration (NOAA), natural disasters create billions of dollars worth of damages in the U.S. each year. This includes about 1,300 tornados, two Atlantic hurricanes, and multiple widespread wildfires annually.

In August 2020 alone, NOAA stated that there were “four billion-dollar” disasters that occurred: the Derecho storm in the midwest, the Isaias and Laura hurricanes, and the series of fires hitting the West Coast.

Since hurricanes, tornados, and wildfires are three common forms of natural disasters, landlords and their renters in high-risk areas should be prepared for them. Here’s what landlords and renters need to know to prepare for and recover from any of these three natural disasters.

1. Hurricanes

Hurricane damage can be the most extensive and costliest of all natural disasters. Damages range from those caused by high winds and hail storms to excessive flooding. Hurricane seasons fluctuate depending on region, with the Eastern Pacific Hurricane Season occurring between May 15 to November 30, while the Atlantic and Central Pacific Hurricane Seasons last from June 1 to November 30.

What Renters and Landlords Can Do to Prepare for Hurricanes

As a landlord, the main preparedness step is to clear all dead or dying trees and branches that are near the rental. This simple maintenance step will reduce the risk of anything falling on the rental property, possibly causing damage to the structure and those in it. Landlords are also responsible for securing siding on the building, closing or anchoring all shutters, and either removing or pinning any movable objects of the building to ensure that they are stationary in high winds.

Renters, on the other hand, should bring all lightweight objects that are outside, such as lawn chairs or tables, back indoors while securing all heavier objects, like propane tanks, to the ground outside.

Both landlords and their renters need to be aware of all evacuation routes, safety zones, and shelters that are available for their area. Again, if a renter is new to the area or region, the landlord can have this discussion with them so that they are aware of emergency protocols during a hurricane.

Renters Insurance for Hurricanes

While renters insurance doesn’t explicitly cover damages caused by hurricanes, many plans will cover windstorm and hail damage, both of which are aspects of a powerful storm such as a hurricane. It’s important that a renter and their landlord check what their respective insurance plans cover in terms of this disaster as insurance providers vary on their wording in terms of hurricane coverage.

2. Wildfires

According to a 2019 report by the National Interagency Coordination Centers (NICC), an average of 2,500 homes are destroyed every year due to wildfires. These fires occur in more than 30 states, with the most significant damage centering around the western region of the country. Though many fires occur in coastal states such as California, the top three states where the risk of wildfire damages to properties is highest are Montana, Idaho, and Colorado.

What Renters and Landlords Can Do to Prepare for Wildfires

Landlords should be consistently monitoring and maintaining a cleared “fire-resistant zone,” which is an area that encompasses up to 30 feet of land that surrounds the rental. This means removing all flammable materials where possible, like leaves and debris, to help prevent a wildfire from getting too close to the property. Landlords should also be aware of the materials they’re using when building or renovating a rental property — using fire-resistant materials or a chemical coating that protects against fires will help maintain the property and prevent it from burning down.

A top priority for renters should be understanding when to evacuate and where to go in case of a wildfire in their area. If the fires are not an immediate threat but air quality conditions worsen because of the fires, renters can create a room that is completely closed-off from outside airflow and has a portable air cleaner in it to keep the renters safe.

Finally, both landlords and renters should know where all fire extinguishers are, should keep important materials in fire-proof safes or have them easily accessible to take when evacuating, and review their insurance coverage in regard to wildfires.

Renters Insurance for Wildfires

While a landlord will probably have fire insurance that protects the building, a renter can add fire coverage to their renters insurance plan to protect personal property within their unit that was damaged due to a wildfire. This form of renters insurance must be held by the renter themselves, as a landlord’s insurance policy for the entire building will not cover the property of their individual renters but instead will cover damage done to the rental property itself.

Depending on the plan that a renter has, there could also be “additional living expenses” or “loss of use” clauses that cover the cost of replacing personal items, as well as temporary living and meal expenses that a renter accrued after being displaced by a fire.

Know that renters insurance plans in areas with a higher risk of wildfire will be more expensive since the probability that the insurance will need to be used is greater. If a renter is not able to find an insurer willing to work with them due to the increased risk of damage, the Fair Access to Insurance Requirements (FAIR) Plan can help with that. These plans are state mandated and sometimes subsidized by private insurance companies in order to cover properties that are more likely to be damaged due to a natural disaster.

3. Tornados

The U.S. alone sees an average of 1,253 tornados a year, according to a study conducted by the NOAA from 1991 to 2010. While they can occur in every state, they are focused primarily in the Midwest and southern states, the most common being Texas (155), Kansas (96), and Florida (66). While not every tornado does damage, or is even dangerous, it’s important to know how to prepare for one just in case.

What Renters and Landlords Can Do to Prepare for Tornados

As a landlord, the best way to prepare for a tornado is to have a safe room (either underground like a basement or “landlocked” meaning there are no windows) that can withstand high winds. This can be difficult in an apartment building, which is why a windowless room can be the safest place for a renter to be during a tornado. Both landlords and renters should bring all lightweight furniture and objects that are outside into the rental to reduce the amount of flying debris.

Renters Insurance for Tornados

Some renters insurance plans will cover tornados, or at the very least, cover extensive damage caused by high winds. Again, it’s important to read through the insurance plan before a natural disaster occurs in order to confirm what your insurance company will cover and what it won’t.

Landlord and Renter Responsibilities Before a Natural Disaster

Landlords and their renters should be discussing the possibility of a natural disaster, what needs to be done to prepare, and what issues can arise at the point of signing a lease. In some areas where a certain natural disaster is common, landlords will even include a clause that outlines what will happen to rent payments, late payment fees, and the lease in general in the wake of a disaster. All of this should outline what a renter needs to know before a disaster hits to be better prepared afterward.

For new renters, landlords can also provide information about evacuation routes and shelters in case of an emergency. If the renter is new to the area, this could be lifesaving advice for them, and advice from a landlord that lived through natural disasters before can put their worries at ease.

Before a natural disaster, landlords should also make sure that their rentals are up to code and structurally sound in order to prevent expensive damage. All safety measures, such as fire extinguishers, smoke detectors, and even emergency shelters should be available and fully functional.

For the benefit of both the renter and the landlord, a conversation about renters insurance should also take place. Many renters insurance plans will cover damages to personal items due to a natural disaster. A landlord is not required to pay any relocation costs or damages to a renter’s personal property that were caused by the natural disaster, which renters should keep in mind when assessing renters insurance policies.

Landlords should also have some form of homeowners insurance that will cover damage to the building overall.

Landlord and Renter Responsibilities Post-Natural Disaster

The aftermath of a natural disaster can be incredibly overwhelming and devastating for landlords and renters alike. There might not be a clear plan of action or next steps for the landlord or their renters, which can make the situation worse. This is why both parties should have a general idea of what should happen after their rental was impacted by a disaster.

While renters should stay in constant communication with their landlords, said landlords will need to know what has to happen in order to get their renters back in their homes. One part of this is coordinating with local officials to have a home inspection once everything is safe. This will determine whether or not the rental is habitable, which will impact the landlord’s next steps.

If the rental is deemed habitable, then the renters can move back in. If it isn’t, there needs to be a conversation between the landlord and their renters on how to proceed in terms of paying rent while the property is reconstructed.

What Happens to a Lease and Security Deposit After a Natural Disaster?

If a rental is habitable, then the lease is still binding and the renter is still required to pay rent. However, if it’s not habitable, generally the renter will not need to pay rent until they can move back in and can even terminate the lease early with no charge. Keep in mind that the requirements and circumstances of terminating a lease early due to a natural disaster range based on state law.

A landlord should also be aware that, even if the unit is habitable and rent needs to be paid, a natural disaster can still affect a renter’s ability to make their monthly payments on time. This could be because of a loss of employment due to the disaster or possible damage costs that put them in financial stress. Staying in contact with each renter will help maintain a channel of communication regarding late rent payments and other accommodations.

Regarding security deposits, landlords cannot use a renter’s security deposit to cover the damages done by a natural disaster. If the lease continues after the natural disaster, then the landlord will still keep the security deposit to use for any renter-caused damages to the property.

Handle Maintenance Issues Caused by Natural Disasters

Though these measures are important first steps, there are many more steps one can take to be completely prepared for these and other natural disasters. And though the aftermath can be overwhelming, particularly for landlords facing some substantial repairs, using a system to file and manage maintenance requests online can help pinpoint and track damages that could be caused by a natural disaster and keep landlords and renters on the same page when it comes to needed repairs.

The post A Landlord’s and Renter’s Guide to Dealing With Natural Disasters appeared first on Avail.

]]>The post Do College Students Need Renters Insurance? appeared first on Avail.

]]>

Renters insurance isn’t usually on a college student’s radar, and that’s not surprising. Between tuition, rent, and beer money, most college students aren’t willing to shell out extra cash for something without immediate benefits.

But what do you do if someone gets seriously injured at your house party and you’re liable? Or if someone swipes your $2,000 MacBook from your apartment? It turns out college might be the best time for your first renters insurance policy.

What Kind of College Student Needs Coverage?

It depends where you’re living. If you live in a dorm or in on-campus housing, you’re typically covered by your parents’ renters or homeowners insurance — as long as you’re listed as a dependent and the policy includes “off-premises coverage.” It’s smart to have your parents check their policy and make sure you’re actually covered for any on-campus loses or damages.

But this all changes when you live in an off-campus rental. Your parents’ policy no longer extends to you, and your landlord isn’t liable for covering or replacing anything that’s lost or damaged in your college rental.

If there’s a fire or someone breaks into the place, it’s on you to replace what’s been stolen or ruined — and that’s where renters insurance can make or break a bad situation.

What Does Renters Insurance Cover in Your College Rental?

Rental insurance typically covers personal property, liability, and additional living expenses. Here’s why each of those matters.

Personal Property

This one covers your belongings. If there’s a fire in your apartment or someone steals your new iPad from your bedroom, renters insurance covers the value of your possessions. Keep in mind that disasters like earthquakes and flooding aren’t typically covered here — you’ll need a separate policy for that.

Liability

This protects you in the event that you hurt someone or someone is hurt in your rental. Let’s say someone got seriously injured during a party at your apartment. The liability protection will pay your legal fees, and in some cases, necessary medical expenses.

Additional Living Expenses

This covers expenses you’d incur if you can’t live in your rental. If your roommate sets the place on fire, this protection will cover your temporary housing and meals while damages are repaired.

Keep in mind that if your roommate has renters insurance, it doesn’t mean it covers your stuff, too. Policies typically only cover the policyholder.

Is Renters Insurance Worth It?

We think so. Based on data from 2012 to 2014, more than 62,000 burglaries, robberies, and car thefts took place on college campuses across the U.S. The overwhelming majority of them — roughly 77% — were burglaries, which would be covered by a renters insurance policy.

How Much Does Renters Insurance Cost?

Not all renters insurance is going to break the bank. Companies like Lemonade have made renters insurance quick, affordable, and modern.

Lemonade offers policies that start at just $5 a month, and everything can be done through their app or online. They take a flat fee, pay out claims quickly, and give what’s left to charities of your choosing. You can get a renters insurance quote in 60 seconds here.

Is It Right for You?

Since your off-campus college rental is a place where doors are more likely to be left unlocked and ovens left on, with roommates and visitors coming and going, it’s a good time to be covered in case something goes wrong. You’ll thank yourself later.

If you’re still looking to find that perfect place, check out the listings on Realtor.com.

The post Do College Students Need Renters Insurance? appeared first on Avail.

]]>The post Avail Partners With Lemonade for Tenant’s Renters Insurance appeared first on Avail.

]]>

Here at Avail, our values are extremely important to us. That’s why we only partner with companies that align with our values and make lives easier for DIY landlords and their tenants. As of July 17, 2019, Avail has teamed up with Lemonade to become exclusive partners in providing renters insurance to tenants nationwide.

Through Lemonade’s advanced machine learning technology, we’re now able to seamlessly provide digital proof of insurance — eliminating the outdated process of tenant’s having to provide printed proof of renters insurance to their landlords.

Lemonade’s modern approach to insurance also means that everything can be done over the app or online, making quotes and claims quick, hassle-free, and user-friendly.

Who Is Lemonade?

Lemonade is a property and casualty insurance company that is transforming the very business model of insurance. By injecting technology — like artificial intelligence — and transparency into an industry that often lacks both, they’re creating an insurance experience that is fast, affordable, and hassle-free. Unlike any other insurance company, they gain nothing by delaying or denying claims (they take a flat fee), so they handle and pay as many claims as quickly as possible.

Additionally, because of Lemonade’s use of artificial intelligence, they don’t need insurance agents, which allows their premiums to be lower than a traditional insurance agency.

“One of the most important factors when considering a new partner is adding value to the user experience,” said Ryan Coon, Avail co-founder and CEO. “We believe that Lemonade’s technology-focused, user-centric approach aligns really well with the Avail DIY mentality and our user-friendly platform.”

Why Partner With Lemonade?

In addition to providing tenants across the country with an affordable (from $5 per month), convenient renters insurance option, Lemonade knocks it out of the park when it comes to values. As a Public Benefit Corporation and certified B-Corp, social impact is part of Lemonade’s legal mission and business model. This means that Lemonade is legally permitted to consider the interests of all its constituents, not solely the interests of its owners.

Lemonade even has a “Giveback” option when you sign up for renters insurance. When you get a policy, you can select a nonprofit you care about. Then, once a year, Lemonade tallies up the unclaimed money left from you and others who chose the same cause, and gives that unclaimed money (up to 40%) to the nonprofit you chose. As of 2019, some of the charities Lemonade gives back to include the ACLU, The Trevor Project, UNICEF, and the American Red Cross.

How Does it Work?

As a landlord and a tenant, renters insurance should be a must for both parties (more on that here), which is why here at Avail we made it a seamless experience with Lemonade. Now, when Avail users sign a lease in a state where Lemonade is available, they will be given the option to get a quote, which takes about 10 seconds. Once a tenant obtains renters insurance through Lemonade, they will be able to do everything on Lemonade’s app from sending claims, editing coverage, adding a significant other, and more. Even better, 30% of claims are handled instantly.

The partnership between Avail and Lemonade will also streamline the process for tenants to show proof of insurance to landlords. Landlords whose tenants sign up for renters insurance through Lemonade will be alerted, and have access to basic information about their tenant’s policy on their Avail dashboard. It’s a win for both parties. See for yourself how easy it is to sign up for renters insurance with Lemonade.

What Does Renters Insurance Cover?

Renters insurance usually covers your belongings, things that other people hold you accountable for, and temporary expenses if you can’t live in your rental. These fall under three types of coverage:

- Personal property insurance covers your belongings (bikes, laptops, TVs, etc.) in the event of a covered loss.

- Personal liability insurance covers damages you’re found liable for — like if someone gets hurt on your property or you damage someone else’s property.

- Loss of use coverage (sometimes referred to as additional living expenses) will help with temporary living expenses if your rental unit becomes uninhabitable.

What Is Not Covered by Renters Insurance?

Typically, the following things aren’t covered by renters insurance:

- Belongings that are lost by the owner

- Natural disasters

- Bed bugs

- Pet damage. However, in most cases, dog bites are covered under your personal liability clause

- Extra-valuable items (there’s a cap on jewelry coverage)

- Your roommate’s belongings

About Avail

Avail is an online platform for DIY landlords and their tenants. We provide tools, education, and support to make renting easy.

The post Avail Partners With Lemonade for Tenant’s Renters Insurance appeared first on Avail.

]]>The post 11 Home Security Mistakes You Don’t Know You’re Making appeared first on Avail.

]]>

As a tenant, home security is often overlooked because you’re likely living there temporarily. However, it’s a large mistake to overlook your safety. In this article, we’ll show you how to avoid the most common security mistakes:

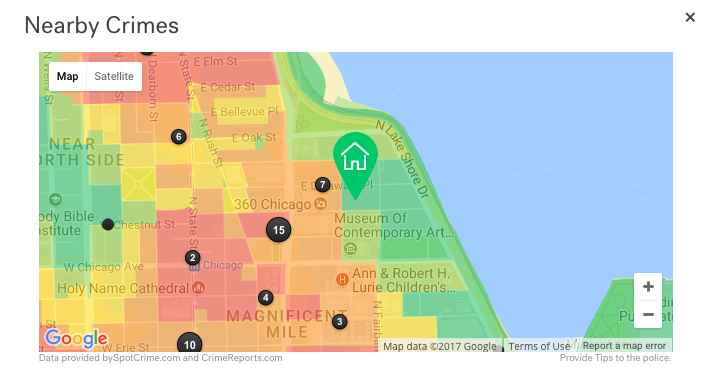

1. You’ve Never Checked a Crime Map

As you’re searching for a rental, and once you live in one, you should be aware of local crime. Some rental listing sites, such as Trulia, offer crime maps. As you’re looking at a listing, you’ll see if crime is listed as low, medium, or high in that location.

In the map (shown below) from Trulia.com, you can see low crime areas are green and high crime areas are shown in red:

Great resources for staying up-to-date are Spot Crime and the ADT Crime Map. You enter your zip code and receive email updates if there’s a crime in a five-mile radius of your zipcode.

Receiving updates about crimes can help you stay informed and keep your home more secure. It’s also helpful to be educated about the safety of a neighborhood as you’re searching for an apartment.

2. You Don’t Have Outdoor Lighting On at Night

Some studies have shown that less crimes occur on well-lit streets. However, outdoor lighting is often not enough on its own. Outdoor security lighting is effective if there are people to witness suspicious activity.

We also recommend keeping your outdoor lighting on a timer. You should re-set the timer for longer hours if you’re planning on coming home late. Walking up to your front door with lights on is safer than coming home in the dark.

And last, we recommend having motion sensor lights around the perimeter of your rental property. This will alert you if someone walks near your property at night. You can purchase these at home maintenance stores, such as Home Depot.

Just remember, outdoor lighting is helpful, but it’s best when paired with a complete home security system.

3. You Don’t Make Sure the Exterior of the Building is Well-Maintained

Burglars tend to scope properties for weeks before intruding and they tend to pick properties that are not well-maintained. If a building isn’t well-maintained then there’s a low chance of the property having a home security system.

Submit maintenance requests to your landlord right away for problems like broken windows, so that your building doesn’t attract burglar attention. And in general, make sure the outside of the building is clean and well-kept.

4. You Don’t Have a Peephole or an Intercom System

If you’re expecting a guest, you should ensure you’re opening the door for the right person. Being able to check a peephole or talk to someone through an intercom system decreases your chance of opening the door for a stranger.

If someone knocks on your door unexpectedly, it’s better to be able to talk to them through an intercom system, rather than opening the door right away.

If your rental property doesn’t have a peephole or an intercom system, we recommend asking your landlord if he or she is willing to invest in it. A good landlord will be interested in keeping the tenants and property safe from vandalism, theft, and violent crimes.

5. You Didn’t Ask for New Keys

When you move into a new rental, you should request that the locks are changed. Not every landlord re-keys between tenants, so it’s best to ask. Having new locks is helpful for a few reasons.

First, it eliminates the chance of prior tenants having access to your unit. Even though tenants typically return their keys, it’s possible they have copies they didn’t return.

And second, brand new locks and keys are usually more secure than older locks.

6. You’ve Never Checked Your Window Locks

Windows are a common entry point for intruders. You should make sure that they are locked at all times. Having a rental with newer windows is also more secure. If your landlord hasn’t updated the windows in 25+ years, then it’s likely time for new windows.

7. Your Sliding Doors Aren’t Bolstered

If your rental has sliding doors, you should make sure they’re securely locked. Having a security bar, or any additional locks, will make your home more secure.

8. You Don’t Have Blinds or Curtains

Blinds and curtains ensure that people outside your home can’t look in, especially at night. This helps for a few reasons. Intruders may try to watch and learn your routine if they can see in. Similarly, intruders may be more likely to choose your property if they see expensive belongings, such as a nice TV, inside of your house.

9. You Don’t Lock Your Doors Every Time You Leave Your Apartment

It’s common for tenants to leave their unit doors unlocked, especially if the building has a locked front door. However, it’s crucial to always lock your door.

It’s often overlooked that a neighbor in your building could potentially rob your apartment.

Consistently locking your doors is your safest bet to avoid an intruder.

10. You Hide a Spare Key Under the Mat

Even burglars know that hiding a spare key under the mat or in a fake rock near the door is common. Try a lockbox or a digital key code to unlock your front door instead, or leave a spare key with someone you trust that lives nearby.

11. You Don’t Have Renters Insurance

Not having renters insurance is a security mistake. After all, it covers damage caused by home burglaries and vandalism, but also fire damage and water damage. It also may cover if someone is injured in your home.

It provides a lot of value at a very low cost, as low as less than $1 per day. Learn why we recommend renters insurance from Lemonade.

The post 11 Home Security Mistakes You Don’t Know You’re Making appeared first on Avail.

]]>The post Do You Have the Right Insurance for Your Rental Property? appeared first on Avail.

]]>

Having the wrong insurance policy for your rental property could cost you thousands of dollars. Often, landlords believe a homeowners policy is enough — but it’s not always enough to cover the added liability of renting your home to tenants.

Questions on Rental Property Insurance

What is the best policy for a landlord to have to protect their properties?

As a rental property owner, you should consider policies that provide:

- Coverage for the appropriate dwelling type, such as a single family home, duplex, apartment and other structures on your rental property, like a shed or detached garage

- Coverage for personal property if you rent your dwelling partially furnished (i.e. you provide certain furniture)

- Liability coverage

- Loss of Rent coverage

If you live in an area subject to flooding, you may need a Flood Policy through National Flood Insurance Program (NFIP). And if you live in an area prone to earthquakes, you might consider adding an earthquake endorsement to your policy.

What should we look for in the tenant’s renters insurance policy?

It is up to the tenant to select his or her coverage and carrier. But in general, you will want to confirm they have a renters insurance policy that at a minimum includes liability coverage. Other important coverage includes personal property coverage and additional living expenses (loss of use).

Lemonade offers renters insurance policies starting at $5 a month that cover all of the above, and renters can get a quote in 60 seconds.

I’d like to understand what is covered for pets. My policy won’t cover damage from my tenant’s pet, but I can collect from their policy if their pet damages my property? Do I understand that right?

Your policy will not cover their pet’s damage. But you may be able to pursue a claim against your tenant’s policy. For example, you may be able to pursue a claim if your tenant’s dog chews on your carpet.

Do renters insurance policies usually include Loss of Use or is this a separate rider?

Lemonade renters insurance

If the tenant’s water overflows and drips down to the below neighbor’s ceiling, who is liable?

In these situations, several policies can come into play as well as the Association CC&Rs:

- Your policy for damage to your property and loss of rents

- Their policy for damage to their condo unit

- Liability coverage if they did something that caused them to be responsible

- The condo association master policy may apply

How does a policy determine who is responsible for repair damages? For example, what if a bad contractor did poor repairs that failed and needed more repairs?

Determination of responsibility depends on the facts of the situation, like who hired the contractor, the policy contract, and the contract with the contractor.

If a covered loss damages a tenant’s stuff, is that not covered under liability damages?

Liability coverage is dependent on your being legally responsible for the cause of the damage.

The post Do You Have the Right Insurance for Your Rental Property? appeared first on Avail.

]]>The post What to Do Before Moving Into an Apartment appeared first on Avail.

]]>

Now that you’ve signed your rental lease, the next step is getting ready for your move. In this chapter, we outline each step to help you thoroughly prepare for your move.

Reach Out to Your Current Landlord

By now, you should have already notified your landlord about not renewing your lease; now you can let them know what day you will be moving out. In response, your landlord will likely want to complete a move-out checklist with you and specify when and how you should return your keys.

Contact Your New Landlord

Let your new landlord know what day you plan to move in. You should ask them some key questions as well:

- When will you receive your keys?

- Where should you park on moving day? Is there a parking area big enough for a truck?

- Are there service elevators for moving big furniture?

- Will you need to complete a move-in checklist before moving in?

- How should you pay the first month’s rent? If you’re paying rent online, you’ll need to set up your account and add your bank account or credit card.

Make Sure You Have Renters Insurance

Renters insurance is always a smart thing to have. In fact, your landlord may have even required it in your rental lease. Renters insurance protects your belongings in case of theft, fires, water damage, etc. It will also insure you up to a certain dollar amount to cover any damage done to your belongings. You can get renters insurance for a low monthly cost, maybe as little as $10.

If you already have renters insurance for your current apartment, all you need to do is call your renters insurance agent. They will walk you through updating your plan for the new address and let you know if there’s any price change.

If you don’t have renters insurance, check out Lemonade and get a quote in seconds. They’ll even help you switch if you’re already insured through another provider.

Set Up Your Utilities

Your lease will outline which utilities are your responsibility. It’s common for landlords to cover water and trash, but typically you’ll need to set up gas, electricity, internet, and cable.

Change Your Address

To change your address, contact USPS. The process is simple: you’ll enter your new address, select whether your new address is temporary or permanent, select whether it’s a family or individual address, and select a forward date. Your forward date should be your move-in date.

Be sure to update your address with your bank, credit card, medical offices, subscriptions, and let your family and friends know, too.

Research Your New Neighborhood

If you’re moving to a new neighborhood, take some time to get acquainted with the grocery stores and shops in your area. You may want to set up a new gym membership, find out what bars and restaurants are in the neighborhood, and what transportation is nearby as well.

Shop For New Furniture

If your new place is bigger or you need new furniture, we recommend shopping at leading furniture stores like Crate and Barrel or Ikea to find new pieces for your new place.

Consider Storage

If you’re downsizing, or there are items you won’t need in your new place, then consider renting a storage unit. We recommend companies like PODS and MakeSpace. They will securely store your belongings at a reasonable price.

Pack Your Belongings

The key to making your move go smoothly is to start packing early. You should start with items that you don’t need day-to-day, such as decorations, sentimental belongings, books and movies, and wall art. You can also pack clothes and dishware that you won’t need before your move early so you don’t have more to deal with later.

Next, organize the last-minute belongings so you can swiftly pack them closer to the move date. Be sure to disassemble any furniture ahead of time to make the moving day easier.

As you pack your boxes, label two sides of each box so you can easily identify what’s in each box. This will also ensure you can read the labels even if boxes are stacked on top of each other.

Consider Hiring Professional Movers

Professional movers will make sure your move goes smoothly. To help you decide whether you need movers or not, consider the following:

- How much it’ll cost you? What’s your moving budget?

- How long will it take to move everything? Moving costs usually depend on an hourly rate, so if it’s a long move it will cost more.

- How much you have to move? Is it possible for you to carry everything yourself?

If you’re looking to hire movers, we recommend TWO MEN AND A TRUCK®. They are experts at swiftly packing and moving your belongings. Learn why our thousands of tenants trust TWO MEN AND A TRUCK® on moving day and get started with a free moving quote today.

Clean Your Current Apartment

Typically, landlords have a professional cleaning service clean the unit once you move out, but it’s still helpful to clean your place before you leave. Making sure that everything is in tip-top shape before handing the keys back to your landlord helps ensure that you’ll get your full security deposit back as well.

Make Renting Easy

If you follow the advice in this chapter, then your next move will go smoothly. As moving day approaches, get your new keys (and make sure they work) and you’ll be all set to move into your new place. For more moving tips, check out our ultimate moving checklist.

The process of looking for an apartment, applying, signing a lease, and getting ready to move can be overwhelming, but the advice in this guide will make it that much easier.

To continue renting with ease, sign up with Avail to manage your entire rental experience online. You can apply to multiple rental properties at no extra cost, sign leases, pay rent, and send maintenance requests to your landlord — all through one platform.

If your new landlord isn’t already on board with online payments, reach out and tell them about Avail. That way, you can make your renting experience that much easier at your new apartment.

The post What to Do Before Moving Into an Apartment appeared first on Avail.

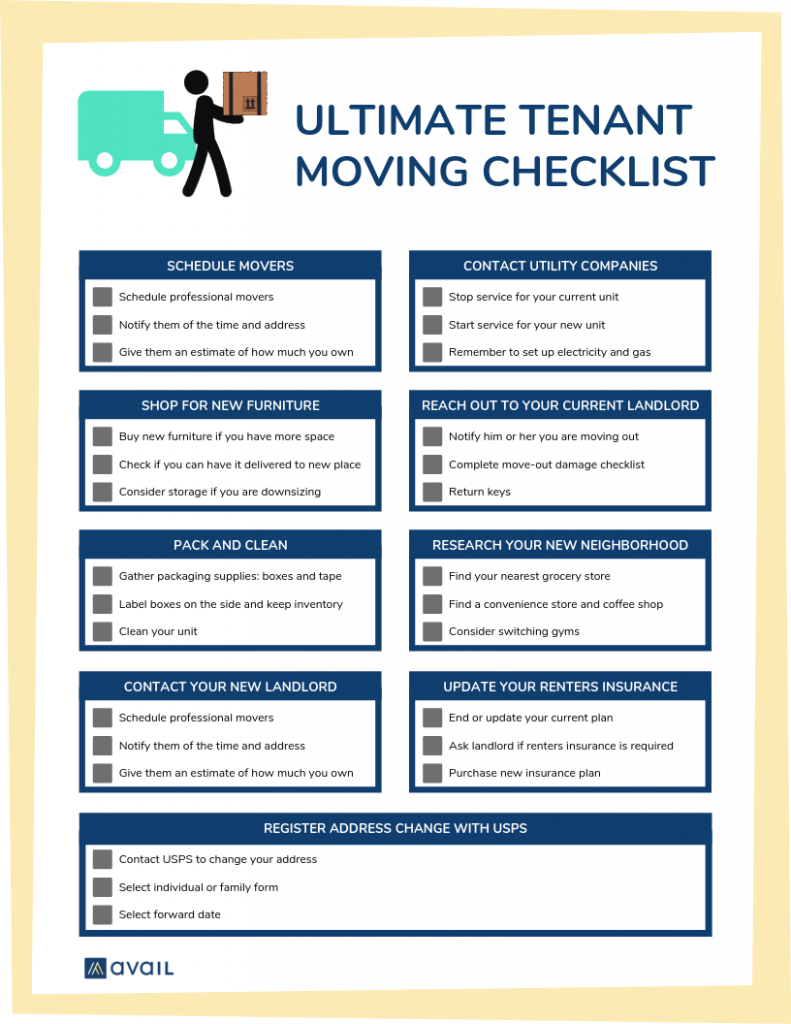

]]>The post The Tenant’s Ultimate Moving Checklist appeared first on Avail.

]]>

You’ve found your next rental property and signed a lease. The next step is organizing your move from your current place to your new place. We’re here to help you prepare for moving day.

With so many important tasks, it’s easy to forget something. You could end up locked out of your new unit, living without air conditioning, or not receiving your mail if you forget one of these tasks. Our checklist below will make sure you don’t forget anything.

Plus, you’re likely to move again in your lifetime. According to an analysis of US Census data by FiveThirtyEight, the average person moves a total of 11.4 times. If you’re between the ages of 20 and 40, then you will likely move 3-8 more times. When you’re continually moving, it’s worthwhile to perfect the process to save yourself time and energy. You can refer to our checklist every time you move.

We know moving is a hassle, which is why we’ve created this checklist for you. After all, our ultimate goal is to make renting as easy as possible for tenants and landlords alike.

Start preparing for your moving day with our complete checklist.

Moving Checklist

Below, you’ll find advice for each step on the checklist.

Reach Out to Your Current Landlord

About 60 days before you plan to move, notify your current landlord that you won’t be renewing your lease. The exact amount of time required to give notice is likely specified in your lease agreement. By giving notice as far in advance as possible, you’re giving your current landlord as much time as possible to search for new tenants. Your landlord needs to be aware that you’re moving out and will need to help you with the process.

You’ll want to ask your landlord for a move-out damage checklist. This step is especially important if you have a security deposit. A move-out checklist allows you to check off what is in good shape and what is damaged.

Your landlord will want to go through the checklist with you, so set up a time for your landlord to stop by. When your landlord stops by, ask him or her if you are required to return your keys. If your landlord is changing the locks, then he or she may not need the keys back. If your landlord wants the keys back, you’ll need to set up a time to return them after you’ve moved out.

Contact Your New Landlord

As soon as you sign your lease, you should reach out to your new landlord about the following important tasks:

- Find out when you can pick up your new keys

- Ask about move-in day

- Does your new landlord want to be present when you complete a move-in damage checklist?

- Is there a certain place you should park?

- Will you need to schedule a service elevator?

- Double check what utilities you’re responsible for setting up

- Double check the move-in date

Verifying the move-in date is crucial. Your new landlord will need to remind the current tenants what day they need to be out by. Communication surrounding move-in day is important because it would be a nightmare if a current tenant hasn’t moved out yet.

You also need to know your move-in date in order to complete the next task.

Schedule Movers

As soon as you know your move-in date, schedule your movers. It’s important to schedule movers as soon as possible to ensure the moving company is available. Weekends are busy times for moving companies, especially during the summer months.

When you call your movers, you’ll need to provide the moving date, your current address, your new address, and a rough inventory of your belongings, especially a list of heavy objects (couches, beds, dressers, etc).

When you reach out to a moving company, you can purchase moving supplies from them. Our preferred moving partner, TWO MEN AND A TRUCK®, offers a wide selection of boxes and packing supplies.

Read why we recommend TWO MEN AND A TRUCK® for your next move and get started with a free moving quote today.

Shop for New Furniture

When you move to a new unit, you may need furniture. If you’ve been using your roommate’s couch and now you’ll be living alone, then it’s time to go shopping.

You’ll also need furniture if you’re moving to a bigger space. You can shop at leading furniture stores like Crate and Barrel or Ikea to find your new furniture.

Consider Storage

On the flip side, if you are downsizing, or moving in with people, you may need to store some of your belongings. Companies like PODS and MakeSpace make it easy for you to store your belongings.

Set Up Utilities

Here are the utilities to set up before your move:

- Electricity

- Gas

- Cable and internet

- Water

- Trash

Most utility companies provide the option to switch your services from one address to another. All you need to do is set an end date for the current unit’s service and a start date at your new address.

Register Address Change with USPS

To register your address change, contact USPS. The process is easy:

- Enter your new address

- Select whether your new address is temporary or permanent

- Note: temporary addresses are less likely to receive spam mail

- Select family or individual

- If you are moving with other people, it helps to select family so each individual doesn’t have to go through the process

- Select a forward date

- This tells the postal service when to start forwarding your mail to the new address

You can complete this task whenever you know your new address. We recommend selecting the forward date to be your move-in date.

You’ll also need to update your address with your bank, credit card companies, medical offices, magazine subscriptions, your office, and be sure to tell family and friends.

Update Your Renters Insurance

Every time you move, you’ll likely need a new renters insurance policy. Renters insurance covers your belongings in case of theft, insures you in case someone is injured on your property, and more. Renters insurance is reasonably priced and can cover you for thousands of dollars in damage.

Check out Lemonade and get a quote in seconds. They’ll even help you switch if you’re already insured.

For more information, check out our Guide to Renters Insurance.

Research Your New Neighborhood

You should find out the location of your nearest grocery store, convenience store, and coffee shop, among other important spots.

If you’re planning on switching gyms, you’ll need to cancel your membership and start a new one.

Similarly, if you have a car and your unit doesn’t come with a parking spot, then you should research what parking permit you will need in your new location.

Pack Your Belongings

The last step on our checklist is packing, since you’ll need to access your belongings up until the time you move.

We recommend prioritizing your packing, starting with belongings you don’t need first. And then pack your last-minute items (toothbrush, towels, etc) closer to when you move.

As you’re packing, you may notice there are certain belongings you don’t use. We recommend donating belongings you don’t need anymore.

To make unpacking easier, clearly label your boxes. It’s a common mistake for tenants to label the top of the box, which makes the label useless once you stack your boxes. It’s better to label the side of the box on at least two sides, so you can easily identify what’s in each box.

As you’re packing, keep an inventory of each box, what items are in each box, and what room the belongings will go in. This ensures you won’t lose anything during the move and will make unpacking easier and more organized.

Clean Your Unit

After packing, you will likely need to clean your unit. You should also do some maintenance before handing it back over to your landlord for inspection. If you’ve hung artwork, we recommend patching up the nail holes. To do this, you can cover the hole with fast-drying spackle until the hole is level with the wall surface. Let it dry for 24 hours.

Landlords appreciate this maintenance and it ensures you’ll get your full security deposit back. Sometimes landlords deduct from security deposits in order to cover cleaning and maintenance fees.

If you use our comprehensive checklist, then you won’t forget any of these important tasks. We want to make your moving process easier than it’s ever been before.

When it comes time to schedule movers, we recommend TWO MEN AND A TRUCK®. They’re reliable, fast, and protect your belongings during the moving process so everything is transported safely.

The post The Tenant’s Ultimate Moving Checklist appeared first on Avail.

]]>The post Top 5 Reasons Tenants Don’t Buy Renters Insurance appeared first on Avail.

]]>

A 2014 poll from the Insurance Information Institute found that 37% of renters don’t get a renters insurance policy. Are you surprised by this? We were surprised, so we did our own investigation to find out why nearly half of renters don’t protect their belongings. What we found surprised us again, because the reasons tenants cited for not purchasing renters insurance were mostly all myths and misconceptions.

If you’re a renter and you are reading this article, you may ask why we care whether renters get insurance. After all, aren’t we a service geared mostly towards landlords? Well, yes, sort of. We certainly help landlords. But we were renters once too and so were most landlords.

We also deeply care about our renters, which is why we designed many of our services around renters specifically. You’ve got belongings, and most of them are likely worth a decent amount of money. Don’t you want to protect those belongings from events that are outside of your control?

So we wrote this blog to help renters, like yourself hopefully, clear the fog of misunderstanding so that you can re-evaluate whether its time to purchase renters insurance. Here are the top five reasons cited for not buying renters insurance.

- I’m covered by my landlord’s insurance

- Renters insurance is just too expensive

- My stuff isn’t worth insuring

- It’s just stuff. My stuff.

- It takes too long

Let’s talk about each one:

I’m Covered by My Landlords Insurance

Nope. That’s just not true. Most policies for landlords cover just two things: 1) the physical structure of the building, and 2) liability should someone be injured on the property (not inside your rental unit). There’s not much in his/her policy to cover your personal belongings or liability within your space. The exception to this is when damage is done to your personal property as a result of the landlord’s negligence (he knew about a leaking pipe, took too long to fix it, and now it ruined all of your clothes). In that case, you could seek reimbursement through the landlord’s policy. However, you would be left uncovered should the property flood due to an otherwise sudden pipe bursting, or should there be a fire, vandalism or theft.

There’s also the fact that a landlord doesn’t own any of your belongings. So even if he wanted to help you out and have a claim be filed for your stuff, the insurance company would most likely determine the landlord doesn’t have an “insurable interest” in the lost/damaged/stolen property. He would then subsequently be denied, which means you would be denied.

It’s also important to note that landlords are not required by law to have a landlord insurance policy. So many tenants may think coverage exists in general where none does at all. Still, if the landlord does have a policy, it wouldn’t cover your personal belongings anyway.

Renters Insurance Is Just Too Expensive

Is it? Did you know you can get renters insurance for as little as 50 cents per day? The national average for renters insurance premiums is actually $12 per month. That’s only $144 per year, less than a leather jacket (and that’s just one jacket, not your entire collection of clothes if you needed to replace them all). The average policy provides for $30,000 of property coverage as well as $100,000 of liability coverage.

There are also levers you can pull that adjust the total expense. You can adjust the deductible (when you make a claim, the amount you pay before the insurance carrier pays anything) – the higher your deductible, the lower your annual or monthly premium payments. You can also increase or decrease the total coverage you want/need. A lower property and liability coverage also means a lower annual or monthly premium.

Rather than thinking that the cost of insurance is too expense, I’d flip that thinking and consider replacing all of your stuff out-of-pocket at one time is too expensive.

My Stuff Isn’t Worth Insuring

Please rethink this. You’ve got a couch you’re sitting on, a TV across from you, and probably a laptop or tablet that you’re reading this blog from. There’s a good chance, you’ve also got some nice clothing hanging in your closet, dozens of shoes, and nice jewelry or a watch. You may be thinking that those were all “hand-me-downs” and aren’t worth anything. It’s tempting to think in terms of what you paid, but in reality, you should be thinking in terms of what it would cost to replace those things.

So even if your TV was a hand-me down when your parents upgraded their TV, if it was stolen, you’d still want to replace it wouldn’t you? And that replacement cost is what you should consider.

It’s Just My Stuff

Unfortunately, this isn’t true either. Well, yes, you would be insuring your stuff. But it’s more than that. Let’s say you’ve got a rug you love. It’s one of those rugs with a lion’s head attached to one side. Your friend comes over, trips on your lion head rug, and breaks a leg. It’s not just stuff anymore when you receive the $30,000 in medical bills. You have to consider that you’ll have guests over who could hurt themselves because of a weird piece of furniture or unusual furniture placement, or even because they had too much wine.

It Takes Too Long

Okay. We have to give credit where credit is due. This certainly is true. In today’s world, something that takes a full 5-10 minutes may just be too long. But, knowing what you know now from the above, don’t you think it’s worth the five minutes to feel and actually be more protected?

Having a change of heart? Hope so because renters insurance is a must. Check out Lemonade and get a quote in seconds.

The post Top 5 Reasons Tenants Don’t Buy Renters Insurance appeared first on Avail.

]]>The post A Guide to Renters Insurance appeared first on Avail.

]]>

Renters insurance is likely one of the last things on your mind when you’re moving or signing a new lease. There’s so much going on — filling out rental applications, packing, finding movers, shutting off and re-initiating utilities — that it’s easy to forget about renters insurance. And once its back on your mind there are so many questions that the momentum stops and you procrastinate getting renters insurance until you’re months into your lease (or sometimes you never get it).

But renters insurance isn’t complex. It’s not expensive. And it should’t take more than a few minutes to get. That’s why we’ve created this guide — to help you figure out the process, get the momentum back on your side, and feel safe in your home knowing that your property is protected.

What Is Renters Insurance?

In the most simplest terms, renters insurance results in a cash payout to you if your property is lost or destroyed. It’s financial protection against the loss or destruction of your possessions when you rent a house or apartment. It’s not much different than other insurance in that it protects you from having to pay huge sums of money out-of-pocket to replace all your possessions.

The distinction that its “renters” insurance simply means that what’s covered is only the value of your belongings (furniture, electronics, clothes, jewelry, etc.) and not the physical building. And thats fine because your landlord should have his own policy that covers the building (and which does NOT cover your personal belongings).

The typical renters insurance policy defines what events you’d be covered under, and includes things like: fire, smoke, lightning, vandalism, theft, windstorms, and water damage (not floods though).

It’s important to highlight that your renters insurance will only cover your belongings from the events listed in the policy (also referred to as “named perils”). This means that if the damage or loss of your property was not due to one of the named perils, you won’t be entitled to a cash payout. Don’t be too concerned about that though, because typically the named perils are the types of events you are most likely to face as a tenant.

Renters insurance also covers you for liability suits that may arise if a guest in your home injures themselves. You never know when a visitor may trip over a piece of furniture and break a leg. But you’ll want to have insurance help cover the medical costs and any personal liability lawsuit that may arise .

What Are Premiums and Deductibles?

The premiums are what you pay for the insurance policy (typically monthly, but could be every six months or even yearly). It’s simply the price of the policy and is determined based on what perils are covered, the value of your possessions, and how much liability coverage you want. When making a claim (reporting losses), the deductible is the amount you will pay upfront before the insurance company will cover any/remaining costs. The amount of the deductible is flexible, but the lower the deductible, the higher your monthly premiums will be. Most renters elect to have a deductible in an amount that they find manageable to cover at a moment’s notice, one that wouldn’t “break the bank”.

Do I Need Renters Insurance?

Short answer, yes! Just ask yourself, when unexpected events occur, could you afford to / want to replace everything you own? Or if you were sued, would you have enough money to pay legal fees and possibly settle the suit? Chances are you can’t, wouldn’t want to, and would benefit from the protection that renters insurance brings. The idea of insurance is to cover you for things where the value, or cost to replace those things, would be high enough that you wouldn’t be able to do it on your own. Very few people can afford to replace all their belongings should they be lost in a fire or another disaster. Surprisingly enough, we found that nearly half of all renters don’t get insurance. And the reasons they gave for not getting renters insurance were surprising. However, you’re here so you won’t be one of them.

Landlord insurance policies don’t cover your personal property and the landlord doesn’t have an insurable interest on your assets (he doesn’t own them, therefore can’t insure them). So if you’re relying on that, you would be out of luck if a catastrophe occurred. In fact, most landlords try to make this very clear to their renters because many tenants wrongly believe they are covered by their landlords’ insurance. Most lease agreements require that you purchase and maintain renters insurance, often going so far as to require you to provide evidence of such, including the type of coverage, its limits and its expiration.

And since renters insurance doesn’t cover the physical structure of the building, it’s relatively inexpensive, meaning price shouldn’t be a barrier for you.

Lastly, most renters insurance will cover your personal property regardless of where it’s located. In fact, one of our founders, Ryan, had his car broken into in Silicon Valley with thousands of dollars worth of stuff stolen. It wasn’t his auto insurance that covered his stolen property; it was his renters insurance policy.

How to Select From the Various Insurance Options?

Insurance Providers

When choosing between insurance providers, you should first consider the reputation, financial standing and reviews that are available for that provider. You can check your State’s department of insurance to make sure they’re licensed and have done all their filings. You can also check J.D. Power, A.M. Best and the Better Business Bureau to see how the companies stack up against each other. What’s important is to make sure the company has the financial standing to be able to pay any claims you’ve made, and the history to show that they DO pay claims fairly.

You should also compare quotes from a few different providers to see how they compare. Some providers have leaner operations, fewer middlemen, etc. and can pass those savings onto you as the customer. This will often be reflected in the different quotes you receive. However, it’s important to make sure that you’re comparing apples-to-apples here. Make sure that one policy doesn’t just appear less expensive because the premiums are lower. Consider what the deductibles and coverage limits are when making the comparison.

Reach out to friends, colleagues and trusted sources to see what they recommend. Oftentimes, people who have first-hand experiences with their insurance carries, especially after a claim, can give you some visibility into the carrier. Here, at Avail, we often get asked if there’s a company we recommend. In fact there is. We’ve done the research we recommended above, spoken with our renters, and vetted many different carriers. We recommend working with the folks at Lemonade to get a quote in seconds.

Actual Cash Value Vs. Replacement Cost

When determining the type of policy, you’ll elect whether your payout for any claims will be based on actual cash value or on replacement cost.

- Actual Cash Value is the value of your property minus any depreciation. Depreciation factors in the age and condition of the property. So a computer you paid $1,500 for three years ago may, after depreciation, only result in a payout of $700. The actual cash value is likely not enough to allow you to fully replace everything – or at least not with the same level of quality as your property that was lost, damaged or destroyed.

- Replacement Cost, on the other hand, is the actual cost of replacing your property (depreciation is not factored in here). So the laptop you paid $1,500 for thats been destroyed, you’d be paid on the amount you actually must pay to replace your laptop with the same one or a comparable one.

Because the replacement cost type of policy covers you more fully, it also means your premium would be higher than the actual cash value policy. However, this increase is not typically substantial and most renters should elect to select the replacement cost policy.

Property Coverage Limit

You’ll want to figure out what coverage limit to have on your property (or how much your property is worth). The best way to do this is to take an inventory of your property and its value. You can do this on a sheet of paper and sum up all the values. Do this for your clothes, shoes, electronics, furniture, jewelry, etc. When you get to the end and sum it all together, you’ll be surprised. Your property is usually worth a lot more than you’d initially think. According to State Farm, the average renter has more than $35,000 worth of property in their rental. This can be considerably more depending on the number of bedrooms and people living in the unit or house.

As you’re creating your inventory list, you should consider also taking photos or a video describing the items, when/where you bought them and how much you paid for them. This will come in handy should you need to do a claim in the future. And since you’re already going around the apartment making an inventory list, you might as well create the evidence at the same time.

One important note here is that there is usually a limit per single item, particularly around jewelry. For example, most policies will have a $1,000 limit per piece of jewelry. So if you have jewelry and other items that are more than the standard limits for a single item, you’ll want to consider adding to your policy to cover those specific items individually. This is known as adding a rider to the policy or a personal articles policy.

A higher property coverage limit will directly increase the total premium you pay.

Liability Coverage Limit

The typical liability coverage limit is for $100,000. This is the coverage that kicks in if a guest is injured while in your rental home, and covers medical costs associated with the injury. Claims here don’t typically have a deductible apply, whereas claims for damage to property always do. However, many insurance agents recommend increasing the liability insurance amount past the $100,000 average as medical costs and liability suits can go quite high.

How this impacts my premiums…

A higher liability coverage limit will increase the total premium you pay.

The Deductible and Premium Tradeoff

As mentioned earlier, the deductible is the amount you’ll pay when you submit a claim before the insurance carrier’s coverage kicks in. Another way to think about it is your share of the claim. As an example, if you have a claim for $10,000 and a deductible of $500, then you’d be reimbursed for $9,500, with the remaining $500 being your share of the liability. The deductible is something you can adjust higher or lower when you’re first creating your policy. If a $500 deductible is too high for you, then you can lower it. However, a lower deductible will mean a higher premium. Some renters prefer to have a higher deductible so that their premiums are lower.

This is a tradeoff that you’ll want to consider and adjust based on what you’d be willing to pay out of pocket if a disaster occurs and what you can afford, or be willing to pay, monthly in premiums.

How to Get the Best Deal on Renters Insurance

There are a few other items that can help you get the best deal and lower the cost of your renters insurance policy. Here’s a quick list:

- Ask for a smoke alarm and fire extinguisher discount. If you have these properly installed/placed in the apartment, many carriers are willing to offer a discount. In many places, it’s actually a legal requirement that the landlord provide smoke alarms and fire extinguishers, so these should be an easy discount.

- Have a security/alarm system in place that monitors for break-in, vandalism, etc. This deters theft and should help you lower your monthly premiums. There are several companies available that offer affordable, flexible and moveable alarm systems so that you can take the system with you when you leave.

- Pay your renters insurance bill in full, upfront, rather than in monthly installments. There’s typically a discount for prepayment.

- Buy your car insurance or other lines of insurance with the same company. There’s usually a discount, called a “multiline” discount for having multiple lines of insurance with the same carrier. The additional benefit here is that with a company like State Farm, you’ll also be building a relationship with an agent who can provide more than just insurance options.

6 Questions to Ask Your Insurance Agent

When you’re ready to dive in, these are the questions you should ask your insurance provider so that you make sure you have the right coverage and understand how claims are handled.

- Is all my stuff covered?

- What perils are covered?

- What happens if someone gets hurt in the apartment?

- Does the policy cover all roommates?

- Is my dog covered, too?

- How much will the policy cost?

These are all the basics. If you have more specific questions or needs, check out more information here.

About Avail

Our online rental software helps do-it-yourself landlords be more effective, fair and honest with online tenant screening, digital leasing, and online rent payments. Tenants find the software user-friendly, intuitive and enjoy the transparency that Avail brings to the rental process.

The post A Guide to Renters Insurance appeared first on Avail.

]]>